This last weekend I got to thinking about an interesting question, how did generations of the past accumulate enough wealth to retire? This curiosity was spawned from an observation of my own generation (Millennials), who don’t seem like they are saving enough to prepare for retirement. So, I was curious to know how past generations made it work.

In my undergraduate studies at Biola University, I completed a lengthy research paper on Millennials. This was my first time studying about generations and I was fascinated by the traits that permeated those who shared a common birth year(s) and grew up together during a particular time in history. I thoroughly enjoyed reading about the cultural influences that differentiated Millenials from Gen Xers and Baby Boomers.

In my research, I did not read or write much about the personal finance difference of these generations, so what better place than TOM to pick up where I left off. Today, we will take a look at how generations of the past made retirement work.

And off we go…

The Name Game

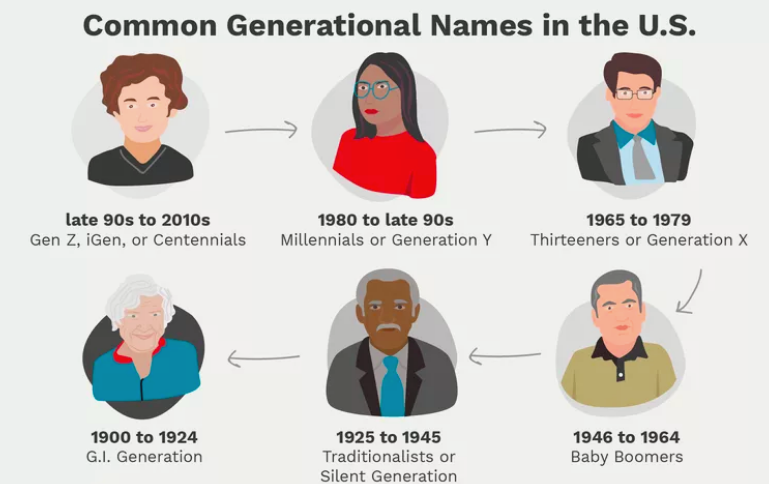

These generations are most commonly segmented and named like so:

Source: www.thoughtco.com

Throughout our discussion, we will reference these common titles, but we will focus the structure of our conversation around some TOM created segmentations of our own: The Pension Generation, The Real Estate Generation, and The Inheritance Generation.

The Pension Generation

Many folks of the Silent Generation and the Baby Boomers benefited from pensions. Pensions are a defined benefit plan, which is much different than a defined contribution plan (e.g. 401(k) plan) that we are most familiar seeing today. Just like the title says, a defined benefit plan defines a future benefit that will be allotted to a participant. These pensions provided lifetime income after a certain threshold of years of service was met. These types of benefits made retirement planning very easy, as the pension would offer a somewhat seamless transition from employment income to retirement income. Work stopped, yet the paychecks continued.

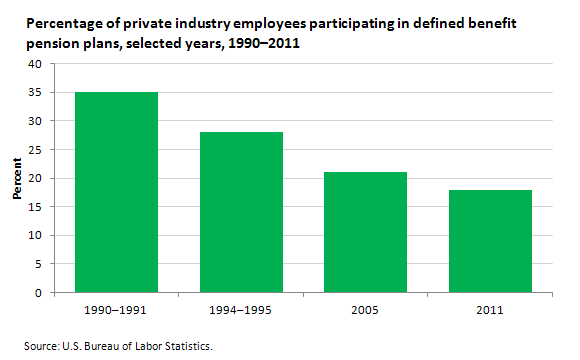

In 1875 the American Express Company was the first to offer a corporate pension in the United States. According to an article on The Balance, “By 1950, nearly 10 million Americans, or about 25 percent of the private sector workforce, had a pension. Ten years later in 1960, about half of the private sector workforce had one.” Another article from CNN expanded on this statement, “The percentage of workers in the private sector whose only retirement account is a defined benefit pension plan is now 4%, down from 60% in the early 1980s.” The Bureau of Labor Statistics shows us the steady decline following this peek:

Source: Bureau of Labor Statistics

Source: Bureau of Labor Statistics

So, how did this generation prepare for retirement? Pensions were one contributing factor that existed then, and not so much now. If pensions were so great, why’d they disappear? They are difficult to fund. When a company is funding a defined benefit, they are guaranteeing perpetual income and they need to make some assumptions about a retiree’s longevity and rates of return, which can be hard to predict. Looking at longevity, according to The World Bank, in 1960 life expectancy in the United States was approximately 70 years old and by 2016 it had risen to almost 79 years old. This +9 year expansion in lifespans would result in a significant additional funding need for a company providing a pension. Regarding rates of return, the world experienced two notable recessions:

In just one decade – the dot com bubble and the financial crisis of 2007-2008, this “lost decade” had a brutal impact on companies pension funding efforts.

