Dear Valued Clients and Friends,

Sometimes it is important to remember that “volatile” is not a synonym for “negative.” Volatility refers to “up and down” movement – directionless – choppy – uncertain. The market turned volatile a couple weeks ago, and the last week of January that included a down 400 point day and a down 600 point day, along with a couple up 100 or 200 point days. The first week of February “volatile” included an up 400+ point day, an up +150 point day, an up +500 point day, and (as of press time Thursday) an up 100 point day (so roughly +1,150 points on the week thus far) … So yes, this is volatile – lots of down volatility last week and lots of up volatility this week.

And of course, this is why “volatility” can’t be traded. It can only be appreciated (if you are thinking through the prism of optimism), or endured (if you use a half-empty glass).

In this week’s Dividend Cafe we do all we need to do to understand the current market volatility, to consider the right portfolio approach to all present state of affairs, and of course to break down one of the most significant political weeks in recent times.

So cozy up, grab a coffee, and join us in the Dividend Cafe!

Just out of curiosity, why are markets up?

I write a lot about why markets do not need an excuse to go down and the same is true about markets going up. I certainly agree that there are moments when the impetus to a sudden move up or down is easy to identify, but there also are moments when the reasoning is subject to highly questionable identification. I do believe fear and uncertainty around coronavirus was a major factor in last week’s downside volatility, but I also believe the flattened yield curve, oil prices, and general market fatigue are good anecdotal explanations.

So what drove things higher this week? For those squarely in the coronavirus camp last week, they must believe the reversal in markets this week happened because of a reversal in coronavirus outlook this week, right? Except there was no such reversal – China remains in a heavy quarantine mode, and significant trade and travel remains on lock-down.

So the best explanation(s) we can offer … (1) Less panic and more rationality took over decision-making as it pertains to coronavirus, even as the world’s greatest scientists working on it have yet to claim victory; (2) The economic data overwhelmed market actors, with the blowout ADP jobs number and the huge reversal in ISM manufacturing giving pause to those expecting a tepid or negative economy in 2020; and (3) Net-net, earnings season is really going pretty darn well …

But then there is this:

Liquid medicine

How do global equity markets rally hundreds of points higher when a disease that was three days earlier supposedly going to bring the world economy to its knees, with no medical progress or situational improvement evident whatsoever?

$174 billion of liquidity – that’s how. Or put in Chinese terms, 1.2 trillion (with a “T”) Yuan … That is how much the Chinese central bank inserted into their financial markets this week.

A crude review

Obviously the broad stock market response to coronavirus fears was most people’s focus over the last two weeks, though some more serious analysts were focused on the impact in fixed income markets as well (bond yields dropped and gave a big boost to fixed income returns in January, offsetting the equity market volatility). But it is oil markets that the impact seems to have been felt most profoundly. Brent Crude was trading at $71 per barrel on January 8, yet hit $54/barrel this week – a 24% drop in just three weeks.

There has been a push-pull tension in oil prices as it pertains to macroeconomic indicators for years now – years – and it has not subsided one bit. On one side, lower oil prices reduces inflation expectations, adds liquidity to the economy, and marginally benefits consumers. On the other side, it pressures capex spending, suggests weak global demand, and stresses indebted energy companies.

Our position has always been that global demand is perpetually under-stated, something that has played out time and time again over the last few years as so many erroneously try to treat it as a supply issue. The Wuhan virus can have at the most a highly transitory and barely noticeable impact on oil demand. And when demand is impacted, the most basic of economic laws says that supply gets inversely affected, creating the price equilibrium that is at the very essence of what we call “supply & demand.”

That $50-75 range for oil is where prices are low enough to not suggest creeping inflation and high enough to maintain profitability at the margin for producers. And it is that range we believe will be maintained.

Economic check-in

As of press time the January jobs data from the Bureau of Labor Statistics has not posted (though it has by the time you are reading this), but we did get the ADP measure of private payrolls this week. 291,000 jobs in January was an upside surprise, and if matched by the BLS number will serve as yet another incident of rolling averages in jobs data pointing to an extraordinary job market up and down all wage levels.

And then there was the manufacturing data which returned to positive territory in January. Now, what can we think of that got better in the last couple months versus the months prior that might explain this??? #tradewar #phaseone

So what would an economist want to fret about right now? The answer is the yield curve, which though “un-inverted” this week, continues to be too flat to reflect confidence in long-term economic growth.

Pros and Cons

The liquidity and loose credit environment bodes well for the economy and market. Employment and labor and consumer confidence are indisputably positive.

Capex, manufacturing, and business investment are negatives.

Inflation remains low and points lower when energy prices decline. Long-term growth is compressed by excessive deficits as we spend today what we would be investing tomorrow. There are good and bad components, but America remains the economic hot spot of the world.

