Dear Valued Clients and Friends,

The month of April came to an end this week. It feels weird to say it was the best month for stocks since January of 1987, even though it was. When stocks suffer the kind of rapid and violent moves down that they suffered from late February throughout March, the math of the first phase of recovery sounds better than it feels. But that’s not to say that April markets didn’t feel good to investors, too. There is actually a lot to learn from the April market action, and I think this week’s Dividend Cafe is a great place to do it.

I learned a lot in the month of April as well, and I want to share it with you today. I am either excited to tell you or sorry to tell you that this week’s Dividend Cafe is the longest one I have ever written, but also the most important one I have ever written. The length of it is just simply because of the sheer ambition of all I am trying to cover this week. There are some investment opportunities that have been created out of these last two months that warrant the attention I have given them this week. But there also are lessons learned and principles reinforced that I am excited to share.

For readers of the Daily COVID and Markets missive, please note that this Dividend Cafe commentary will serve that purpose today to avoid redundancy. COVID and Markets every day but Friday; Dividend Cafe every Friday as longer weekly commentary …

I do hope you will buckle up and jump on into the Dividend Cafe.

Resolving my inner conflict and where you fit in

I would like to explain a little something before we dive into this week’s Dividend Cafe that I have struggled with as long as I have been writing weekly market commentary. In the simplest of summaries, I do not think the commentaries provide actionable information for my clients (or non-client readers). Put differently, they are not written to provoke an action, and frankly, the better conclusion from Dividend Cafe may be one of inaction (assuming one is already invested within the principles we hold dear).

But that is not the same thing as saying that Dividend Cafe is not important. It is just that I believe its importance is different than many understand it to be. I believe from the bottom of my heart that investor behavior drives the lion’s share of investor results. I have believed this from very early in my career, and then every year of my career has been one reinforcement of this principle after another. I believe most financial objectives are met by the simple facilitation of compounding capital (accumulation phase), and then the simple process of dependable withdrawals (spending phase). I am sure I could think of exceptions, but what has created financial failure time and time again has been behavioral interventions in either phase – interventions that can best be described as “big mistakes.”

Every single advisor at The Bahnsen Group works diligently to help our clients avoid those mistakes. They take on different shapes and sizes, but usually amount to some manifestation of a panic-mistake or a euphoria-mistake. Fear or greed. One or the other. Always. And so it always will be.

I believe we will have a vaccine to COVID-19 – perhaps sooner than many believe. But I do not believe we will have a vaccine to the parts of human nature that plague financial goal achievement. I believe the human condition is ontological, and if you would like I will start writing more about philosophy (my first love, thank you, dad). In the meantime, let me just say that I take it as a solemn duty to protect my clients (and to a much, much lesser degree, the non-client readers of Dividend Cafe) from the realities of human nature. Greed and fear give way to euphoria and panic, and out of euphoria and panic, time-tested financial plans get ripped up. Excessive leverage gets taken. Mistakes get made that leave people devastated. So yes, to that end, we work. We can’t have it.

And this gets back to the inner conflict I began writing about a few paragraphs ago. I want my clients to understand what the Fed is doing. I really want my clients to better understand economic theory (speaking of which, there is some real theoretical love in this week’s Dividend Cafe if you make it that far). I believe in heavy communication around what we are doing with client portfolios. I believe in being a reliable source of information, perspective, and unabashed conviction. I cannot stand the gutless and thoughtless drivel that passes as investment commentary these days. We do view thought leadership as part of our value proposition. Particularly in times of distress, we want to foster more confidence, more faith, more trust, more understanding, more wisdom in our clients – and we want to do that in our relationship with you, but also in the perspectives we share through our various content properties.

So what is the problem, exactly? I do not believe there is any harm in clients learning more about structured credit (you’re about to), multiple expansion, inflation, midstream energy, or any of the topics we are about to tackle. What keeps me up at night is fear that I would ever communicate accidentally that some magic information, secret sauce, or key application of data could ever in a million years transcend the need to behave well as an investor – to avoid the big financial mistakes.

If you read Dividend Cafe and market commentaries like it throughout the COVID economic distress, you will likely come out of it a more informed investor. But if you don’t read it all, and just simply avoid financial mistakes throughout and wake up a few months after it is done, you will be just fine. The purpose of this content is to facilitate the right behavior, and never the wrong behavior. I am ever mindful of the need to manage that, and I thank you for hearing me out on this.

Now let’s get to it.

In all thy getting, get this (TINA, meet Fed) …

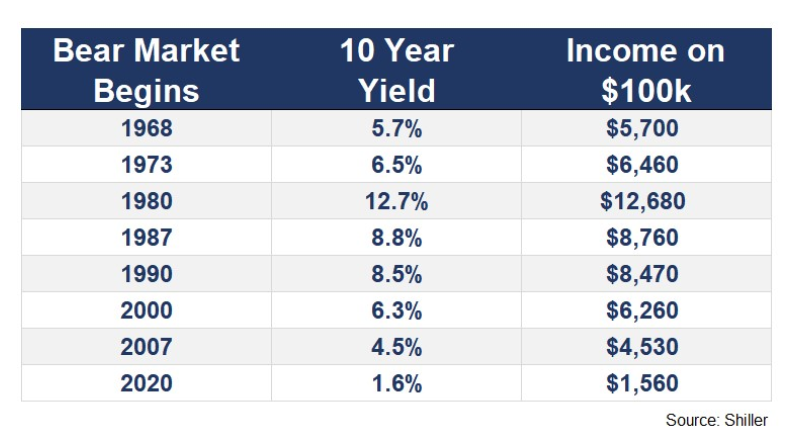

I can think of no simpler and more useful explanation behind investor relative confidence in U.S. stocks than the lack of alternatives stripped away by the low-interest rate environment. Past periods of market volatility always offered some positive return in Treasury Bonds, money markets, CD’s, etc. Even my chart below shows a 10-year bond yield of 1.6% at the beginning of 2020, when in fact it is 0.6% now. “There is no alternative” remains a compelling factor in the direction of investor flows now, and I reckon, well into the future.

