My family lives just five miles inland from Newport Beach, in the neighboring city of Costa Mesa. Given how close the two cities are – literally sharing a border – I used to assume that checking the weather outside my window was enough to prepare for a beach day with the kids.

But after a few surprises, I learned the hard way: Costa Mesa weather is not Newport Beach weather. While it might be sunny and warm at home, the beach can be cloaked in a cool marine layer, leading to a chilly beach day.

It turns out, a quick glance outside isn’t always good enough.

Roth Conversions: Does the Hype Deliver?

In financial circles, Roth conversions are often hyped up.

I’m a strong advocate for proactively considering Roth conversions. But they’re often misunderstood or oversimplified. Many investors are told to convert based on a simple tax bracket comparison without considering the broader tax implications. Like glancing out the window when you really need to check the beach forecast, it’s not quite sufficient.

This article isn’t intended to pinpoint the perfect timing for a Roth conversion or to provide an exhaustive list of pros and cons. Instead, its purpose is to help you – the informed investor – recognize that Roth conversion ‘tax traps’ do exist.

With this awareness, you’ll be better equipped to collaborate with your CPA or financial professional.

*Please note: this article is for informational purposes only and should not be considered tax advice.

What is a Roth Conversion?

First things first… a Roth conversion is a taxable event whereby an investor transfers money from a pre-tax account (often an IRA) into a Roth IRA, often with the goal of tax-free growth within the Roth IRA.

The Oversimplified Roth Conversion Logic

Here’s a common rationale:

- The client is in the 22% federal tax bracket today

- They expect to be in the 24% bracket in retirement

- Therefore, they should convert now to “save” 2% in taxes

Sounds logical, right? Not so fast.

Roth Conversion Tax Traps

Let’s establish two key facts with Roth conversions:

- This is a taxable event that increases your Adjusted Gross Income (AGI) and Modified AGI (MAGI).

- AGI and MAGI affect far more than just your tax bracket.

These figures influence everything from Social Security taxation and Medicare premiums to capital gains taxes, tax credits, and more. That’s why a Roth conversion can trigger unintended tax consequences.

Because of these ‘tax traps’, it is not sufficient to say, “I am in the 22% bracket now and will be in the 24% bracket in the future, therefore I should do a Roth conversion.”

Below, we’ll review factors that can negatively influence Roth conversions, along with two real-world examples.

State Taxes

If you currently live in a high-tax state like California or New York but plan to retire in a no-income-tax state like Florida or Texas, converting now could mean paying unnecessary state taxes.

Social Security Taxation

Whether your Social Security benefits are taxed depends on your total income from other sources. Converting funds to a Roth IRA can significantly impact this, potentially increasing the portion of your Social Security benefits subject to tax from 0% up to 85%. To be clear, this means 85% of your benefits are included in the tax calculation. It does NOT mean the benefits are taxed at an 85% rate.

IRMAA, NIIT, and QCDs

I’m certain this article would go viral if the title were “IRMAA, NIIT, and QCDs”. Jargon jokes aside, these three acronyms are quite important when it comes to Roth conversions.

