Hindsight is 20/20

If I only had a time machine…

I tell myself this quite often: if I only had a time machine, I swear I would be the best investor of all time.

It reminds me of Biff Tannen in Back to the Future Part II, where he snags the Grays Sports Almanac from the future, which he then uses to go back in time and become a gambling phenom.

My most recent time-machine-moment comes from watching the rise of mortgage rates. I am kicking myself for getting a 7-year interest-only loan when I bought my new house. I was able to personally negotiate a slightly lower rate this way, but oh, do I wish that I locked in a 30-year mortgage.

Hindsight is 20/20, right?

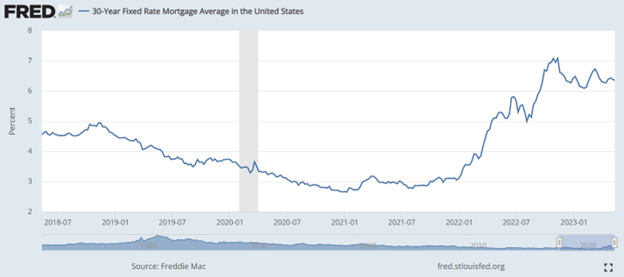

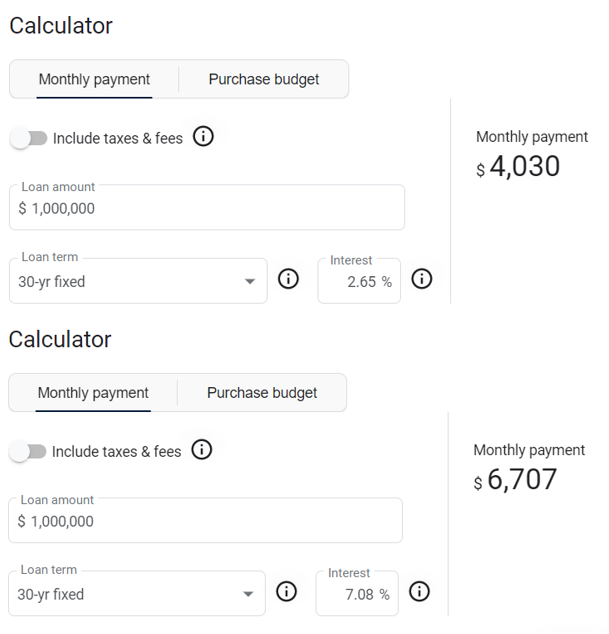

Take a look at rates since they bottomed out in early 2021; the national average on a 30-year fixed mortgage was 2.65% compared to 7.08% in November of last year. Just to give perspective, here is a look at the cost difference on a monthly payment (2.65% vs. 7.08%):

*For illustrative purposes only

So, if you locked in a 30-year loan in the 2’s or 3’s, I think you should pat yourself on the back. Whether by luck or skill, it would seem that you timed that purchase or refinance quite well.

No Regrets

Joking about time machines helps me not to dwell too much on my past financial decisions. For me, humor and making light of it always helps; no regrets. As investors, we will always work with the information we have at hand and try to make the decisions that best fit our financial plan.

Yet, there is always a benefit to watching some “game film” – my way of describing the process of reviewing past financial decisions – to see what we can learn from our own decisions and behaviors. David Bahnsen was presenting to the team this week and brought up this concept of the Freeze-Frame Myth. A concept that is most often used in discussions about economics, a caution against assuming the way things are today (population trends, demand for natural resources, etc.) will always be the same. This concept is very relevant to personal finance as well. My choice of a variable rate loan (fixed for 7 years, then variable) at the time was steeped in this belief that rates would remain low for a long time. I figured 7 years would give me plenty of time to pivot to another borrowing solution.

Now, I would assume that even the most intelligent finance minds would not have predicted that violent spike in rates. Yet, it was my assumption that things tomorrow would be just as they are today, which led to a less ideal planning decision.

Sitting on their Hands

This reality of changes in borrowing rates wasn’t unique to me; this is impacting all investors. Savers are now – for the first time in a decade or so – feeling well compensated in their money market accounts, leading many of them [investors] to not want to take any risk beyond “safe” assets for the time being. Potential home buyers are sitting tight, as they can’t fathom borrowing at rates double what their neighbor borrowed at.

So…. Everyone is sitting on their hands.

In a recent DC Today, David Bahnsen described it this way:

Mortgage applications are down to levels last seen in the late 1990s.

I am becoming more convinced that the challenge right now is volumes have collapsed, but prices aren’t budging a lot because sellers believe prices will be higher when rates inevitably drop, and buyers believe monthly payments will be lower when rates inevitably drop. And more fascinating is that many transactions that otherwise would be happening (upgrades, relocations, upsizing, etc.) are not happening because folks who can afford bigger and better or want bigger and better are staying put because of the attractive rate they have on their current home.

With this said, I caution you not to fall victim to the freeze-frame myth. What you are seeing today is not predictive of tomorrow. You must do a biopsy of your beliefs and challenge your assumptions.

The Futures

As David mentioned in this same DC Today, futures are estimating a 99% chance that the Fed will cut rates from their current level before year-end. Granted, we can’t speak with the complete authority of when rates will drop or by how much, but it would be reasonable to assume that a trend (interest rates) that has been heading in one direction is most likely to shift course in the near future.

The Fed raised rates with the intention of stabilizing prices; combating above-average inflation. We have seen those inflation figures lose momentum and trend down. Perhaps (most likely) for other reasons outside of the Fed’s manipulations, but we will save that topic and conversation for another day.

All this to say that it doesn’t take the mind of Sir Isaac Newton to conclude that interest rates will have some sort of gravitational pull back to reality, back to some sort of “natural” rate.

What Does this Mean for You?

If you are reading this, I will assume you are an investor. Whether you have $1 invested or if you have $1 billion invested. If you are an investor, then I will assume you have financial goals and aspirations. Whether that be retirement plans or charitable ambitions. These goals, your goals, aren’t taking a time out for 2023. Yes, the White House will have its political boxing match regarding the debt ceiling, the Fed may continue to surprise you with its decisions around interest rates, and there is a laundry list of other geopolitical headlines that can cause concern. Yet, again, your goals will not rest based on these happenings and headlines.

Your goals are objectives to be achieved in the future, and the steps to get there are all the little financial decisions you will make along the way. Let me be candid; too many investors are in a holding pattern right now, thinking that decisions will be easier to make in the future. I opened up today’s article saying that I wish I fixed my mortgage rate for 30 years, but I didn’t, and that decision – although it would be great to change it – will not make or break my financial plan. It’s actually great that I did choose to execute on that mortgage because that rate and that opportunity window closed quite quickly. If I would’ve dragged my feet, I would’ve been much worse off.

You might be faced today with needing to borrow money – whether for the purchase of a home or to fund a project for your business. Yes, rates are higher today than they were in the recent past, but you can’t let this reality paralyze you from making a decision. One of the admirable attributes of American society is that people adapt, pivot, and evolve quickly. We have these idioms that speak to this reality – you’ve got to play the hand you’re dealt, or when life gives you lemons, make lemonade.

So, if you are an investor adjusting your allocations to fixed income because the uncertainty is overwhelming you, let me remind you that this uncertainty has always, and will always, exist. In a sense, your returns are just that, an uncertainty premium. If you are a borrower skittish about rates, I want to remind you that rates change – it was the rise in rates that has created discomfort, but the reverse (falling rates) will create a future refinancing opportunity for those that do borrow. This is financial planning 101, learning to manage both the asset and liability side of your balance sheet and being nimble enough to pivot as the environment changes.

Fear Itself

FDR said it best in the throes of the Great Depression, “The only thing we have to fear is fear itself.”

I talk to investors all day, every day. This is my occupation. The fear out there right now is crippling people; everyone is in a wait-and-see posture, and many find themselves sitting on their hands. We should never take action without reason and purpose. All actions and decisions need to be aligned with the objectives of one’s financial plans. Yet, we also can’t let the environment and our emotions lead us to inaction.

What about you? Have you hit the pause button in some area of your financial life? If so, maybe it’s a good time to connect with your advisor and start a dialogue.