What is this “discounting mechanism” you speak of?

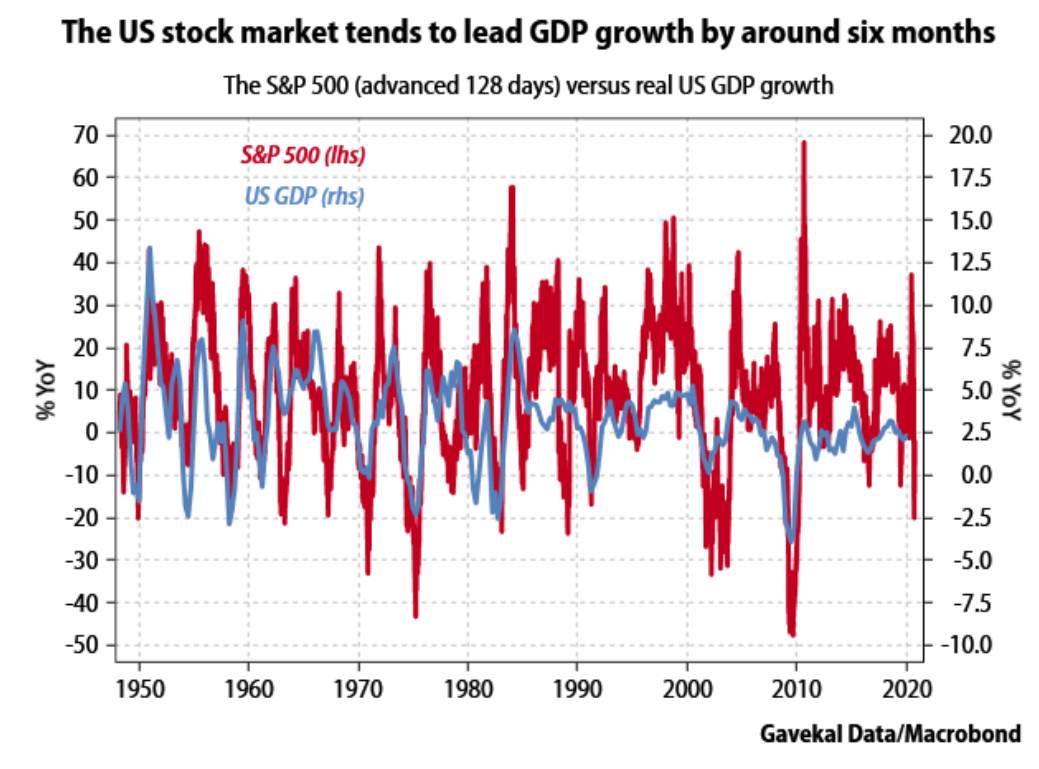

I am as serious as can be that I do not know what the stock market will do in the next few weeks and the next few months, but I am even more serious that (a) The economy being really bad, and (b) Stocks not shrinking much from where they are, would not be abnormal, but rather very normal. If the economic contraction all market actors know is coming proves to be much longer-lasting than some fear, or even deeper than some fear, than of course the “discounting” the market has done or is doing may prove inadequate. But it is the norm for markets to lead GDP growth by 2-3 quarters, and this is a reality that goes back decades!