Although the income stream seems easy and seamless from the employee’s perspective, the company is responsible for making all the funding mechanisms work behind the scenes. Surviving as a company is tough enough in itself, so imagine adding the responsibility of funding thousands of people’s lifetime income on top of that. It’s not an easy endeavor.

I will note one potential downside to the pension is that it does not create inheritable wealth for future generations. For prudent savers and wise investors, the defined contribution plan (e.g. 401(k) plan) is an attractive offering as the participant is able to “self-manage” their assets to meet their future income needs and build a legacy of wealth for future generations.

The Real Estate Generation

Many of my friends have caught the real estate bug, as they have seen how their parents have accumulated wealth from buying, selling, and renting out properties throughout their lifetime. For the Baby Boomer (and some Gen Xers) generation Real Estate was a great source of wealth accumulation.

For this generation, this was one large funding source for their retirement. Whether that was through rental income or the sale of a second property or downsizing or even a reverse mortgage, they were able to resource this built up equity to help fund retirement.

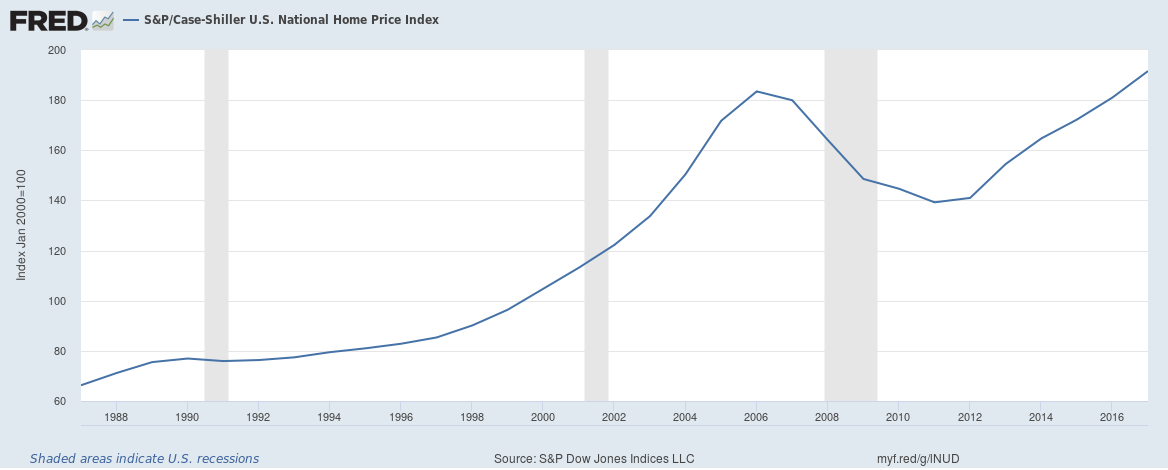

Take a look at this chart of real estate prices from 1987 to 2017:

Source: Federal Reserve Economic Data

Source: Federal Reserve Economic Data

Yes, you can see the large dip created by the financial crisis in 2007-2008, but still, the zoomed-out result (1987 – 2017) is a slope up and to the right. This means that the Baby Boomers and some Gen Xers definitely benefited from the compounding growth associated with real estate.

