From Bonds to Stocks

Last week we had a discussion about what drives bond prices. So, it would only be appropriate to follow up that conversation with a discussion on what drives stock prices. This may seem like a difficult topic to tackle, but I bet you will be surprised by how simple the answer actually is.

The Bottom Line

What does it mean when someone asks you, “what’s the bottom line?” It typically means they want you to cut through all the fluff and give them the facts. They want the most important information; they want to know the stuff that matters.

Although this idiom has become commonplace in our everyday language, it’s important to remember where it came from. The literal meaning is the bottom line of a profit and loss statement. The bottom line is the row that provides the numerical value of that particular companies profits or earnings.

So, what’s the bottom line? Earnings.

The Noise

Again, the trigger for this “bottom line” question is usually because someone wants to tune out all the noise and begin to collect all the key details. When it comes to markets and investing there is lots of noise. It’s difficult to know what matters and what doesn’t. Think about everything that’s going on in the world just right now: the trade war, potential fed rate cuts, looming fears of recession, inverted yield curve, Brexit, Presidential Tweets, etc. etc. etc.

Some of these issues/headlines will surely create ripples that will be felt within an investor’s portfolio. Some will not. Some will be disruptive today but won’t even be remembered in the future. Although the noise can capture our attention, we should really be asking, “what’s the bottom line?”

Earnings

The late Benjamin Graham was a finance professor at Columbia University, author of the bestselling value investing book, The Intelligent Investor, and perhaps most well known for his mentorship of billionaire Warren Buffett. One of Graham’s oft-quoted adages is, “In the short run, the market is a voting machine, but in the long run, it is a weighing machine.” The truth that Graham was trying to get at, is that in the short run our emotions – the general sentiment of market participants – drive stock prices, but in the long run business fundamentals are all that matter. A voting machine representing a mechanism that collects opinions and a weighing machine one that reflects facts.

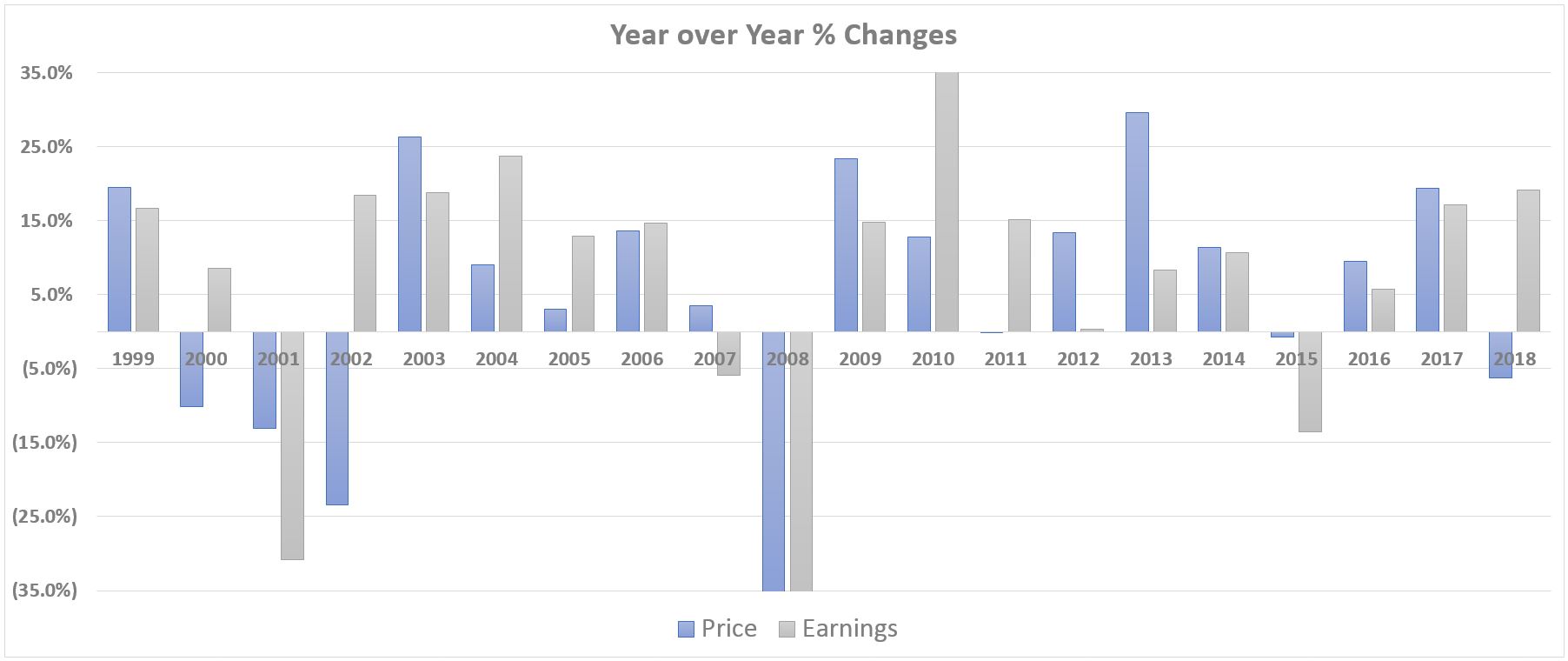

Here is an easy example of how this plays out. Since 1960, companies within the S&P 500 have grown their earnings by approximately 6.8% per annum. Over that same time period, the average stock price of those companies has grown by 6.6%. This near-perfect correlation represents this idea that in the long run stocks are a “weighing machine” and they are weighing value based on profits (earnings).

Now although this correlation holds strong when we are looking at a large enough sample size (let’s say ≈ 10 years), you can see from the graph below that this relationship can disconnect on a year to year basis. This chart that I created provides the year over year change in price (blue) and earnings (grey) of the S&P 500 over the last 20 years.

Voting Machine

The question we posed today was what drives stock prices? Stock prices are driven by profits. But, just as Graham alluded to, these rules change when you shorten the time horizon.

Here is why this matters to you. At some point in your investing lifetime, you will be drawn to a particular investment, strategy, philosophy, pitch, etc. and if you don’t have a basic foundation for how things are valued, you might find yourself learning an expensive lesson.

Take a look at this chart of the last 25 years of P/E ratios for the S&P 500. This is a simple ratio, it just represents how many dollars an investor is paying (P) for every dollar of earnings (E) that these companies are producing.

Source: JPMorgan

Do you notice where this ratio peaks? That’s the tech bubble. A time when investors began to disconnect from the bottom line and they started to be wooed by the noise. They got excited about the potential of owning the next big thing and they began to pay more in stock price (P) for less earnings (E). Many of these companies had no profits to even speak of, they were more of an idea than a business.

Takeaways

So, next time you get excited about a new potential investment, I’d encourage you to revert back to this truth about how stocks are valued. Make sure you aren’t falling more in love with the story than the fundamentals. This should help to avoid a common trap many investors walk into. Just because you love the company or the product, doesn’t mean that the stock price and the underlying details of the company are just as loveable. There is such a thing as a good well-run company, that’s a bad investment.

And that’s it. In approximately 900 words you learned what drives stock prices: earnings. Simple, right? Well, the difficult part is identifying those companies that are able to sustainably grow their earnings over long periods. If we knew the earnings results beforehand, we’d be excellent investors, but unfortunately, that’s not reality. Perhaps a topic for a future TOM discussion, “what drives earnings.”

Until next time…