Trade update like it’s 2019

After the phase one trade deal I am sure you are hoping that periodic trade war updates are left in last year, but actually this week provided a positive update when China announced they are cutting the tariffs on $75 billion of imports from the U.S. in half! This is in line with phase one deal implementation but represents a hugely positive (and timely) indication about where things stand in trade between the two countries.

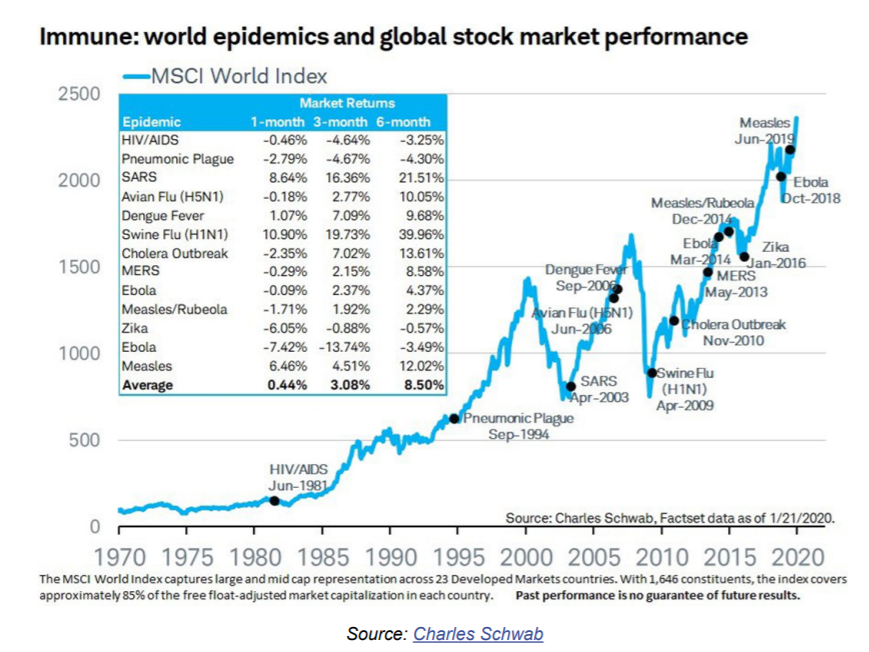

A trip down memory lane

Shocked that the market went up over a thousand points this week with a virus outbreak? Let history be your guide.

* Mauldin Economics, Charts that Matter, Jan. 29, 2020

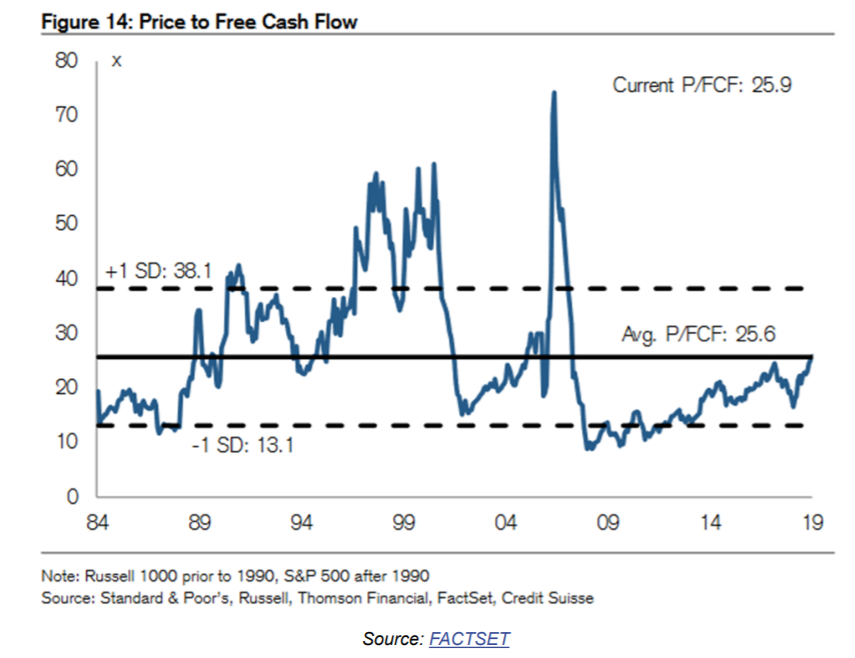

Valuation re-visited

We have heard ad nauseum about the market’s valuation from a P/E standpoint (price-to-earnings), and I have argued for some time that:

(a) The market taken as a whole index is fully valued or slightly over historical median value

(b) That provides no timing benefit at all as markets spend most of their time going above the median or below it – not at it

(c) Within the index, there are certain companies and sectors that account for all of the froth, and some companies and sectors that are at a discount to historical valuation

But I will now add another point: Price-to-earnings is not the only valuation metric out there. Indeed, taken by price-to-cash flow, the market is not over-valued even when taken as a whole.

