Today, I want to talk about how to save money in taxes. The strategy I will present has the potential to save a significant amount in taxes. This strategy is one I’m sure you’ve heard about, but I will submit that it is often misunderstood.

Today, we will discuss Roth conversions. The timing of this article should be ideal, as this is typically the time of year (November) when I assist clients with their annual conversions.

But before we jump in, let’s start with a story about my middle child…

Lost in Translation

At home, we have a 6-year-old, a 4-year-old, and an almost 2-year-old. Yes, you are correct; it is a beautiful chaos… daily.

My 4-year-old says the funniest things. We really need to start writing down all his little one-liners because there are so many that I often forget them.

My two boys love bunk beds. We have a guest room that has two sets of bunk beds, and their weekend treat is often to sleep in the bunk bedroom. We recently invested in a camper van that also has bunk beds, which the kiddos are over the moon about.

We went on our first family camping trip last week, and as you can imagine, bunk beds inside a cargo van are going to be a bit tight. During the acclimation period, you could hear a medley of thumps and bumps as little noggins on the bottom bunk collided with the top bunk.

Later that evening, our middle child looked at me with a smile ear to ear and told me that he was so excited to sleep in the “bump heads.” I wasn’t sure if I heard him right, so I asked him, “You want to sleep where?” He exclaimed, “In the bump heads, daddy!”

He went on to explain to me, in all seriousness, that they are called “bump heads” because sometimes you bump your head. I loved the logic, the misnomer, and everything about this 🙂

Sometimes, things just get lost in translation…

A History Lesson

Roth conversions aren’t much different than “bump heads.” People are familiar with the term and some mechanics but often get lost around the strategy and execution.

To understand Roth conversions, you must first understand the history behind defined contribution plans. To understand defined contribution plans, you must first understand the history behind defined benefit plans (pensions).

Your grandpa probably had a pension, or at least some of his friends did. During his working career, people didn’t do much job hopping, and their loyalty was rewarded with a lifetime income throughout retirement – a pension. Nice for the employee, but quite expensive for the business. These liabilities (pensions) are also hard for the business to quantify because an actuary needs to provide reliable estimates of returns and longevity (the lifespan of the beneficiaries). What happens when returns underperform expectations and people live longer? These liabilities become weighty and burdensome.

So, there needed to be an evolution away from pensions. Rather than the company needing to define the benefit and manage these monies to last your lifetime, they decided to shift the responsibility to you (the employee) with a defined contribution plan. In 1978, as part of the Revenue Act, section 401(k) was added to the Internal Revenue Code.

Now, employees can allocate portions of their income to their 401(k) (defined contribution plan). These assets would grow tax-deferred, and the income tax would be assessed when they distributed the funds during retirement. With one caveat, the IRS would mandate that portions of these tax-deferred monies begin to be distributed at certain ages, which we call a Required Minimum Distribution (RMD).

Exact Opposites

The simple explanation was and is that the defined contribution plans allow employees to earn money today and pay taxes later. The hope/intention for the participant would be that taxes in the future, during their non-working years, would be more advantageous than the tax rates in their peak earning years.

What’s the simplest explanation of a Roth conversion? You are electing to move assets from an IRA to a Roth, meaning you will incur taxes today to place those assets in an account that will grow tax-free for the rest of your life. You are basically undoing those 401(k) contributions, instead of electing to defer you are electing to realize that income.

Again, this election would be based on believing that you could get a better deal on taxes today versus tomorrow.

So, what would drive someone to believe that they could convert (realize taxes) today and that it would be more advantageous than waiting? Often, it’s because of future Required Minimum Distributions. With even the most straightforward financial planning software, one can see how those future RMDs will eventually drive up one’s taxes and into higher tax brackets. Essentially, it can force the participant to withdraw more than what is needed, creating more taxes than preferred.

As I often say, a Roth conversion is a CHOICE to elect to pay taxes today versus a REQUIREMENT (RMD) driven by the government in the future. The goal/intent would be to reasonably align those conversions in lower brackets to save taxes over a lifetime.

All About Timing

Ideally, as I said earlier, you want to defer in higher brackets and convert in lower brackets. Deferrals and conversion give you some authority on timing versus earned income and RMDs, which take away that flexibility.

This means that, most often, investors will use what I would call their “gap years” to execute these conversions strategically. The gap years are the time between when you stop receiving a paycheck (retirement) and your first RMD.

At this point, I think an illustration would be most helpful, so let’s jump into a simple example of this…

For Example…

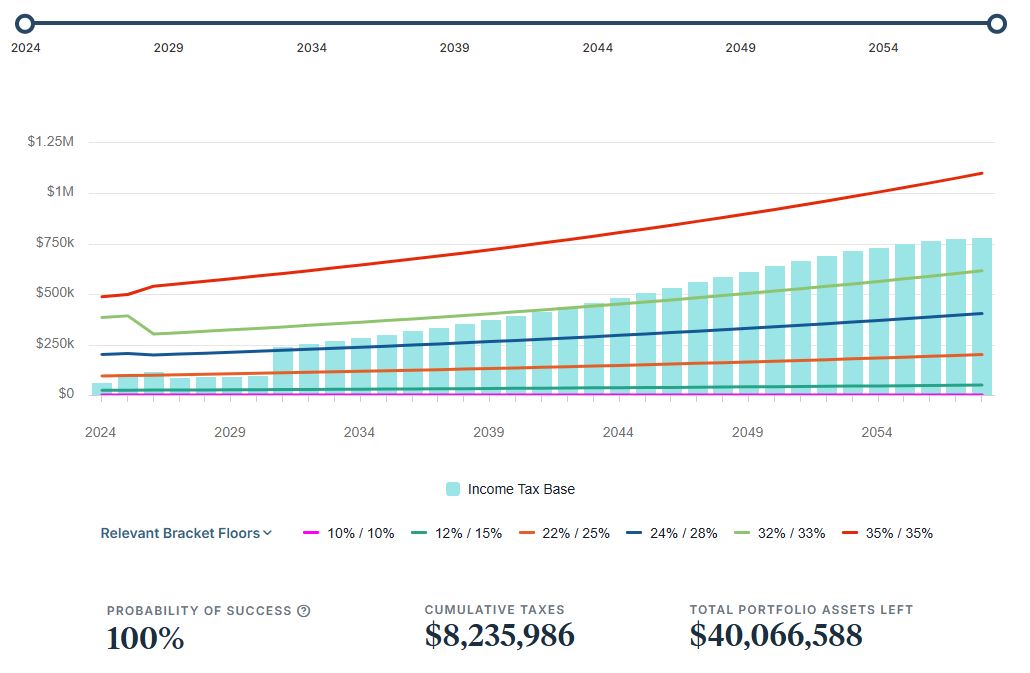

Here is a snapshot of a client in those gap years from our planning software. This client has a net worth of $7mm, has modest annual spending, and will begin RMDs in 2031. As you will see, those RMDs will have this client jumping from the 12% tax bracket into the 24% tax bracket. Note that the turquoise bars represent the taxable income by year, and the colored lines running across represent the tax brackets.

Source: eMoney- Nov 7, 2024

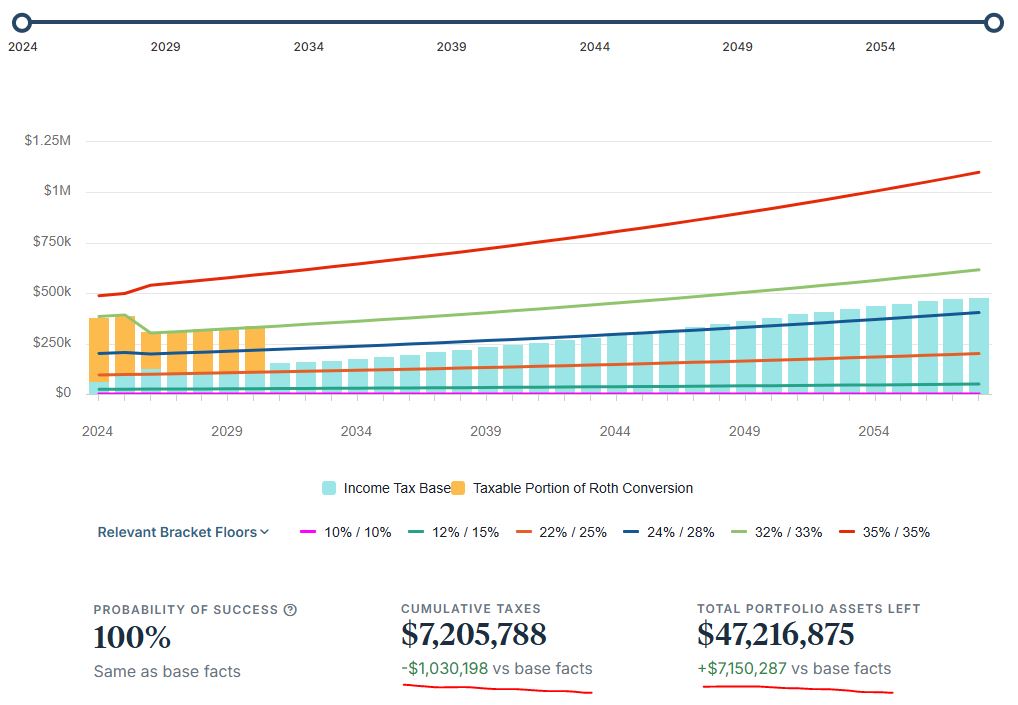

Over the next 30+ years, the above forecast shows an estimated total tax of over $8mm. So, what if the client implemented a simple Roth conversion strategy that focused on smoothing those future tax bills into the gap years rather than allowing the RMDs to drive the client’s tax rate higher over time? The illustration below shows Roth conversions “filling up” the 24% tax bracket over the next seven years.

Source: Money – Nov 7, 2024

This simple illustration represented over $1mm of lifetime tax savings and over a 15% increase in net worth at the end of life. I will mention, too, that these conversions led to a more attractive net worth composition, as tax-deferred assets were depleted, and tax-free assets (Roth) were increased significantly.

Most and Few

The issue we conclude with is that the above is just an example, and these types of illustrations have lots of nuances. You need to tailor a scenario to you. You need to look at the impacts on Medicare premiums, capital gains tax implications, how this might affect the taxability of your social security and a laundry list of other items. That’s what we are here for, so I encourage you to engage your advisor and begin the dialogue. The strategy you choose will impact the taxes in your lifetime and, most likely, the tax implications that your heirs will inherit.

Here’s my main point, though: most people I talk to either currently participate in a retirement plan through their employer (e.g. 401(k)) or they have in the past. Very few people I talk to have considered or executed a Roth conversion strategy. This is what I am calling “most and few.” If you really think about it, Roth conversions are simply the reverse action of a 401(k) contribution. Millions of employees around the country will defer taxable income into their retirement plan from their paycheck, and a conversion would simply be the opposite election – a choice to realize taxes now versus later because you see an opportunity to take advantage of a reasonably better tax rate.

Sure, it was funny that my son calls them “bump heads,” but we all know they really are just “bunk beds.” Sure, a “Roth conversion” seems like a confusing and technical term, but they are really just the inverse of a contribution into a tax-deferred retirement account. It’s just that simple.