Dear Valued Clients and Friends,

I kind of like this week’s Dividend Cafe. We are going to do a very quick look into how the Fed fuels Japanification, but more specifically, how low-interest rates hurt growth. It is one thing (and a more severe one at that) that monetary policymakers generally view artificially low rates as a really good thing to fuel economic growth, but at this stage in my life and career, there is little I can do about that. It is another thing altogether that so many investors think is a great thing. Today I want to do a quick lesson on why it is not just wrong but a dangerous fallacy, that is, wait for it, undermining economic growth.

Speaking of growth, many want to know when the Emerging Markets will deliver it. I think you will benefit from that lesson today as well. Unfortunately, the EM gain is likely to be Europe’s pain, so get ready for a case of hot-cold.

And finally, I want to add to last week’s talk about “gross domestic product” in how we think about economic growth. You may find it illuminating.

Jump on into the Dividend Cafe.

|

Subscribe on |

It is not just debt fueling Japanification

I have written time and time again about the reality of low/slow/no growth in the United States being fueled by excessive indebtedness. I don’t want to overstate the point right now, and Dividend Cafe archives are filled with the case.

But when I make the point that Congress and government spending are suffocating future economic growth and that this becomes a vicious cycle going forward, I sin by omission if I do not properly cover the monetary aspect of this Japanification trap. The central bank is involved as well, and today I want to better unpack what this actually looks like.

Interest Rate Vocabulary

First, some basic definitions. The “market rate” is the actual interest rate in the market – what people are actually paying. It could be the Fed Funds rate or a Treasury rate, or a corporate bond yield, but it is some reference to real life.

The “natural rate” is an economist’s attempt to define what the rate “should” be. The Fed refers to a “neutral” rate – a magical spot where rates neither take away from nor add to economic growth. But rather than feign a “neutrality” that I very much doubt exists, we’ll use an extremely practical and empirical way to define a “natural” rate, and that is, the “growth rate of corporate profits.” What could be more real life than that?

Celebrate low-interest rates at your own peril

When the market rate of borrowing is less than the natural rate, the incentive for financial engineering is huge. Borrowing an X to buy something that yields more than X becomes easy. But of course, leveraging incumbent (legacy) assets to capture a spread does not create new assets. It can generate profits (by definition, borrowing at X to buy something yielding more than X is profitable – this is a tautology), but it does not result in new assets, new endeavors, new projects, and new risk. And this creates a structural decline in productivity. So low-interest rates hurt output, or at least interest rates that are “too low.”

What about when the opposite happens? What about when the market rate is higher than the natural rate? Well, first of all, we have to point out that this will happen. In the paradigm described above, a structural decline in productivity will hurt corporate profits (slowing the rate of growth of such). So the natural rate being higher than the market rate creates the conditions for the market rate to become higher than the natural rate. And this becomes the debt-deflation cycle I have written about before (where the attempt to pay down debt leads to an even higher ratio of debt-to-assets/income because assets/income are dropping faster than the debt itself is being paid down). It is the nastiest of economic conditions imaginable, and it is at the very heart of the Great Depression, Japan, the Great Financial Crisis, and in a slower/milder state, the Japanification of the U.S. that I fear.

In all thy getting, get this …

The belief that artificially low rates create growth has, in fact, decimated growth. At issue here is not those moments of recession where the Fed cuts rates for a time; rather, it is in leaving them low for years and years and years. This has created dependencies and distortions that simply make moving above a 0% real interest rate even harder. What is needed is a productive investment. But who needs productive investment when manipulated interest rates create desired profits from an unproductive investment?

Capital being allocated according to the marginal return on invested capital as opposed to the spread between the natural rate and market rate is the need of the hour.

Emerging challenge

So in the U.S. right now, “market” rates are going higher (that is, the interest rate received on Treasuries are instruments denominated by the U.S. dollar). But, the “natural” rate in foreign countries is not going higher

This fosters a liquidity crisis (think of the debt-deflation dynamic described above – a foreign country has borrowed money with U.S. dollars, and the more they pay back, the stronger the dollar gets and the weaker their own economic imbalances become).

This is a very tough dynamic for emerging markets (equities, bonds, currencies).

So what reverses things for Emerging Markets?

Well, what if hypothetically, we get slowing U.S. growth, inflation that comes down but not quickly or dramatically, and the Fed eases up on its tightening in the near future? In that scenario, I have little doubt that the U.S. dollar declines, commodity prices drop, and emerging markets stocks (and bonds, for that matter) perform extremely well.

The challenge right now is that the macro is dictating the returns of EM, yet we believe very much in a strategy centered around the micro.

A relative energy case

A point I would share that I picked up from the great Louis Gave of Gavekal Research … If one believes that access to energy and the cost of accessing energy is going to continue being a problem for Europe (Russia issues and more) and in the U.S. (almost entirely self-induced problems), it is fair to note on a relative basis that many emerging markets economies may not have these same problems, either because they produce themselves, or have no societal pushback against using coal, or because they can buy from Russia in their own currency. This macro trend is very important and an under-appreciated potential catalyst in the EM space.