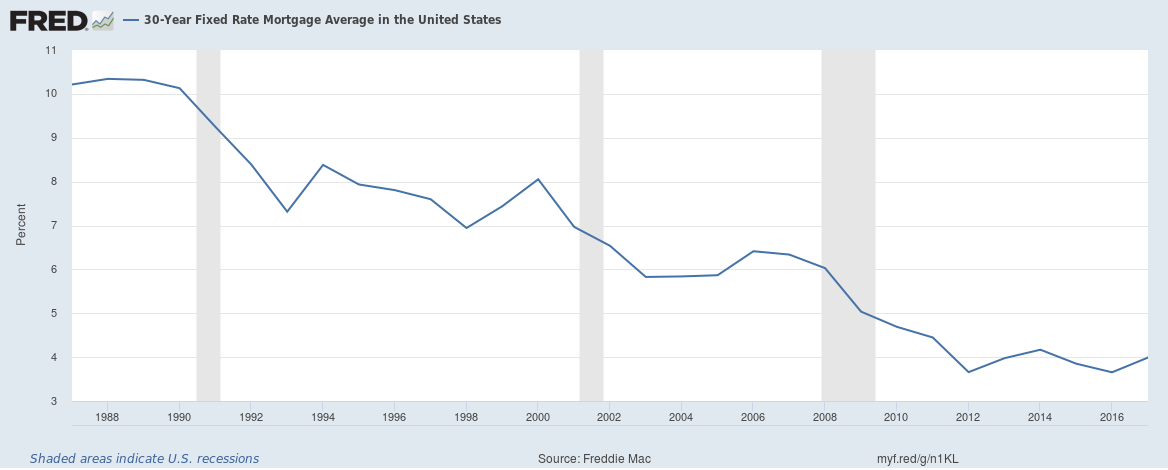

Were their factors unique to this generation that caused this real estate tide to rise? Yes, I believe so. Here is a chart of 30-year fixed mortgage rates for that same time period:

Source: Federal Reserve Economic Data

Source: Federal Reserve Economic Data

The general theme of this graph is a slope down and to the right, perhaps the inverse of our previous chart? I think that’d be a fair assessment. Falling interest rates have provided a tailwind to the appreciation of real estate assets. This chart shows a peak in the late ’80s of approximately 10% to a rate today of around 4%. This is a 6% drop and based on our current base of 4%, we just don’t have that same runway to provide that same drop to provide that same tailwind to property values.

The Inheritance Generation

According to CNBC, “The biggest wealth transfer in history is about to happen… It’s estimated that 45 million U.S. households will transfer $68 trillion in wealth over the next 25 years…” The report goes on to discuss that the Baby Boomers are the wealthiest generation in American history and these assets will be passed down over the next few decades.

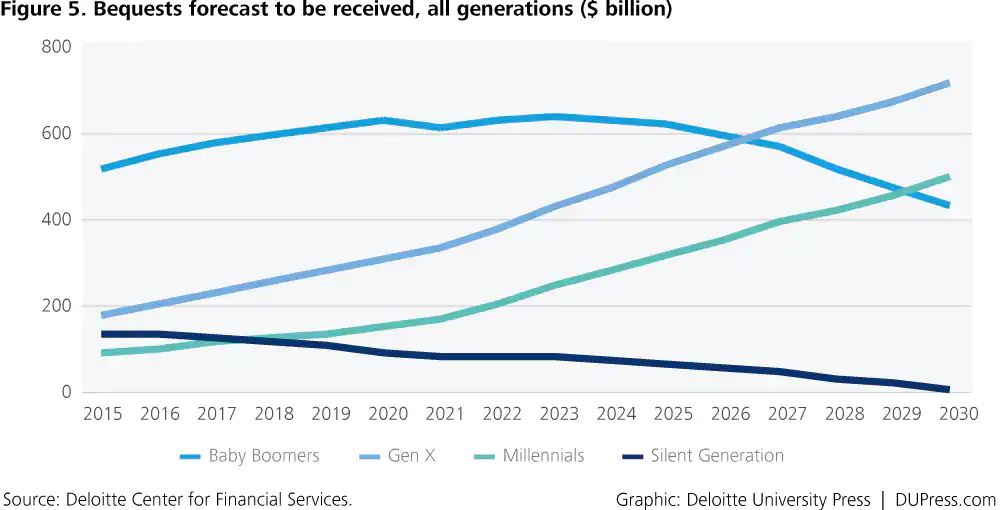

This study from Deloitte provides a great depiction of this transfer across generations:

Source: Deloitte

Source: Deloitte

Gen X may not have had the same access to pensions as the generation before and some may not have been gifted with the ideal timing for purchasing real estate, but this may not matter one bit. This pending wealth transfer may just overshadow those other retirement funding sources from generations past.