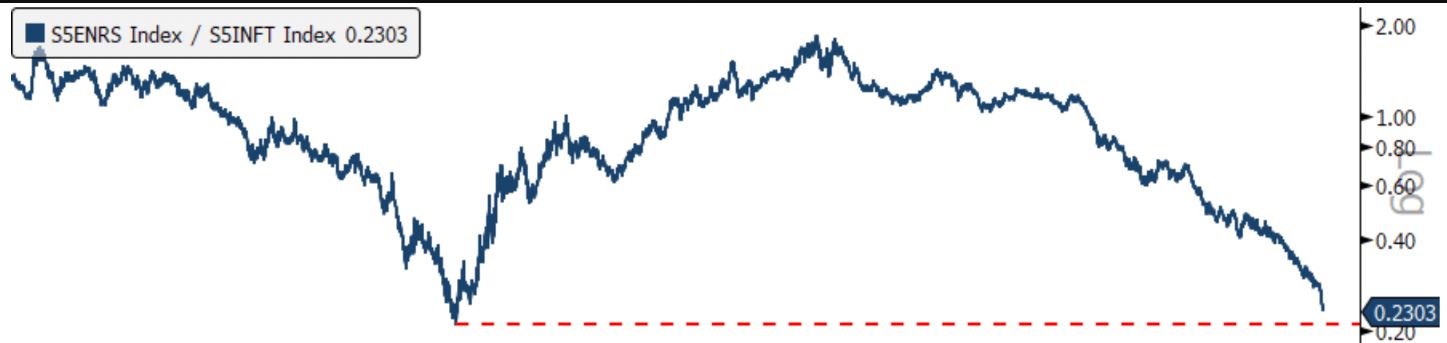

An early chart of the week

Before we get to the official chart of the week, this chart grabbed me and hit me in the face … This represents the ratio of the Energy Index divided by the Technology Index – and it looks like it is being set up for a simply massive mean reversion. One can believe what they want about reasoning, timing, and any other logistics. But this chart is a powerful dual expression of the value embedded in Energy and high cost of much in the Technology space.

* Baycrest Partners, Stranger Things, Feb. 5, 2020

The resilience of a good portfolio investor

Is there such thing as a resilient portfolio? It depends what one means by that. A portfolio can be built with the appropriate diversifiers, defense, and reducers of volatility that one needs to be comfortable – to be psychologically soothed in periods of up and down price movements. Portfolios can be built with more credit risk, or less credit risk. They can be built with more underlying fundamental strength in the companies owned (balance sheet, leverage ratios, etc.), and of course they can be built with less of that sort of thing. Certainly portfolios built around the eternal aspiration of a growing P/E ratio vs. an alignment with growing free cash flow and dividends have different levels of “resilience.”

But this is a worthless conversation apart from the concept of a resilient investor. A less defensive portfolio may hold up fine when held by a well-behaved investor. And even a more defensive portfolio (the kind we favor) is doomed when an investor forfeits rationality and discipline in favor of panic, behavioral mistakes, and emotional capitulation.

We view our mission on God’s green earth as guiding the resilience of our clients behavior, not merely their portfolios. To that end, we work.

Politics & Money: Beltway Bulls and Bears

- President Trump’s approval ratings reached the highest level of his Presidency this week. His betting odds for re-election reached their highest level to date. The Democratic Iowa caucus was fumbled and mumbled and jumbled so badly that no level of analysis could possibly do it justice. He was acquitted by the Senate in his impeachment trial. And he gave a State of the Union address to a captive TV audience. It was not a bad week for the President of the United States politically.

- Don’t look now, but Michael Bloomberg has now exceeded Joe Biden in the betting odds to win the Democratic primary. And at 20% odds (vs. Biden’s 16%), that represents a really interesting development (if Biden ends up out of the race before Super Tuesday – highly unlikely, but not impossible).

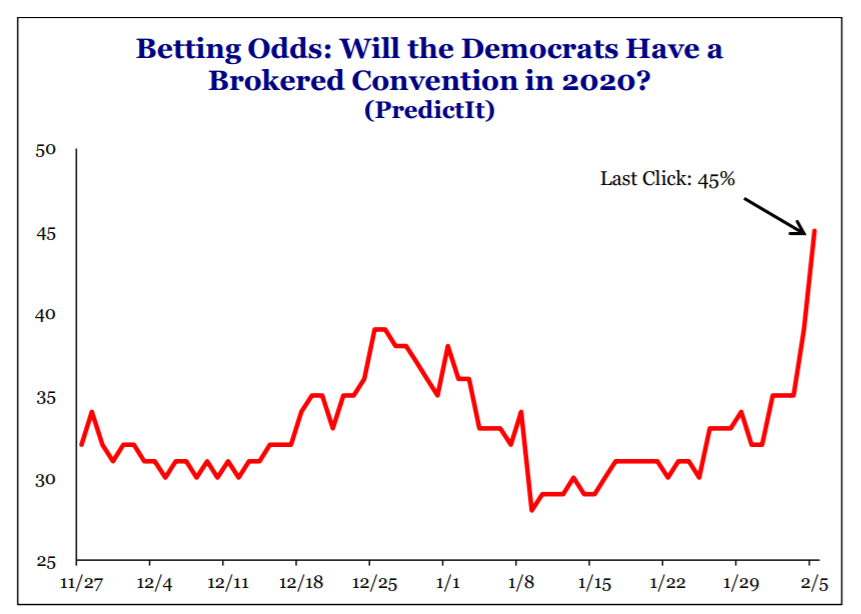

- And don’t look now, but the odds of a brokered Democratic convention are a stunning 45% …

* Strategas Research, Policy Outlook, Feb. 6, 2020, p. 6

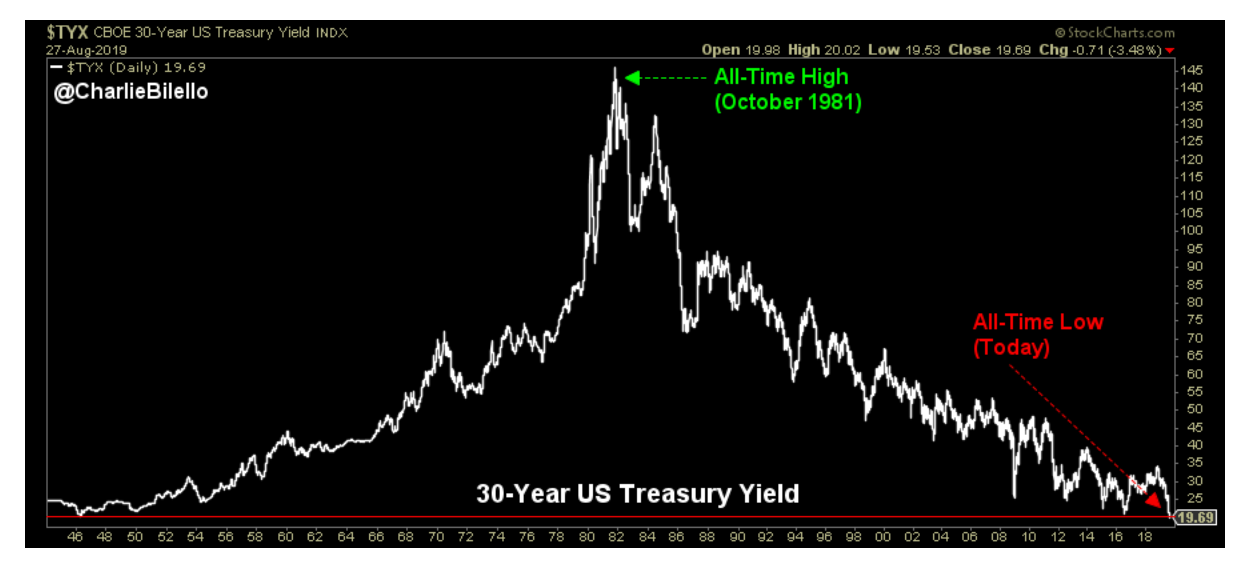

Chart of the Week

What does a bond bull market look like? Remember that bond prices go UP as bond yields go DOWN (and vice versa). Note the incredible inflationary pressures of the left side of this story, then disinflationary forces, and then deflationary forces, and how bond yields have responded. A stunning upside-down V in bond yields. And with it, the generational story of our capital markets.

* Compound Advisors, Charlie Bilello, Jan. 5, 2020

Quote of the Week

“It had long come to my attention that people of accomplishment rarely sat back and let things happen to them. They went out and happened to things.”

~ Leonardo da Vinci

* * *

I do want to welcome the newest members of The Bahnsen Group family, Steven Tresnan, Leigh Ferst, and Mina Widmer, all based in our newly expanded New York City office. Click the link to hear more, but we could not be more excited to be adding such a depth and breadth of talent to our advisory team and client experience platform.

This was (as of press time) the strongest week in the market in a long time. We shall see what next week holds. Might I remind you that a big week up makes no more difference to your long-term achievement of financial goals than a big week down does? Sustainable dividend growth … To that end we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet