I love the truth.

I value the truth.

I really do appreciate the plain and simple truth.

Let me give you an example. My wife and I always enjoy trying new restaurants, which is both an adventure and a risk at times. When approaching a new menu, it can be overwhelming – lots of options. There is also a curiosity of what is that one really a special item you must try. I love, I value, and I really do appreciate it when the waiter or waitress will tell me what they like to order or what to stay away from, or even the honesty if they haven’t tried a certain item or if a certain item is rarely ordered. This type of candor and culinary conviction is rare and valuable (for a foodie).

The discussion above is simply relating to what tickles my taste buds and warms my belly. One really ought to expect a lot more when it concerns personal finances.

But…

Where is someone to go if they are looking for candor and conviction? Said another way, what breeds candor and conviction? Experience and knowledge. So, let me tell you about a time in my career when I was lacking both.

I can’t emphasize enough how difficult it is to promote yourself as a financial advisor when the ink is still drying on your business cards. At the onset of your career, you literally have zero experience, a very shallow well of education, and little to no application of that knowledge. A scary place to be; I remember it well.

Here’s the hardest part, every common investor mistake or mishap that I try to address here on Thoughts On Money are the same types of obstacles and distractions a brand new practitioner will face. Why? Because our young-aspiring-hypothetical-advisor has not laid the foundation of an investment/planning philosophy and lacks the convictions needed to accompany that philosophy. The world of finance is full of distractions, and a new practitioner is a victim of those distractions just as much as any other investor.

Being new to the industry and the advisory practice means you (1) must learn the language of finance, including all the acronyms, short-hand, and slang terms, and (2) gain a grasp on the wide array of financial products out there. In this learning process, it is very common for a young advisor to become enamored with certain financial products and shortcut the financial plan to pitch a product instead.

I remember my first time learning about structured products. These are products that are typically issued by a bank (as a note) and have defined outcomes that are linked to an index or specific investment. Structured products often come with some other bells and whistles that draw a lot of curb appeal – protection on the downside, etc.

Again, being new, some of your greatest fears are that your clients’ assets would decrease in value, that they’d get upset with you, and even potentially fire you. The allure of safety in some of these structured products, along with the healthy compensation for selling them, make them quite popular amongst new advisors. An advisor is not yet mature enough in their craft to realize that their value is in helping clients endure volatility for the long-term rewards it generates for the investor.

My intent today is not to criticize structured products or provide feedback/analysis on this pocket of the financial products market, although I could. I simply want you to recognize the appeal these have for a fresh set of eyes – whether that be an advisor or client – and how perhaps the pitch might not match the punch.

Let’s make up our own hypothetical structured product to give you an idea of why this product can catch a lot of eyeballs and curiosity. Here’s our fictitious descriptor – a product that tracks the performance of the S&P 500, but it protects you from ever having a negative year, and it caps the returns on the upside to 8%. At first glance, this can seem too good to be true. Some investors avoid the stock market because of the motion sickness the volatility causes them. So, they become captivated by the idea of participating in some of the upside and avoiding all the downside.

This is where our assumptions can get us in a little bit of trouble. We can’t do the mental computation to decipher if the capped upside in exchange for the protected downside is a good trade. I am going to provide some real numbers to help you see under the hood a bit, but let me give you a simple answer, this is not a good trade if your expectation is to generate equity-like returns. I know some structured product advocates out there has a rebuttal ready for me that these products offer diversification and are meant to be a hybrid between one’s stock and bond allocation. I do appreciate the rebuttal here, but let me tell you that when I first saw a promoted product like this, I absolutely assumed that I would be able to have my cake and eat it, too – I thought I was getting all the upside of the stock market with none of the downside. This was an easy assumption to make because I figured the stock market always averaged close to 8% (over long periods), so if I could grab that 8% and turn all my negative years into flat years, it seemed like I’d actually come out on top.