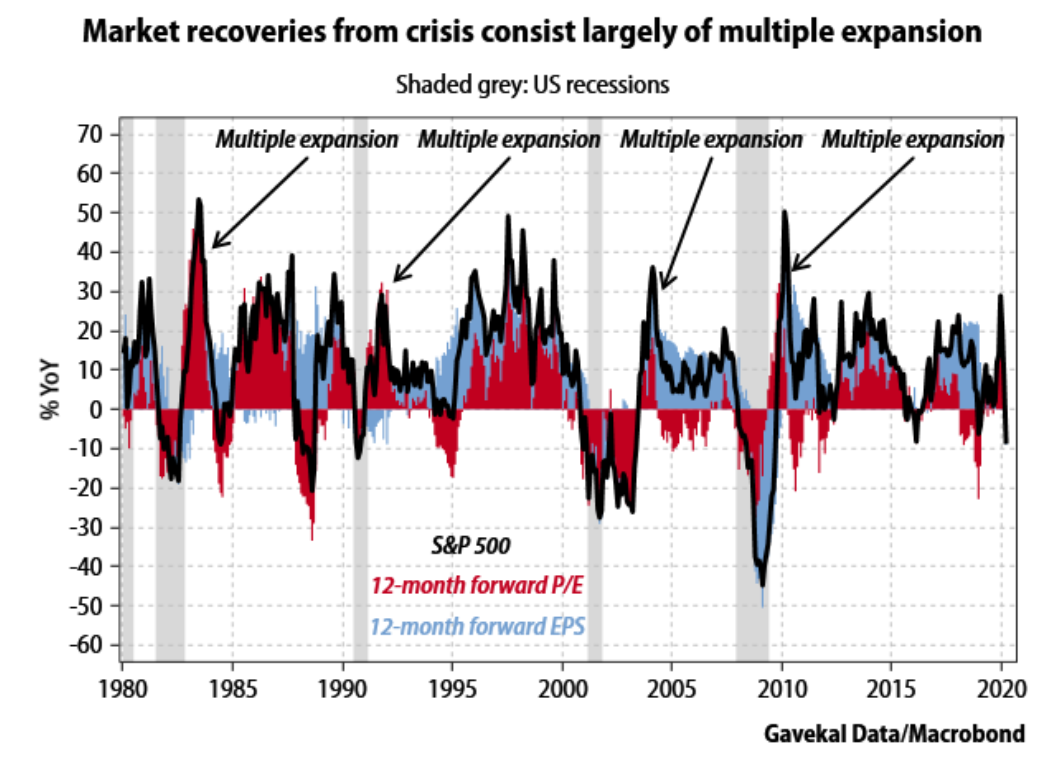

A quite substantial multiple expansion could very well offset what we know will be substantial earnings contraction. And this would not be hoping for some irregular miracle – it would indeed be the historical norm. The argument is that Fed policy has set the table for substantial valuation premiums. Sentiment may very well go a different direction, but I am not at all convinced that one can know where earnings will be in early 2021, or what multiple will be deemed appropriate when all monetary accommodation is factored in.

I am only convinced that that will be the market’s focus in the months ahead, not the daily headlines (which will, no doubt, be awful).

The State of the Health Pandemic

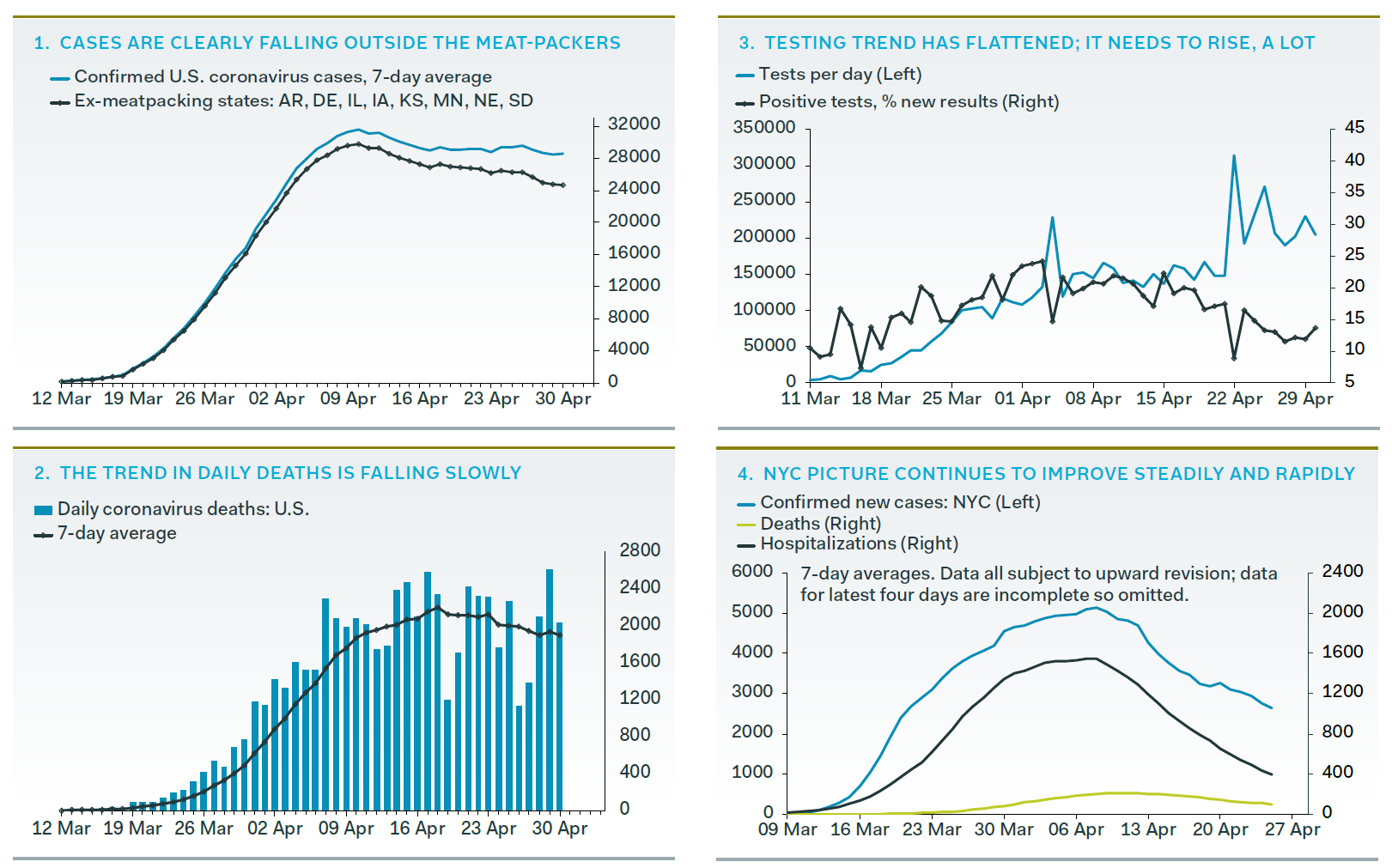

My daily COVID and Markets missive attempts to break out the daily update in case growth, testing, the shape of the curve, and other medically-relevant facts around the state of COVID-19 (globally, but particularly here in American society). I have been encouraged by those that have felt I am being too optimistic in my presentation of data, because, well, if all I am doing is presenting data (from a multitude of highly respected government and academic resources), and the interpretation is that I am “being optimistic,” that must mean the data is pretty good. But here is where things seem to stand from an objective point of view here in the states:

(1) Case growth is falling, and the % of case growth seems likely to continue falling.

(2) The trend of deaths is falling, but the fact that thousands of mortalities where COVID symptoms existed (without a COVID positive test) has kept it from falling further

(3) American daily testing has picked way up recently and with it a decline in the ratio of positive tests! This is truly good news. However, a daily test average of 300,000+ tests would go a long way towards instilling public confidence and demonstrating lower and lower positivity of the virus.

(4) There is no bigger explanation of reduction of left tail market risk than the fact that the “hell is coming” predictions of an American medical system overwhelmed by hospitalizations and equipment utilizations have now subsided. In New York City, where 30% of American cases and 36% of mortalities have occurred, the hospitalizations are down over 75% from their peak.

(5) There is obviously tremendous controversy around what level of relief is appropriate in what geographical areas from the most draconian of limits to American life and the American economy. I have my opinions and you likely have yours. And some Governors are handling it differently than other Governors, and some local variation in approach is logical and appropriate. I will not use Dividend Cafe to share my views of what ought to be here, but rather to share how markets and the economy are responding and will respond to what is. The employment data gets better when the economy re-opens. It stays bad while the economy is shut. I don’t know how I can say anything less controversial than that.

* Pantheon Macroeconomics, May 1, 2020

A Structured Credit Extravaganza

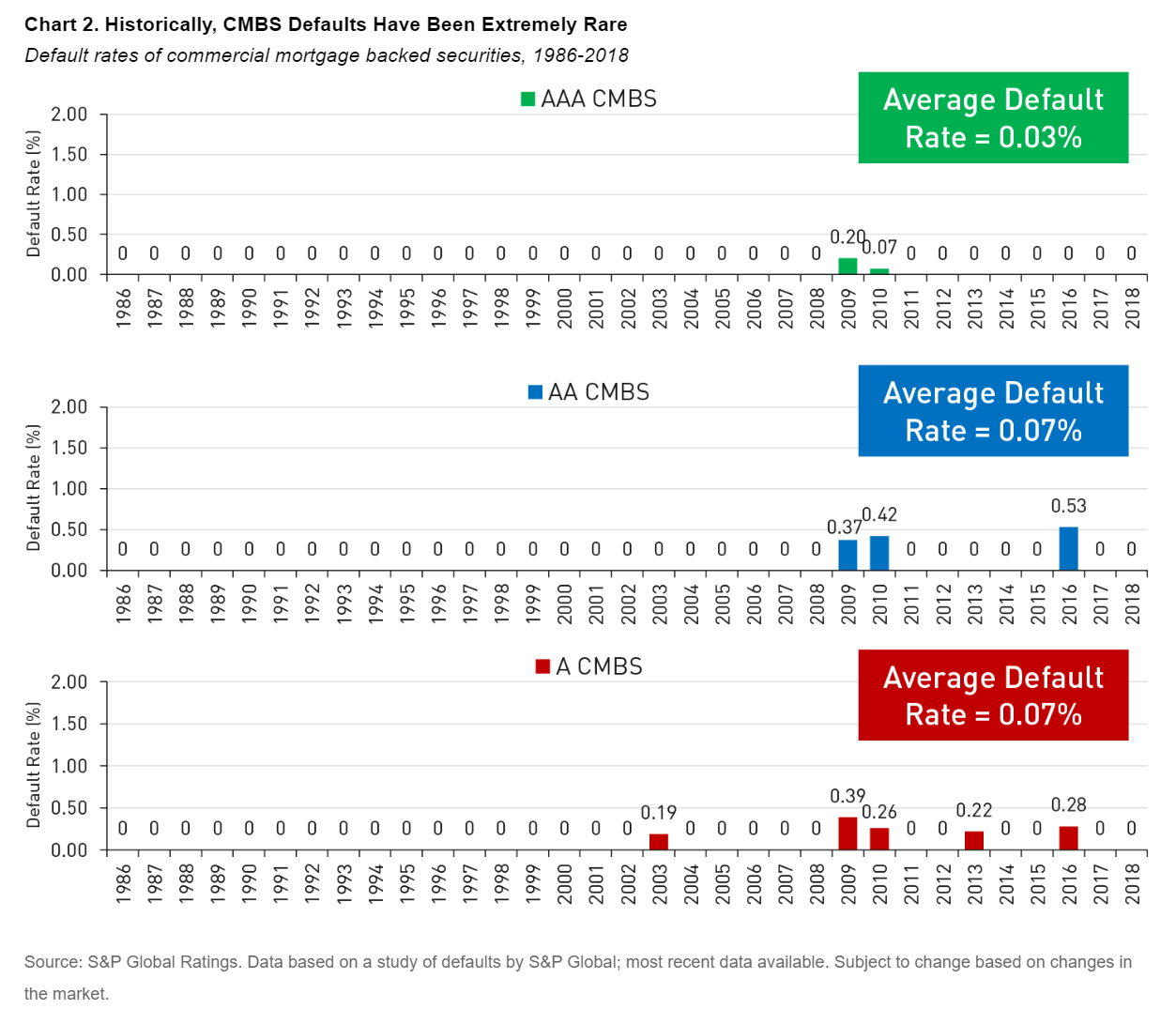

When we speak to dislocations and opportunities within commercial mortgage-backed securities (CMBS), it is not our view that all is rosy in the commercial real estate (CRE) world. Quite the contrary! Rather, it is our view that, despite the genuine challenges in CRE, the senior tranches of CMBS are largely insulated from those challenges in the final hour, and offer opportunity right now as the entry-level prices reflect the sector-wide challenges but not the specific nature of these securities. Not only are defaults extremely rare in senior tranches of CMBS, but the underwriting that has gone into these post-financial crisis is categorically different than pre-crisis underwriting (for the better). The “waterfall” structure provides credit enhancements at the more senior levels that are largely being ignored in the market right now due to overall uncertainty. In that space, we believe there is great dislocation.

