Dear Valued Clients and Friends,

Greetings from beautiful Palm Beach, Florida, where by the time you get this, I will have left my fourth Floridian city in five days and returned to New York City. It has been a whirlwind of a week in markets, in the data, in the political scene, in the weather, and in Florida speaking. But this week, we took a whirlwind of questions and did a special “mailbag” Dividend Cafe. As always, the questions cover a lot of topics, and as always, the answers are meant to be succinct, direct, and clear. I love corresponding with your questions, and I hope the wide audience of Dividend Cafe finds these questions (and answers) useful.

This week, we cover some inflation/deflation vocabulary, even bringing back vital words like velocity and Japanification. We evaluate the way the BLS covers the hilarity of social media “influencers.” We look at what the Fed should be doing in the world they have created. And really, so much more!

Always feel free to reach out with questions of your own, and in the meantime, jump on into the Dividend Cafe.

|

Subscribe on |

Vocabulary Review

“You used the word ‘disinflation.’ Could you walk us through the difference between disinflation, stagflation, and Japanification? Or are these synonymous?”

~ Brendon

A fair question – let’s do a little recap here. “Disinflation” is a “decreasing rate of inflation.” It is not prices going negative (i.e. from 100 to 99), but rather if a price goes from 100 to 102, but then goes from 102 to 103, that is “disinflation” (the rate of price growth is declining).

That is not at all synonymous with “stagflation,” which is really the combination of high (above average) inflation with economic stagnation. So high unemployment and high inflation at the same time is “stagflation” – and really, the last time we saw that was in the 1970’s.

“Japanification” is a made-up term, one I have defined in quite a few Dividend Cafes, and it refers to the downward pressure on growth that happens in an economy when the fiscal and monetary medicine used to treat asset bubbles bursting loses its efficacy.

“Deflation” is a decline in the price level, where “disinflation” is a decline in the rate of growth of the price level.

Why should the Fed raise at all?

“There are obviously lots of market bets around the timing and the increments that the Fed will be lowering rates this year. But why should the Fed ease at all if none of the fundamental economic numbers change? GDP growth, employment, inflation, the banking industry and credit stress in general are fine. The Fed should not ease simply because of the passage of time and market expectations, in my opinion. Am I wrong?”

Chris T.

The issue here is separating what I believe the Fed ought to do (be a lender of last resort) from what their current mandate is (price stability + full employment). In their current paradigm, based on their aspiration to fulfill that dual mandate and use the “neutral rate” to set policy (by going above it to slow economic activity and below it to accelerate economic activity), I cannot find a justification for keeping the rate at 5.5%. The question is a really fair one – “if unemployment is staying below 4% and GDP growth is above 2.5%, and credit spreads are contained, why mess with the current rate?” And the answer is that there is absolutely no question that 5.5% is well above a “neutral rate” – that it has frozen homebuilding, frozen commercial projects, and taken out small corporate borrowers from bank lending. While the economy has not rolled over and employment is quite solid, the reason to reduce is that they would inevitably change that if they did not – particularly behind the “maturity wall” where so much corporate and real estate debt lies in terms of rate locks (i.e., the amount of debt resetting to higher rates in late 2024 and throughout 2025).

I do not believe in the permanent boom/bust cycle in which we find ourselves, but to stay at this rate assures a bust, which then assures a reversal gone-too-far the other way, rinse and repeat.

Capex is not all created equal?

“Is business investment growing as GDP has grown the last two quarters? I know you look at that more than consumer activity.”

~ Nick E.

One thing I will say about capital spending – it has increased, but almost entirely from the government side. Does that matter (if it is the government paying companies to do things versus companies paying companies to do things)? The answer is no, and yes. On one hand, there is no question that private companies can do productive things with money, even when it comes from the government. I have every reason to believe some of these things will marginally enhance productivity, even when funding comes from the government. But the other side of the coin is that it absolutely means a drag on future growth, as government debt spending today is less spending in the future. So, pulling forward future growth into today helps today but hurts tomorrow. It is really that simple.

And I should add, construction spending for manufacturing alone was $214 billion last year, up +61% from the year prior. Is that all government spending? No. Is a lot of it? I think so. Will it lead to more private sector activity after the construction is done? Well, that would certainly be the idea. I think it will boost productive business investment, but I think a lot of it will be wasted, too.

The Alternative(s) Criteria

“Could you explain a bit as to what alternatives you use and in what situations? I am just curious what drives the decisions about which types of alternatives get used for which clients in what situations.”

~ Jonathan S.

Much like our total asset allocation process, this really comes down to very specific client needs and situations. On a macro level of allocation across a client portfolio, the risk tolerance, the comfort with volatility, the liquidity needs (in terms of income and/or access to principal), the sophistication and comprehension level of the client (we call it the complexity tolerance), the tax circumstances, the timelines, etc. all play into how a portfolio is constructed within our “Magnify” silos we use to run our firm’s portfolio management. But this question is specifically within the silo of “Alternatives” and how those decisions are made client by client.

Much of it depends on what we are seeking to diversify. If a client has ample equity exposure in public markets and needed all of that risk bucket for their income needs, etc., we may not be using private equity or equity arbitrage in the alternative bucket but might be looking at global macro or real estate or private credit. If the client is intensely income-focused, the alternatives would almost certainly be biased toward those with a coupon (private credit, direct lending, real estate, structured credit, etc.). If there is a high tolerance for complexity then drawdown/call structure private equity makes sense, but if a monthly mark and instant deployment is desired a different form of private equity is used (this has been a recent priority). What is already owned by a client, what is advantageous in the marketplace, where deal flow lies, and the total investor objectives all drive the decisions.

In addition to highly tailored selection by our advisors and investment committee on a client-by-client basis, we take extreme pride in the curation of what we are selecting from – that is, the due diligence that goes into the menu we use for such alternative investing.

Oil in Water

“Did President Biden make some quiet, behind-the-scenes change in energy policy that nobody noticed? The U.S. was producing 11% of the world’s oil when President Trump took office, it went to 15.5% when he left office, and is 16% now. I am surprised no one is talking about this.”

~ J.D.

On one hand, there are political optics that keep President Biden from bragging about production being higher than many may let on (it is not a highlight to many in his base), but on the other hand, it also is not quite the production victory the headline data may indicate. The Strategic Petroleum Reserve saw 350 million barrels withdrawn in 2022, with barely any replenished in 2023. And more importantly, the gross production is still not clearing the market, projects for future production growth have not been approved, new pipelines for transport have not been built, and drilling on federal lands is way down (a Presidential administration has little or nothing to do with what gets drilled on already dug private lands). Our key Permian producers drive present-tense production levels; public policy has a lot to do with projects needed for the future.

V is for Velocity

“What is velocity with respect to money flow?”

~ Wayne E.

Velocity is the number of times a dollar in circulation turns over – so if person A spends money with person B, and that person spends the same dollar with person C, etc., you see a measurable velocity. When a person in the chain of money changing hands stops spending it, it represents a lower velocity. Across the economy, it is measured as V=PQ/M, which is to say – Velocity equals Nominal GDP divided by Money Supply (more specifically, in the algebra, the price level X transactions divided by money supply).

If you want to take out some of the fancy terminology and concepts, it is money turning over in the economy, and it is highly, highly correlated with loan demand.

Twin Towers

“I greatly appreciate your writings on Japanification and the U.S. trajectory towards something that might resemble it. Do you believe that because Japan does not have a negative net international investment position nor an externally financed bond market (twin debt towers) their situation is different from ours?”

~ Carl F.

I do not believe for a minute that foreign capital to fund U.S. deficits versus Japan’s self-funding changes the thesis of Japanification. What those who bring this point up always seem to miss is that it is the result of Japanification, not a factor prohibiting it. Japan finances its own bond market because they have to. The U.S. version of Japanification is, thus far, significantly more moderate (as I have repeatedly pointed out) and is evidenced in the BofJ owning 50% of Japan’s bond market and our central bank owning well less than 20%. So there are certainly differences on the margin, but not at all in the structural points – that excessive use of fiscal and monetary tools to treat slow economic growth creates slower economic growth, still.

MLP, LNG, and TBD

“Given your belief in the strength of MLPs, how will the new ban on LNG exports by the Biden administration impact the performance and profits of these MLPs? In your view, is the ban just an election year move or will it lead to something more permanent?”

~ Sehat N.

I believe we will end up exporting more LNG regardless of who wins the Presidency because the environmental, economic, and geopolitical circumstances all call for it. Some will be more excited about this or more public, but all will see the need and mandate over time. Export LNG only impacts very few MLP’s, but this current ban helps those who already have export LNG terminals online (most businesses love the government sidelining their competitors for them).

Steve Martin said it best (few will get this reference but I’ll take guesses)

“How does the reporting on labor participation handle all the social media ‘creators’? Are they just in the self-employed category? With so many people missing from the workforce and so many of the younger generation interested in this “career”, I wonder if there might be a correlation there. Seems doubtful that there is a relatively significant number of these people actually making a living, but I wonder if there might be a significant number who consider themselves ’employed’ while the BLS considers them unemployed and not looking for a job.”

~ Greg E.

The BLS does, indeed, capture “self-employed” people. If this was being missed, by the way, it would mean the unemployment rate is actually lower than publicized, not higher. But the BLS has long had survey methodology for those who are self-employed, regardless of their take-home income.

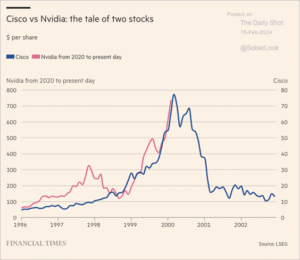

Chart of the Week

It is always a compliment to see charts and concepts I created months ago end up in the pages of the Financial Times, even without attribution.

Source: Financial Times – The Daily Shot – February 15, 2024

Source: Financial Times – The Daily Shot – February 15, 2024

Quote of the Week

“In politics, good gets better and bad gets worse.”

~ Haley Barbour

* * *

I hope everyone has a wonderful weekend. Markets are closed Monday for President’s Day, but a long-form special DC Today will be awaiting you all Tuesday. If the question most on your mind was not addressed today, send us what is in your mind, and we’ll get you into the mailbag! And beyond that, thank you for this run through the Dividend Cafe.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet