Here on TOM, we spend a fair amount of time talking about common mistakes that investors tend to make or particular approaches to avoid or planning strategies to implement, but I thought it might be a good idea to talk about WHY we do it. An old boss would always ask me, “What’s the why behind the what?” or to rephrase, “why are we doing this?” Much of the guidance that TOM provides is intended to help mature folks into long term investors that can weather the day to day challenges that we all face. Today we will talk about the reward waiting for those that are able to endure and stay the course – compounding interest. And what an astonishing reward it is!

Patience is a Virtue

The idea behind today’s entry was spawned from a recent review I did. A friend sent me some account statements to look over and asked for some feedback. What caught my attention when looking over the statement, was that most of the mutual funds she owned had been held for quite a long time. This is a rarity these days, as many folks are constantly turning over their portfolio, transferring assets, switching approaches, looking to buy the next hot thing, and so on and so on. My friend was a patient investor and had a track record of staying the course. This made me smile, I was proud of her.

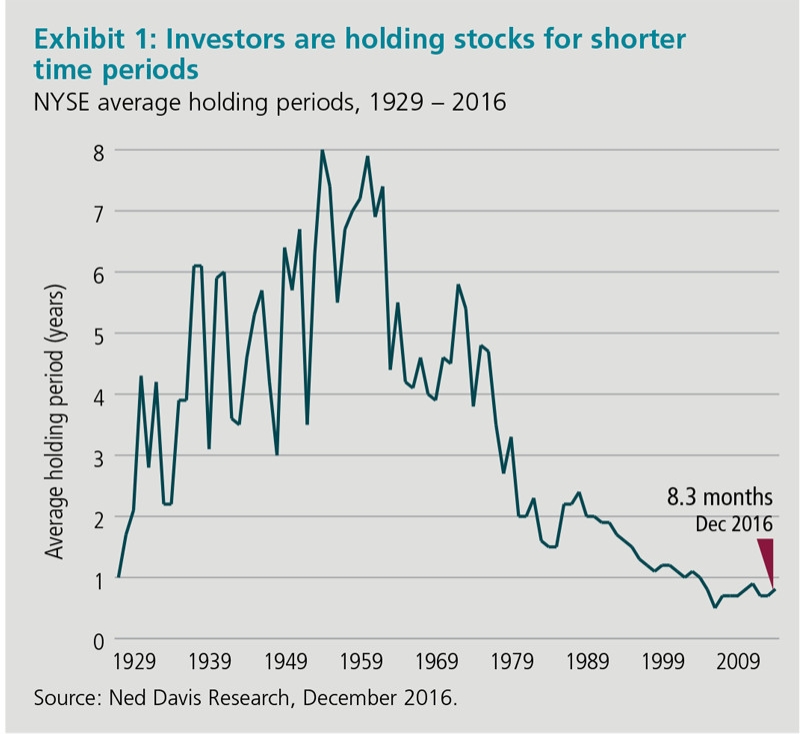

Ok, a quick pause for a fun fact, check out the historical holding period for stocks:

(https://www.mfs.com/content/en_us/mfs-insights/lengthening-the-investment-time-horizon.html)

Our forefathers of the ’50s held stock on average for about 8 years and the short-attention-span-generation of today clocks in at about 8 months – from 8 years to 8 months in a handful of decades. Oh my, the times they are a-changin’… ok, back to our story.

The Eighth Wonder of the World

My favorite part about my friends accounts statement was a small box on page 1 titled Portfolio Rate of Return. This small graphic provided her rate of return over the last 15 years which was something around 11%. No money had been added, but the annualized return on the investment was 11% and that my friend is impressive! Truly, it is absolutely stunning!

Now, let me clarify, I wasn’t astounded by this because of its performance versus a benchmark or anything like that. I just knew what 11% over 15 years will do to a nest egg. Imagine one of those old cartoons with the snowball rolling down the hill – it’s something like that. Albert Einstein said it aptly calling compound interest the “eighth wonder of the world.”

(Calvin & Hobbes)

In finance we have an easy back of the napkin math trick to help conceptualize the impact of compounding interest, it’s called the rule of 72. Just take the number 72 and divide it by your annualized return and that provides an approximation for how many years it takes to double your investment. Let’s try it out – 72 divided by 11 equals about 6.5, so an investment growing at 11% doubles about every 6.5 years. For fun, let’s say my friend originally invested $100,000 in 2003, this means mid-2009 it would’ve been about $200,000, 2016 approximately $400,000, and if things continued on at this rate, come 2020 that’d be in the ballpark of $800,000. Again, this is a back of the napkin trick, intended to get us close, but not exact. Nonetheless, $100,000 gets parked in an investment, no money is added, and come 20 years later it’s worth eight times more – WOW!

Now for a Parable

Ok, maybe the Einstein quote didn’t make you a believer. Maybe the story I shared wasn’t as jaw-dropping for you as it was for me. Maybe the rule of 72 quick math just didn’t do it for you. How about a parable?

I came across this short story quite some time ago and it really helped to solidify the power of compounding for me. The story went something like this: A man had invented a new game, the game of chess, and he had traveled to India to present it to the emperor. The emperor was so pleased with the game that he told the young inventor that he could name his reward. The inventor’s reply was simple yet odd, he requested that the emperor grant him 1 grain of rice for the first square of the board, 2 grains for the second, 4 for the third, and a continuous double portion for each of the 64 squares. The emperor agreed and was taken back by the minimal request and tasked his treasurer to arrange payment. Sometime later the treasurer returned with a distraught look on his face and informed the emperor that there was not enough rice in all the kingdom to meet this request. The treasurer calculated that this payment would be impossible to fulfill, even over centuries. [18,446,744,073,709,551,615 grains ~ 210 billion tons]

I’ve often heard this fable coupled with the story of the doubling penny, same concept but someone starts by giving you a penny on day one and then double the amount each day for 30 days. Here’s what that looks like:

One penny turns into $5 million just 30 days later.

Ok, Back to Reality

Here’s the thing, you and I both know that we are not going to turn a penny into five million dollars over 30 days. We also know that we are never going to have that much rice but the concept stands true. Compounding interest is an fascinating thing – and math works! My friend is living proof and we should take note of her patience. She devised a plan to be a long-term investor, made her initial investment, and then was patient to let compounding do what compounding does.

As we often discuss, everything around you will try to knock you off your plan and get you sidetracked, so you will have to remind yourself of the rewards waiting for a long-term investor. Let’s end with this last video clip that I always enjoy and see what a $1 in the stock market over time looks like, even with all the potentially distracting headlines along the way. My hope is that these real-life stories, fables, math examples, and this video will all be branded into your memory as a reminder of the power of compounding.

Enjoy!