Spreads have widened across the CMBS universe, both because of liquidity challenges and a difficult macroeconomic environment. What is interesting is that even in the more dire of forecasts for potential CRE delinquencies, forecasts we are skeptical of but at least open to, the senior CMBS paper continues to perform. When one plays it all the way through, and assumes (without much warrant) that delinquencies exceed negative expectations, and that those delinquencies go to default, and that those defaults are not cured, even all the way to the liquidation phase, losses have to exceed 60% in most cases for senior bondholders to be made whole (because of the waterfall of seniority embedded in the credit structure).

CMBS paper (even non-agency, and even sub-AAA), is largely not trading where it is because of presumed impairment that would affect the liquidation value. It is trading where it is because of a market dislocation, one that may last much longer for all we know at this time.

The closely-related sister asset-class to CMBS is Asset-Backed Securities (ABS), whose 0% default history we highlighted last week (securitized loans representing pools of auto loans, credit card loans, and student loans). The argument for this asset class cannot be that everyone will make their auto payment and credit card payment in the midst of COVID distress because they will not. The argument, again, comes down to the structure itself. The level of default rates necessary to impair holders of ABS for AAA prime auto loans is many multiples of anything we have ever seen before, including in the financial crisis.

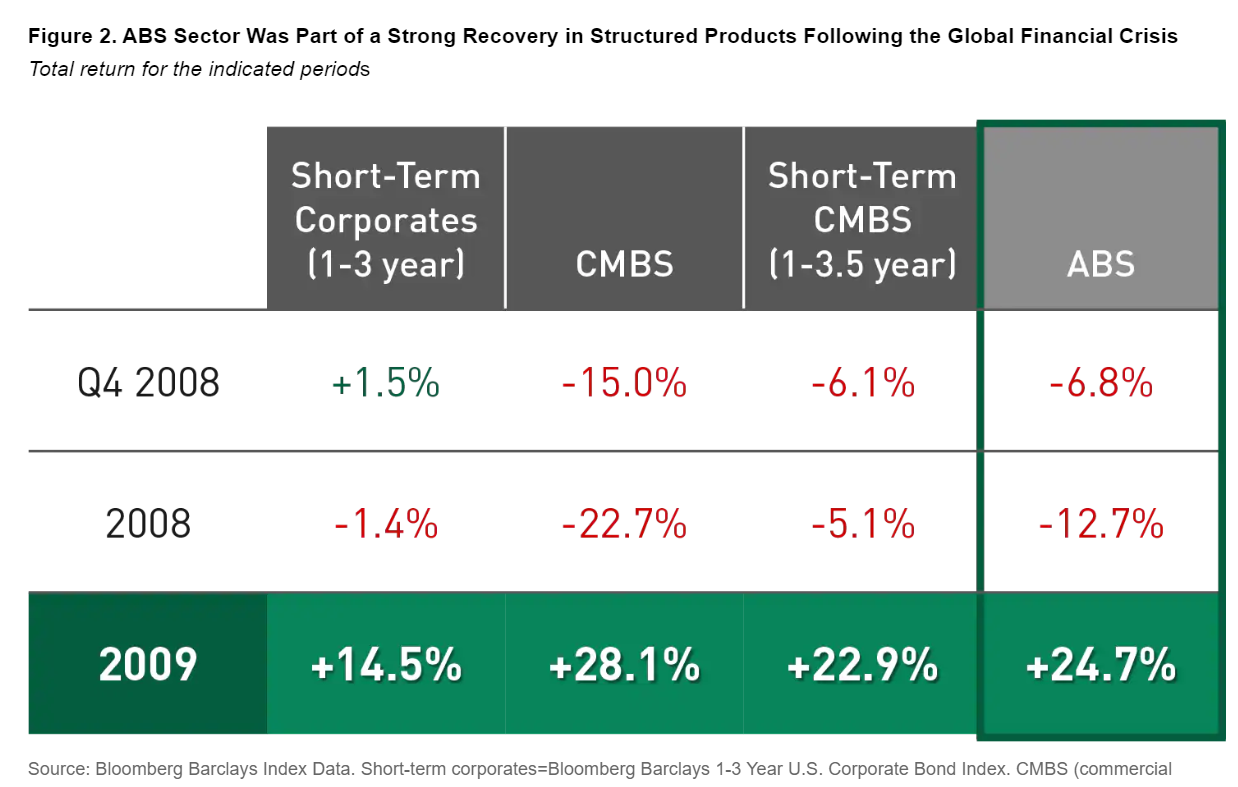

The strong distress in the CMBS and ABS space in 2008 led to significant returns in 2009. Don’t misunderstand: much is different right now. The Fed’s TALF 1.0 program in March 2009 was a shock; the TALF 2.0 has already been announced; and an aggressive Fed response is already assumed to some degree this time, versus the uncertainty of Fed intentions in 2009. But from illiquidity to dislocations to general uncertainties, these asset classes still reflect a period of opportunity, and the discomfort around such is more of an argument for it than against it.

And one more Structured Credit comment because you are begging for more

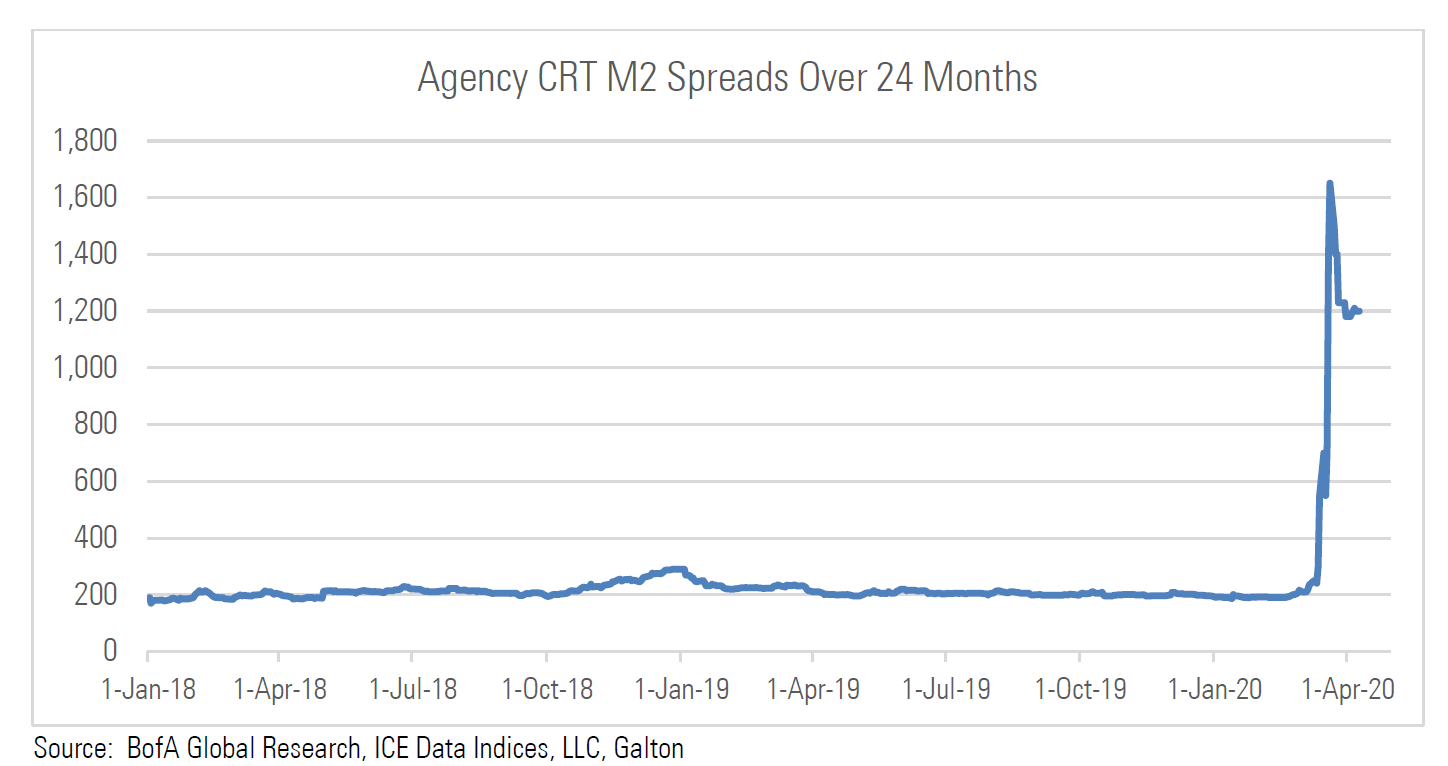

The non-agency Residential Mortgage Backed space (RMBS) is another component of structured credit we believe offers both risk and opportunity. The agency RMBS space itself – Fannie and Freddie mortgage pools – don’t offer the opportunity because they don’t offer the risk. The Fed is buying hundreds of billions of dollars of residential “agency” mortgage securities, and spreads are very tight and those assets quite well bid. However, there is a sub-category called “Credit Risk Transfers” (CRT) where Fannie and Freddie were absolved of full principal guarantee on these loans, but these were agency loans moved to private markets. They were underwritten using conforming standards, but Fannie/Freddie simply decreased the exposures for the taxpayers by transferring to private actors over time. The Loan-to-Values are generally over 60% (for those under 60%, Fannie/Freddie kept the risk), but still well within conforming underwriting standards. The explosion in spreads in this area of mortgage credits was simply surreal. And even with modest tightening since, the space remains extremely wide over its historical average, and any other bond barometer. Even adjusted for losses, there seems to be wide dislocation and opportunity here.

And finally, the largest marketplace of them all – Leveraged Loans

The banks in our country have lent a lot of money to various businesses over the last ten years. And I am referring to senior debt, at the very top of a company’s capital structure. We are talking about roughly $1.2 trillion in extended securitized loans, about double the size of the marketplace during the financial crisis. $600 billion of these loans have been sold to what we call the CLO marketplace (collateralized loan obligations) – baskets of these bank loans packed into a single security. And just as the Residential Mortgage Backed Securities offer different levels of risk and reward, there are different “tranches” of risk and payout for CLO’s as well.

The lowest tier of some of these securitized loan securities are trading down 40% since COVID, as some lower-rated companies in the lower security positions of the structure present uncertainty and risk. The highest-rated securities have not traded down much since recovery from March silliness (2-3% off highs), as the AAA and AA space simply don’t have defaults or downgrades (very often, if ever).

This is the easiest thing to explain in the world – the seniority of the AAA and AA CLO space offers less reward, and really a very low-risk profile (and recoveries, if there were to be defaults, would be quite high given seniority). The lower ratings have more risk, but more opportunity given their dislocations and wide spreads right now. How would we at The Bahnsen Group adjudicate where there is better opportunity in the lower tranches of the CLO space? We wouldn’t. It will entirely come down to credit fundamentals, economic recovery, and underwriting – and we will be relying on deep-dive manager skill to vet and select the risk/reward trade-offs in the space.

Midstream Energy – The Best of Times, the Worst of Times

April ended up being the best month for MLP’s and pipeline stock performance in history. Four straight weeks of +7.5% gains were met with a +5.8% gain this week (through Thursday’s close), and the result is a +nearly 50% price move off of the March lows. Now, this can be deceiving considering the peak-to-trough drop was so severe, but the numbers are what they are.

Some analysts have contended that Bakken activity and refined product volumes have been worse than even anticipated, but that seems to be a very idiosyncratic story that is relevant company by company. At the end of the day, even if it ends up leaving us with an opportunity cost, the decision to be laser-focused on relative strength (liquidity, balance sheets, counter-party strength, etc.) was one of the more significant decisions we made in the last six weeks. Distribution cuts continue from the weaker players, and distribution maintenance (or even modest growth) has been the lay of the land from those with more fundamentally reliable distribution coverage.

As earnings go, so goes the stock market … eventually

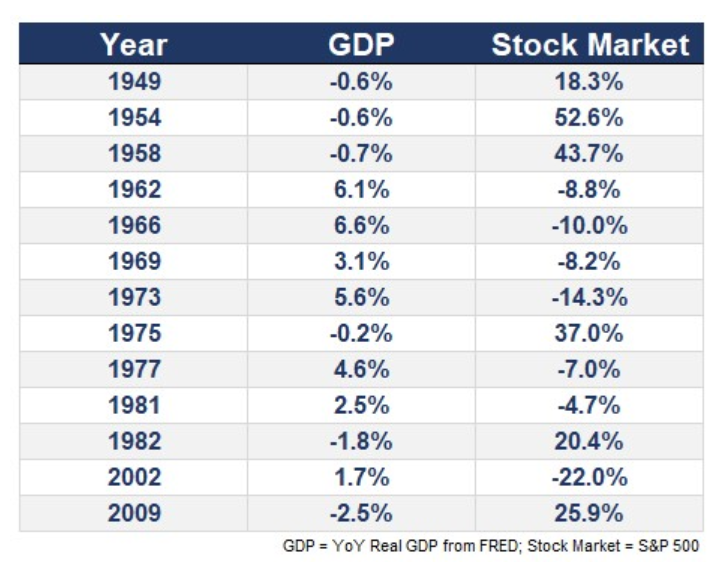

Earnings in 2020 are not going to be higher than they were in 2019, obviously. And the stock market seems highly likely to end 2020 lower than 2019 ended as well. But the market is not pricing in last quarter’s earnings, and generally not even the next quarter’s earnings, as much as it is two or three or four quarters out. This is not a short-term forecast or a present-tense rationalization for market behavior in the midst of economic distress … It is a historical fact. The S&P 500 has seen negative earnings 30 times over the last 90 years, and yet 77% of the time the market was up in those years of negative earnings growth. And what about the state of the economy vs. the stock market? It stands to reason that many times GDP growth is positive as the market is negative (as the market looks forward to bad economic data), and yet many other times the market is positive as GDP is negative (as GDP measures backward-looking bad economic data).

* A Wealth of Common Sense, Ben Carlson, April 25, 2020

I share this not to formulate a market call, but to discourage the efforts to even try. A market call based on present or backward earnings growth and present or backward GDP growth is futile historically, if not downright counter-intuitive. And formulating a future call on either earnings or GDP growth right now is arrogant and impossible.

