If you were to do an internet search on “retirement statistics” you would get a plethora of depressing results about how Americans are ill-prepared for retirement. Earlier this year the Ways and Means Committee presented their solution to improve the landscape for retirement savers via the SECURE (Setting Every Community Up for Retirement Enhancement) Act. The SECURE Act is a proposal to modify some of our current laws regarding retirement plans, with a focus on growing retirement participation and engagement amongst Americans.

What is being deemed a nationwide retirement crisis all stems from a quiet baton pass of what was traditionally an employee benefit that companies offered to attract and retain quality workers, to what is now more often the sole responsibility of the laborer. Companies have been transitioning from pension plans (defined benefits) to 401(k) plans and other defined-contribution plans, creating this seismic shift in responsibility.

The SECURE Act has gained clear, bipartisan support as it passed in the House with a 417-3 vote. This proposed Act still has a ways to go before coming to fruition and there is a good chance that the original proposal will be modified and edited prior to finalization. The Senate has also presented a similar bill, RESA (Retirement Enhancement Securities Act) and many believe that parts from each proposal will find their way into a modified final version.

With all that said, what does this mean to you?

Today we will take a closer look at a handful of the proposed changes within the SECURE Act and discuss how these changes could affect you and your retirement plans.

1) Increasing the RMD Age & Removing Contribution Age Limits

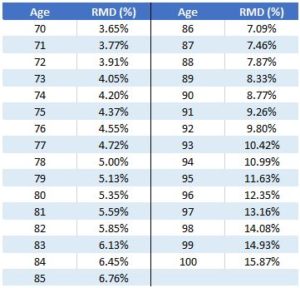

The SECURE Act proposes moving the Required Minimum Distribution (RMD) age from 70 ½ to the age of 72. The RMD is an IRS mandated requirement that a traditional IRA owner is required to take minimum distributions from their account. These distributions, as a percentage, increase as the retiree ages and the distributions are treated as taxable income. This is what those Required Minimum Distributions look like in percentage terms, by age:

Source: IRS

If your initial response is that it doesn’t seem like a big deal that the RMD age changes just a year and a half, you might be missing the point. The RMD age has stayed unchanged since the 1960s and this proposed increase could set precedent for future adjustments as well. People are living longer and working longer and this change would be a step in the right direction. Additionally, for retirees engaging in tax planning strategies like Roth conversions, this extension could prove to be favorable as well. (The RESA Bill from the senate proposed moving the RMD to age 75)

The SECURE act also proposes removing the contribution age limits on traditional IRAs. As it currently stands, an individual is not able to contribute to a traditional IRA past the age of 70 ½. A Roth IRA coincidentally does not have the same limitation, so the SECURE act would remove this limitation going forward. Perhaps not a big deal for most, but it is a signaling from Uncle Sam that more folks are likely to continue working into their 70s.

2) Offering Incentives & New 401(k) Solutions for Small Businesses

As discussed above, there is a saddening statistic on the growing number of people who don’t have access to retirement plans at work. The SECURE Act is working to remove said barriers by offering incentivized solutions to help companies establish new retirement plans to reverse this trend.

The proposed idea is to overhaul a handful of the current retirement rules to allow employers to co-participate in retirement plans that span across multiple employers.

It has always been difficult for small businesses, due to a smaller pool of plan contributors (employees), to find an affordable solution for both the business and the worker. The idea of pooling a larger group of people beyond that of just one small business appears to be a logical and viable solution but we’ll have to wait and see how the mechanics behind this new “sharing plan” play out.

Section 104 of the Act also proposes a new tax credit for employers that have automatic enrollment plans. In 2006 when The Pension Protection Act was put in place, we saw a big uptick in retirement plan engagement through innovations like automatic enrollment, target-date funds, and automatic savings escalation. This tax incentive is intended to spur on those same results.

3) Lifetime Income Disclosure & Annuity Options

The attractive part about pensions is that they’ve always been fairly simple to understand. Once an employee transitioned from working to retirement, they would have a guaranteed fix income for the rest of their life. Yes, there are some nuances regarding how these income amounts are calculated or how the cost of living adjustments are applied, but from the employees perspective, it was a seamless transition from employment to retirement.

The SECURE Act seeks to help bring back some clarity around what a modern retiree should expect for retirement income. The Act requires defined contribution plans (think 401(k)) to disclose the estimated future retirement income based on the lump sum balance in retirement. It’s not clear on how this will be calculated yet, but the Act would include a methodology for presenting this to the participant. The intention is to help retirees understand what their nest egg would likely produce in the form of future income (Lifetime Income Disclosure). My assumption is that this will be an income number that is close to 4% of the lump sum value, meaning that it would be sustainable (with the right investment allocation) to spend at this rate without running out of money.

The Act also proposed that these defined contribution plans offer annuity products. Meaning the plan would offer an investment that would allow a retiree to convert a lump sum into lifetime income. It seems as if Capitol Hill is really pushing for these income products – I assume it is because of their perceived similarities to a pension – but I believe that this will also lead to some unintended consequences. Remember, if you are exchanging for a “guarantee” you are giving something up as well, i.e., access to your funds, potential growth, inflation protection, etc. Not to mention that many of the current annuity products offered are very expensive. It will be interesting to see how this all plays out.

4) The Death of the Stretch IRA

We will end off with perhaps the most criticized component of the SECURE Act, Section 401. Last week, The Wall Street Journal had a scathing opinion piece on Section 401, titled, Congress Is Coming for Your IRA.

Here’s a basic breakdown, currently when you inherit an IRA as a non-spouse you are able to “stretch” the distributions over your own life expectancy. The proposed change would be to have these distributions (remember, taxable income) take place over a 10-year time frame. For some, this will mean inheriting a BIG tax bill. Just imagine an individual in their peak earning years inheriting a sizable retirement account and then having forced distributions in the top tax bracket. The backlash is valid, and most critics believe that this section will see significant modifications. If not though, this will mean that some additional tax planning around spending and converting these assets could make a sizable difference to the future benefactors.

There’s Always More …

Today I gave you some basic highlights and what I would define as the “need-to-knows.” If you wish to know more, you can find more details here in this abridged version from the House Ways and Means Committee website.

As I mentioned earlier, at this stage, the SECURE Act is just a proposal on the table. Who knows what the final version will look like or how long this will take to reach approval. What I find most interesting is how these proposed solutions are crafted. The intention is to try to solve a retirement crisis in the United States, yet I do not believe that these slight tweaks and modifications will be the needle mover to help us change course meaningfully. Though I do believe that investors need to be privy to these changes so that they can efficiently steer their financial plans based on the everchanging environment.

And this is what brings a financial planner the greatest joy – the duty and responsibility of helping their clients navigates the new challenges and obstacles as they arise.

That happens to be what I do. Please feel free to reach out to me with any questions as I know these kinds of articles can be hard to understand, especially when our legislators get involved, right? Thanks again for reading Thoughts on Money!