Emerging’s Case is Europe’s Crisis

As much as this is meant to paint the picture of a potential upside catalyst for emerging markets, I should point out the entirety of Louie’s point here, which is as much European-bearish as anything. When it comes to access to cheap energy, consider the following about the major economic regions:

- North America – has its own production capacity and even the ability to use coal wherever it so desires; but yes, constrained by its own internal constraints

- Japan – has ample nuclear capacity and may very well choose to purchase from Russia

- Asia ex-Japan – does have coal capacity and is happy to buy from Russia (in their own currency, no less)

- But then, Europe – entirely dependent on imports, with most coal mines shut down decades ago. Some countries do have good nuclear capacity, but where oil and gas are needed, there is a high-cost structure that is only going higher

This story is not going away.

Euro has no Energy, either

In July of 2012, Mario Draghi said the European Central Bank would do “whatever it takes” to preserve the Euro. We referred to this as the “bazooka moment”, where essentially a policy declaration was made that if it took the rapid-fire shooting of a bazooka to save the Euro, that’s what they would do. And they did it. Bond spreads that were so wide you could drive a truck through them narrowed. Yields came way down (well, they even went negative, so that sounds terrific). Banks that seemed insolvent did not fail. And no European country actually left the Euro currency, despite the strong temptation in 2012 to do so (that is, for Greece or Italy or other overly-indebted nations to flee the Euro currency and re-denominate their debt in their own currency that they could then weaken as needed).

But a decade later, saying that the crisis of 2012 was averted and that the nation bloc (and its central bank) did triple down on the long-term existence of a shared currency is really about all that can be said. Italy’s debt-to-GDP is now a stunning 150%. A decade ago, it was 120%. The Euro has dropped 30% against the U.S. dollar over the last decade. European banks have not fallen, but they are, shall we say, daily destroyers of capital and continue to lack the ability to heal and grow.

I do believe there was a fork in the road moment in 2012 (real, real long-time listeners may recall my weekly nomenclature about this very subject in my then weekly commentary at Morgan Stanley before the Dividend Café brand had been invented). Had Draghi not pulled out the bazooka and said they would do “whatever it takes,” I think the structural flaws of the whole concept of a shared Euro currency would have overwhelmed continental desires to sustain it. A decade ago, there was overwhelming reason to cut bait. A decade later, with trillions of Euros created out of nothing to buy bonds (and this practice is still going on today), there is no going back. The Euro is held captive by the Fed. And absolutely no good options really exist for what to do.

Is it all Gross to you?

My friend, Mark Skousen, was published in the Wall Street Journal this week discussing the recent hubbub about the definition of a recession and the decline of GDP (gross domestic product). I pointed out in my commentary last week that not only do we lack a concrete definition for what a recession is, but its use of “gross domestic product” is subject to critique, too, since many do not believe that measurement is an ideal encapsulation of real economic health. I pointed out that the NBER does not only rely on GDP though but also on GDI (gross domestic income), which adds up wages and profits, and other income. That number has actually been up the last two quarters (Q1 was up +1.8%, and Q2 will be announced in a week or so but is expected to be up by the same or more). So we have a discrepancy between GDP and GDI, and that is not normal. Just as a strong labor market and a declining GDP are not normal, this current gap between domestic product and domestic income is not normal.

But Skousen has long touted something called “Gross Output” (GO). It measures spending on all stages of production (including the supply chain). Gross Output was up +2% in Q1, and Q2’s number won’t be released until next month. Skousen’s point is that supply chain spending matters and that GDP only measuring finished goods and services are inadequate. Intermediate production, though, is a $20 trillion part of the economy. GDP’s measurement of just 44% of economic activity is inadequate, and the Gross Output measure seeks to remedy this.

Now, I don’t believe mainstream economists (let alone the press) will ever adopt the Gross Output measure when it releases two months later than GDP does. But I wholeheartedly agree with Skousen that Gross Output is a better snapshot of the economy and at least ought to be considered in tandem with GDP and GDI. These are three different measurements, each with their own pros and cons, but in aggregate, they are a great picture of the economic canvas.

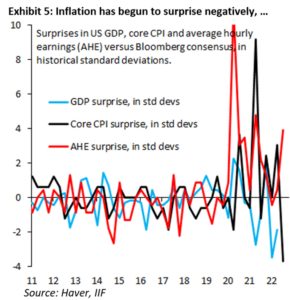

Chart of the Week

I will keep you posted, but …

Quote of the Week

“As a rule, panics do not destroy capital; they merely reveal the extent to which it has been previously destroyed by its betrayal into hopelessly unproductive works.”

~ John Mills (1867)

* * *

I am back in California for a few weeks starting Sunday, and basically counting the days to football, to my daughter starting high school, to the end of summer, and to my favorite time of year (fall, always and forever, fall).

In the meantime, you know how to find me. I’ll be working, reading, writing, managing, stewarding, and producing. It’s my small part towards the cause of economic growth. To that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet