Dear Valued Clients and Friends –

It goes without saying that the news of the day was the U.S./Israeli strike on Iran Friday night/Saturday morning and the continued military endeavor there. Futures dropped overnight but quickly recovered midday today. It is a major geopolitical story, foreign policy story, and human life story (praying for the safety of all Americans), but as for “market impact,” one need not look any further than the bond market today to note the response … instead of a flight to safety (bond yields generally collapse and bond prices rally as people dive into Treasuries looking for a safe haven) we see bond yields up today (not to mention the benign equity market response).

Allow me to quickly say that it is purposeful that my discussion in the Dividend Cafe today of this development centers around market, and economic and energy sector impact. Those wanting a broader military or strategic diagnosis have far better places to go than here. Those who have strong opinions about whether or not this should or should not be happening would not change their mind if I editorialized on that subject, and such editorials are not the objective of the Dividend Cafe. I am sure you understand.

Dividend Cafe on Friday did a deep dive in the [substantial] amount of press related to private credit as of late, arguing that all the talk about AI, investor liquidity, and more affects more people than is commonly understood. I would tell you everything I said, but then I would just end up rewriting the whole thing here. The written version is here (my favorite), the video is here, and the podcast is here.

Off we go …

|

Subscribe on |

Market Action

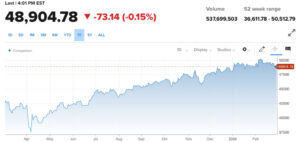

- Markets opened down -500 points this morning and then immediately began going higher. By noon ET, the market was flat on the day.

- The Dow closed -73 (-0.15%) with the S&P 500 +0.04% and the Nasdaq +0.36%

*CNBC, DJIA, March 2, 2026

- I suspect a bigger factor in markets from the military strike in Iran is not the particular implications of the military strike in Iran, per se, but the way in which this uncertainty event adds to already uncertain/pressured circumstances in risk assets. From AI concerns to tariff questions to private credit hysteria to elevated valuations, markets for risk assets are already digesting a lot, and the broader “uncertainty narrative” takes on more weight with a war in the mix (forgive the captain obvious here).

- I do not expect this war to go any way like the 2003 Iraq war did – as in, in no way, shape, or form, do I believe this is going to end up seeming remotely reminiscent of the multi-year operation that became the Iraq war. But that said, even if it were identical, some have mentioned that the Iraq War lasted from 2003-2007, and that the stock market was up +100% during that time (all true). It is as easy as can be to explain the difference: Markets were saved by a three-year bear market when the Iraq War started; markets are now in some of the most elevated valuation conditions on record. Correlation is not causation. And those analogies are fallacious to the core.

- The ten-year bond yield closed today at 4.04%, +8 basis points on the day. This lack of a flight to safety is even more telling than the benign response in the stock market.

- Top-performing sector for the day: Energy (+1.95%)

- Bottom-performing sector for the day: Consumer Staples (-1.35%)

Iran and War

- My general view is that the market response today was reasonably benign, and that the major uncertainty factor going forward is how deep and prolonged U.S. involvement will prove to be. I believe the most likely scenario on that front is that it will prove to be less than some fear, for a plethora of reasons (military, strategic, political, temperamental, etc.).

- An obvious response in the aftermath of the military action in Iran: A big rally in the defense sector today. An also obvious response: A big rally in U.S. energy stocks. A less thought-about but also obvious response: a big rally in liquefied natural gas companies (with much of the Middle East capacity for production on that front currently offline). Now, this may seem like a positive thing for those with long exposure in those sectors … but the problem is, with investing, what seems “obvious” often does not last very long.

Economic Front

- The Producer Price Index (PPI) number on Friday was not good and was surely a major factor in Friday’s market sell-off. A +0.5% increase on the month was much higher than expected, and the +2.9% year-over-year is clearly reflecting the impact from price increases in goods related to tariffs. The reason I isolate goods here is that Energy prices fell and food prices fell … Core goods prices were up a surprising +0.7% for the month. Could this be an anomaly month? Sure. But it was not encouraging.

- On the more encouraging front, ISM Manufacturing was up for the second month in a row (after being negative basically every month of 2025). Prices Paid were higher (not good), but New Orders stayed positive, and 12 of 18 sectors were in the green. That said, manufacturing employment dropped again. The broader expansion across more sectors is a positive. The portion of the move attributed to higher prices paid is a problem.

Housing & Mortgage

- Mortgage applications for new purchases fell on the week, which may be surprising to some since rates dipped below 6% for the first time in forever. But refinance applications did pick up, which makes more sense.

Oil and Energy

- WTI Crude closed at $71.48/barrel, +7.19%. It was up +7% when futures opened last night and +8% this morning.

- Qatar halted LNG production today after Iranian drone attacks.

- Midstream was up +1% last week before the weekend events and was up another ~+2% today. The sector was up +9.5% in February. A lot of the midstream bid today was specific to where there are LNG exposures, as LNG exports became more important with the competition from Middle East LNG production offline.

On Deck

- I am in several different states for meetings and speaking (including two days in our Nashville office) this week and into the weekend, returning to NYC early next week.

Praying for safety for our troops, our unbelievable military, and any U.S. citizens who find themselves abroad in troubled spots. And may God bless America …

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

The Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet.