The big idea and why it matters: Investing in real estate is far from a sure thing. Like many other businesses or investments, the less one knows about it, the more it appears to be a) easy, b) passive, and c) risk-free. However, that is not the case, and people often get in over their heads or lose money in such situations. Buyer beware.

“Real estate is a contact sport.” -Tracey Hampson (realtor)

For the first time in Alt Blend history, today’s quote may not be from someone with their own Wikipedia page, but it perfectly captures what we’ll cover today. This topic has been on the back-burner for over a month as we finished the recent series on crypto updates. While we’ve arrived at this topic independently, David Bahnsen recently released a Capital Record podcast titled “An Investment You Pay Money to Own?” (hint: it’s real estate), which I encourage you to listen to.

My desire to dedicate a blog post to the practicalities of real estate is due to recent conversations I’ve had with clients, prospective clients, and others about the real experience of property ownership (or, in one case, a complete lack of understanding of how real estate works). It will be fun, exciting, and, well, real (you’re welcome). Here we go!

Real estate isn’t magic.

I had a recent conversation with a neighbor that was simultaneously enlightening and something I tried to escape for the entire fifteen minutes from the moment it started on the sidelines of my daughter’s softball event. That dialog went something like this:

The neighbor, whom I’ll call “Jen,” told me how she knows a lady who is rich because she “does commercial real estate.” You see where this is going. Jen’s conclusion was that she could easily replicate her friend’s success and enjoy the ample “passive income” that comes with it. And why not? Jen just doubled the value of her home in recent years, and that was so easy; clearly, she’s pretty “good at” real estate already, right? All she’ll have to do is buy a building and watch the money roll in. To Jen’s credit, she did identify one problem: commercial buildings are so expensive that she’d need to pool together some funds from other people she knows so they could all pitch in and buy property.

Bad neighbor?

Sorry if I’m not a supportive neighbor, but my immediate feedback focused entirely on the countless flaws of Jen’s analysis, some of which were:

- Jen’s friend is not just collecting passive income. If she is, it’s only because of (likely) decades of building a real estate portfolio that is successful enough to have a team (or teams) in place that can run all of the day-to-day management. Or, to be fair, Jen is unaware of the time and effort her friend still puts into her properties (knowing many entrepreneurs, my guess is it’s the latter).

- Her friend also acquired properties during a historic low-interest-rate environment that no longer exists; this makes the current math of buying a property nearly impossible to generate positive cash flow.

- There is a whole business (ever heard of private equity real estate?) that raises capital from investors to pool money to buy, improve, manage, and attempt to profit from commercial real estate. It also truly provides end-investors with passive income. And many of those managers with professional experience have failed – even in the low-rate environment I previously mentioned.

If you’re up for structuring a business entity, have a network of people who are willing to risk their capital with you, possess the know-how and resources to fix, improve, and operate properties, and enjoy the capacity to dedicate significant time and effort (let’s call it a “full-time passive income job”) – PLUS the ability to absorb utter failure of this business venture – then, by all means, go for it. Otherwise, stick to your day job, save, and leave such things to professionals.

How do things go wrong?

In short, expectations can ultimately vary from reality. The process of assessing risks and anticipated outcomes of a given project is known as underwriting. But real life doesn’t always play out how one would theoretically hope when it is underwritten. Better investors tend to use conservative estimates and do their best to account for unexpected issues, but it’s impossible to account for all unknowns. Here are some examples:

- Low Occupancy: Tenants leave their dwellings (apartments, offices, warehouses, restaurants, storefronts, etc.), and replacements cannot be found (i.e., a problem of low occupancy). Lower rents => lower cashflows => lower property value.

- Low Rent: Tenants who were originally expected to leave their rent-controlled apartments stay for longer than expected – or it’s otherwise too costly to get rid of them. Or, perhaps the market changes (e.g., NYC during Covid), causing market rents to fall substantially. Again, lower rents => lower cashflows => lower property value.

- Regulatory or Delays: aside from rent-control & occupancy issues, zoning restrictions/changes, and permitting problems, or other delays can all impact profitability. Internal rates of return (IRRs) suffer if projects take longer – not to mention debt has to be serviced for an extended period, perhaps from cashflows that don’t fully support the payments.

- Financial: Interest-rate changes affect real estate valuations. Rising rates mean generally lower property values and also higher borrowing costs (double whammy!). Fixed vs. adjustable debt can have very different implications on outcomes.