So, let’s go to the videotape…

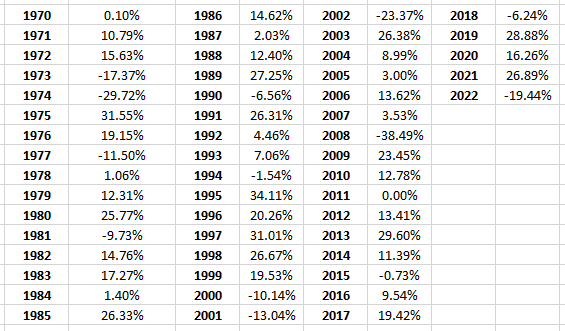

Here is the price return (important note here, these index-linked products often only include the change in price, not the dividend) on the S&P 500 going back to 1970:

*for illustrative purposes only

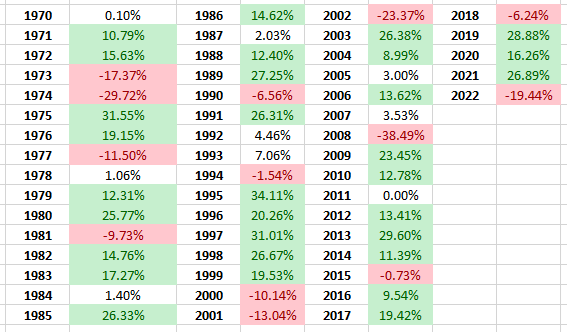

Now, we need to highlight any year where the return was above 8% (green) and below 0% (red) because those are the years that this fictitious structured product would’ve modified the return:

*for illustrative purposes only

A good visual to note here is that there are a lot more green highlights than red highlights, so you are starting to get an idea of who that trade favors.

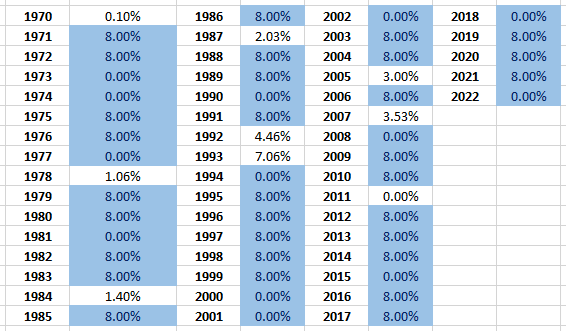

Here is the modified return sequence of our fictitious structured product (I highlighted each modified year in blue):

*for illustrative purposes only

If you calculated the compounded annual growth rate on these two strategies (before fees) – S&P 500 including dividends vs. our fictitious structured product – the difference was roughly 10.4% for the index and 5% for the structured product. Although at face value it looks like you captured half the return, when you compound these figures over these 53 years, our make-believe structured product grew a $100,000 initial investment to $1,356,426, and the index we compared it to grew that same $100,000 to $19,188,950. Now, I don’t believe this disparity in outcomes creates fault (or blame) to the finance industry for creating a product like this, but rather this is simply the cost of transferring what you (the consumer) saw as risk to the proprietor of these products (the banks).

I hope those outcomes were surprising to you, as they were for me young in my career and still today. Here is the truth or lesson you want to draw from here:

- Yes, down markets are excruciating but they are rare compared to when markets (historically) have exploded to the upside.

- Yes, behavioral economics has taught us that “the pain of losing is psychologically about twice as powerful as the pleasure of gaining” (BehavioralEconomics.com – Kahneman & Tversky, 1979) but trading the upside of markets for protecting the downside comes at a real price.

For me, I think exercises like this remind me to slow down and always do the math. If you are a friend of mine, you know how I am wired. I have a bent toward doubt, so I always like to look under the hood and inspect further. Sure, this trait can make me a frustrating person to collaborate with at times, but when managing my personal finances, and advising others, it’s been more of a feature than a bug.

As I mentioned earlier, whether you are a new advisor or a seasoned investor you need to be cautious of all the distractions the finance industry is ready to throw your way. This industry produces the products that the customers say they want, regardless of whether these desires are in the best interest of the consumer purchasing them. If it seems too good to be true, let me help you out, it probably is too good to be true. As much as we despise volatility, it’s that very volatility to the upside that drives long-term wealth accumulation. So much of investor maturity is based on your ability to reframe and retrain your brain on how you react to that volatility. And that is exactly what I am here for, to remind you of that simple truth week in and week out 😊