Is there a chance this wealth will trickle down to future generations too? To some extent, but many Gen Xers are approaching retirement underfunded, many of them will live longer lives than generations past, and many of them will have elevated medical expenses like long term care. Another factor that is revealing itself is the responsibility that this generation will have for their aging parents and their adult children – Kimberlee Davis, a partner at The Bahnsen Group, wrote a GREAT piece on this exact subject, Blindsided by Being Sandwiched!

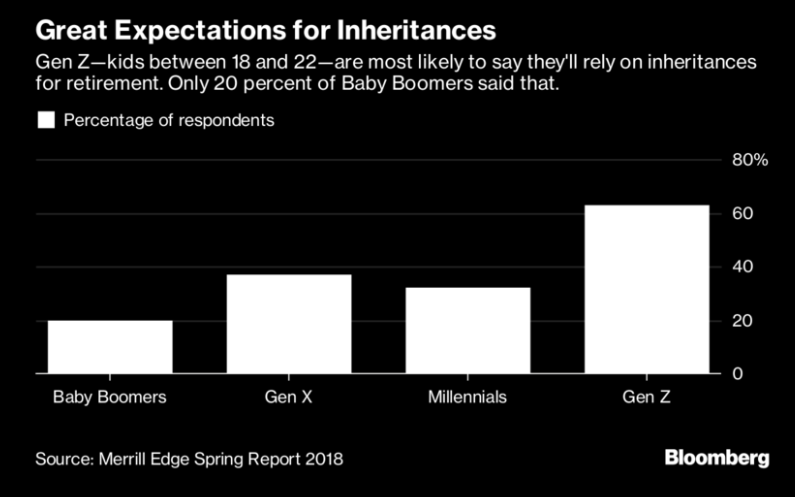

It would be difficult to calculate exactly how much will be left for Millennials and Gen Z, but I assume that the expectation may be greater than the actual outcome. This survey from Merrill Lynch really helps to reflect these potentially disconnected expectations:

Source: Merrill Lynch

Source: Merrill Lynch

The Next Generation

So where does this leave the next generation, the Millennials, and Gen Xers?

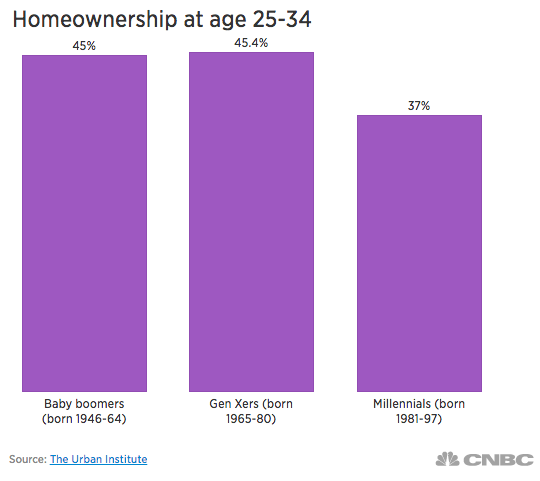

We know that pensions are almost a thing of the past for the private sector, so we can consider that a non-factor. How about real estate? Perhaps it won’t have the same track record it has in the past, but could it be a contributing factor for growing at least some retirement wealth? It could, but this generation just isn’t purchasing homes like the generations that preceded it:

Source: CNBC

Source: CNBC

And although our former survey shows that there is a great expectation for a potential inheritance, this isn’t something this generation should rely on for retirement. Add onto this that many financial pundits are forecasting future return expectations that are lower than historical averages and we can conclude that this generation definitely needs to prepare itself.

So, what is the answer? This generation must take ownership. They must plan, and they must save. The biggest resource they have going for them is time. Time is the number one ingredient for compounding, in order for your interest to earn interest you need time. A simple and well-crafted plan created today around savings targets, investment strategies, cash flow planning, and the such could be the difference between a comfortable retirement and a non-existent one.

Sometimes it’s hard for previous generations to advise and counsel their kids or grandkids on how to build wealth because they rely on what worked for them even though these strategies are not always transferable across time. So, although grandpa may have worked for the same company for 40 years and they took care of him until the day he passed, this might not be the right plan for you. Although mom and dad built up a sizable real estate portfolio that prepared them for retirement, this might not be the right plan for you. And although you might have a great mentor who was the beneficiary to some sizable family wealth, this might not be the right plan for you.

The right advice isn’t so much a strategy or a particular investment, but it’s rather some simple truths that have stood the test of time – spend less than you make, save often and always, manage your risks, and have a plan.