Of course, if any of the above items go better than expected, it can lead to more positive outcomes, but “hoping things go well” isn’t a strategy (hence our passion for Dividend Growth investing).

Reality check: Anecdotes

When my family moved to North Bergen, NJ, in 2013, we rented the first floor of a 2-story home from a gentleman named Mike. After purchasing the property as a local resident, Mike had since moved about 90 minutes away from the area, but he was still there many weekends tending to the property. He often told me that being a landlord was not what he imagined (not in a good way), and ultimately, he was trying to sell the property at a loss vs. what he’d originally put into it just to move on with his life.

The next owner, Rob, also didn’t live in the area but decided to do a full renovation of the top-floor apartment, expecting that he, his wife, and their newborn child would move in. Then they’d have the landlord’s dream: live upstairs and rent to a good downstairs tenant who would pay for most of their mortgage. Rob completed the renovation (at least $75k is a fair cost estimate), never moved in, never rented the top floor, and sold it for about $140k more than it was purchased for. Absolutely a loss once you factor in carrying costs and transaction costs (both buying and selling).

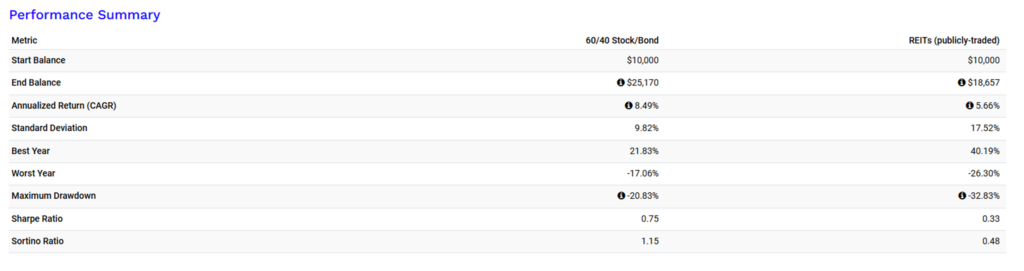

Others I know have owned a condo outside of Washington D.C. since 2013, which was purchased in cash. Fortunately, this is in a building, so their day-to-day involvement has been limited – not 100% passive, but likely as close as one could hope to get. The local economy has been great (the area is inundated with gov’t employees with very consistent employment). The interest-rate environment offered low rates and even moved lower for years – offering them the opportunity to take debt against the property (they did not) and potentially spur some price appreciation. Then you have Covid, which pushed property prices in many locales to new all-time highs. Aside from the more recent rising rates, it’s close to a dream scenario if one could have drawn it up. The outcome? The property has generated a net operating income of about 3% (yield) per year, and its value is…wait for it…about the same as the purchase price 10+ years ago. On top of that, about 40% of the sale price will now be taxable as ordinary income because of depreciation recapture.

Just for fun, had the above investor instead held a standard 60/40 portfolio or even publicly-traded REITs (real-estate income trusts), they would have had to endure greater volatility, BUT would have come away with annualized returns that were nearly 2-3 times as much (again, that’s per year). See the below chart for details.

*Source: Portfolio Visualizer

And perhaps I’ve found the only two families who have such a story to tell, but I recently spoke with another couple who have had a similar experience with a property in Connecticut. Everything seems to have gone in their favor except the value of the property.

Balancing Act

To end on a positive note, I’ve also known a NY-based family who has very successfully owned and operated commercial real estate for generations. They sort of stumbled into it, as a cost-effective warehouse was needed for a textile business, and that prompted a move from Manhattan to (what I’m sure was the far less desirable) Long Island City (LIC). People eventually caught on to LIC as a great location and easy commute to NYC. Property values increased over decades, and it was determined that converting the building to office space was a viable business. The second and third-generation family members have made owning and operating their family commercial building their full-time profession, along with reallocating proceeds in other projects and investment portfolios to continue building wealth. Real estate can be an awesome force in the right circumstances. So, there you have it: Real estate ventures are not always dire!

Closing Transaction

My purpose today is simply a reminder to be aware of what you’re investing in and what needs to occur for it to be a successful investment – whether that’s real estate or anything else. As we’ve covered in our real estate series, property is literally all around us and is such an integral part of our daily lives that it’s easy to view differently. To all of you non-real-estate professionals: the next time you get an itch to be a landlord, just don’t forget there are many risks and a lot of work involved in any project.

Until next time, this is the end of alt.Blend.

Thanks for reading,

Steve