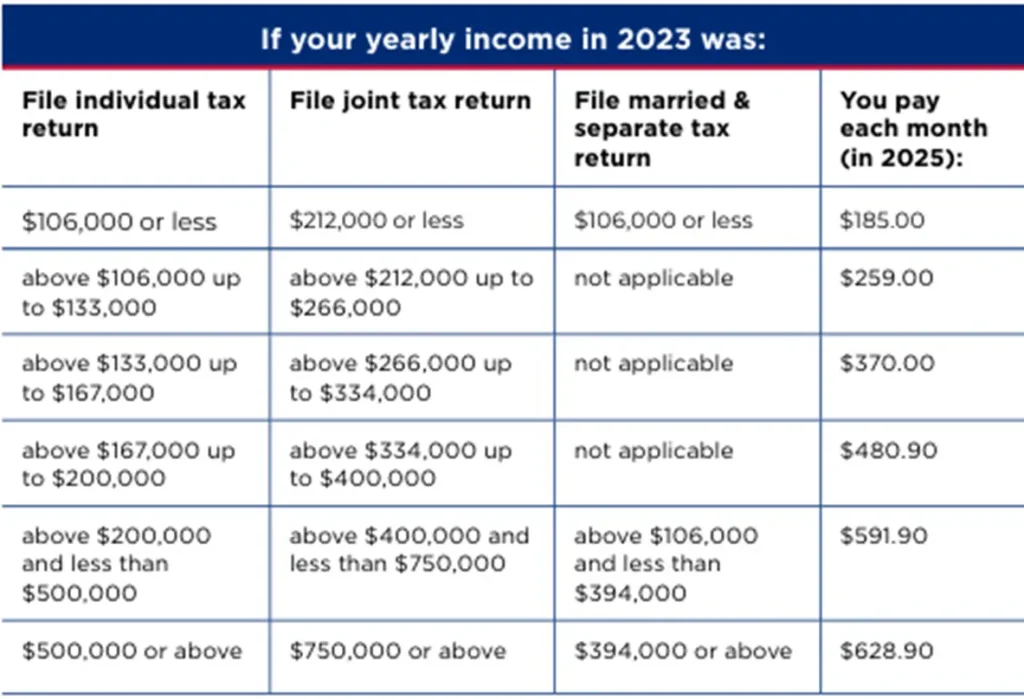

IRMAA stands for Income-Related Monthly Adjustment Amount. A higher MAGI can push you into a higher IRMAA bracket, increasing your Medicare B and D premiums by thousands of dollars each year. See the table below from www.medicare.gov regarding Medicare Part B rates.

NIIT stands for Net Investment Income Tax. If your income exceeds $250,000 (married filing jointly) or $200,000 (single), you may owe an additional 3.8% on investment income.

QCD stands for Qualified Charitable Distribution. Proponents for Roth conversions will often say, “I want to avoid future Required Minimum Distributions (RMDs), so I choose to do a Roth conversion now.”

However, if you’re charitably inclined, future RMDs can be mitigated or even eliminated by giving money directly from an IRA to charity when you turn 70.5.

Dividends and Capital Gains

Qualified Dividends and Long-Term Capital Gains get preferential tax treatment; however, increasing your AGI via Roth conversions can increase the rate at which they are taxed (from 0% to 15%, or 15% to 20%).

Tax Credits

Many tax credits—like the Child Tax Credit or Premium Tax Credit—are phased out at certain income levels. A Roth conversion could disqualify you from these benefits.

Real-World Examples

Example 1: Young Family

- Married couple with two young children

- $200,000 in wages

- $200,000 in long-term capital gains

- Considering a $50,000 Roth conversion

Result:

They remain in the 22% bracket, but the conversion phases out much of their Child Tax Credit and subjects more of their capital gains to the 3.8% NIIT.

Example 2: Retired Couple on Medicare

- Married couple, both age 65

- $50,000 pension

- $60,000 Social Security

- $35,000 in qualified dividends

- Considering a $120,000 Roth conversion

Result:

- Jump from the 10% to the 22% tax bracket

- Social Security becomes 85% taxable

- All dividends are taxed at 15% instead of 0%

- Medicare premiums increase by $2,220 per person

Not quite the savvy tax move they expected.

Knowing the Weather in Both Places is Helpful

If I wake up and it is raining in Costa Mesa, I know not to go to the beach. There’s no need to check the weather. But if it’s sunny, I’ve learned to check the Newport Beach forecast too. Although the proximity is close, it’s not the same, and my children might get upset that I didn’t pack appropriately (hypothetically, of course).

Roth Conversions Are Still Powerful – If Done Right

I hesitated to write this article because I believe in the power of Roth conversions – I certainly don’t want to scare readers away from this technique. When executed strategically, they can significantly reduce your lifetime tax liability. Please do consider them and ask your advisor about them.

But beware of the other influences beyond the headline tax bracket. Work with a professional to evaluate your full tax picture before making a move.

As we head into the summer solstice, I wish you sunny beach days and savvy tax planning.

Until next week…