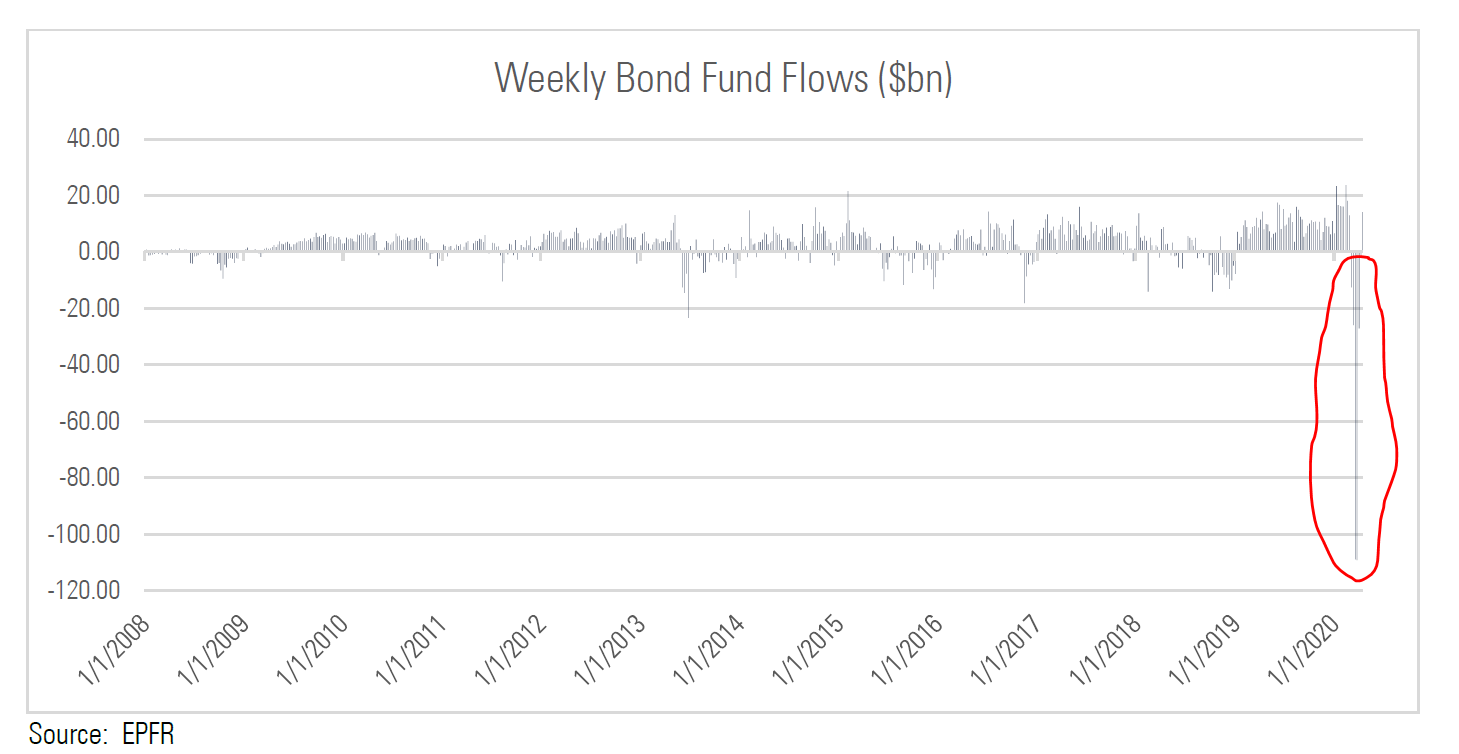

Forced selling for me and for thee

The hundreds of billions of dollars I have highlighted in past weeks that decimated equity markets in March from the likes of risk parity funds and quant strategies were in no way constricted to the equity markets. The violence of the need for forced sellers to raise cash is clearly evident in bond funds, as well, and this chart clearly highlights the magnitude of the dislocations in municipals, corporates, and certainly structured credit.

Monetary economics for those who want it (which is all of you!)

There are several things the Fed can do – and do with force – in the economy. They can dramatically impact the monetary base, and they can alter the reserves banks have on hand from which they conduct their business. They can even try to poke the bear a bit, incenting banks to put those reserves to work by favorably altering reserve requirements or the interest paid or charged on excess reserves. But there are two things no central bank can really control – the velocity of money in the economy (i.e. banks taking their reserves, and lending it out for a profit to someone who plans to use the proceeds to generate a profit on something); and the multiplier (the rate of productivity on the monetary base they generate). Don’t get me wrong – the control of the monetary base is a powerful weapon, but it does not supersede the power of lenders and borrowers choosing to do business with one another.

What has dumbfounded the inflationistas forever (those perpetually calling for inflation in every time, at every step) is that bank reserves do not increase the money supply. All of the bond-buying in the world from the Fed cannot make a lender and borrower transact – only the pursuit of profit can. Now, greater access to a greater monetary base can’t hurt, but it can’t create velocity / demand / opportunity / productivity ex-nihilo. I wish I could wave a wand and have this basic reality understood by all financial actors. Fed purchases of bonds and efforts to grow the monetary base can bid up the valuation of incumbent assets in the economy, but it cannot stimulate opportunities for new goods and services.

If one is looking for a measurement of velocity of money – more financial activity in pursuit of more productive endeavors – it would be in evaluating the productivity of debt. The more unproductive debt (i.e. government spending) the less velocity you will see and can expect. Productive debt can drive velocity. So I can say both of these things with extraordinary confidence in the present COVID environment: (1) The Fed’s aggressive monetary actions are effective for financial stabilization, and (2) The Fed’s aggressive monetary actions are not sufficient for driving future economic growth.

In fact, I am convinced, they hurt long-term economic growth by building up non-productive debt in the economy (the governmental kind). This is not to say it is the Fed’s fault – a government not spending trillions of dollars more than it generates in revenue would not need a central bank to buy trillions of dollars of its bonds.

But I am only calling balls and strikes here. We are facing extraordinary times as a country, and I want to analyze it accurately. The actions of the Fed thus far are not inflationary, not in their present forms. They cannot force a velocity of money, even if they wish they could. And furthermore, they are not a panacea … While stabilization is a good thing, the Fed cannot create productive economic activity.

Deflating the Inflation Fear (or Hope)

The idea that the Fed’s present monetary schemes amount to hyper-inflationary debt-monetization is fallacious, as demonstrated above. That is not to say they are benign (also as demonstrated above). Hiding the shenanigans of our country’s fiscal policy (large and growing budget deficits) on the central bank’s balance sheet is not the same as the Fed monetizing the debt (yet), but that does not mean it is a good thing. It just means it isn’t an inflationary thing, because output is still so far beneath economic potential. The irony is that the harder they try, the less effective it is (diminishing return realities), and the less inflationary the risk becomes.

What the bears are betting against

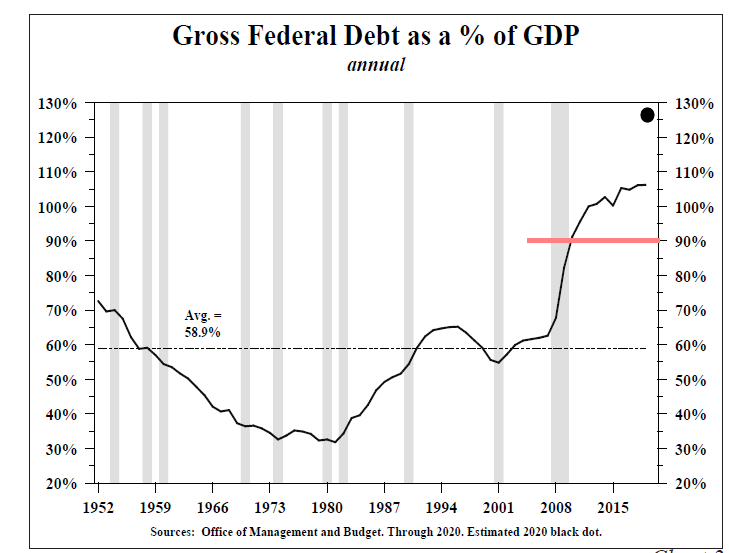

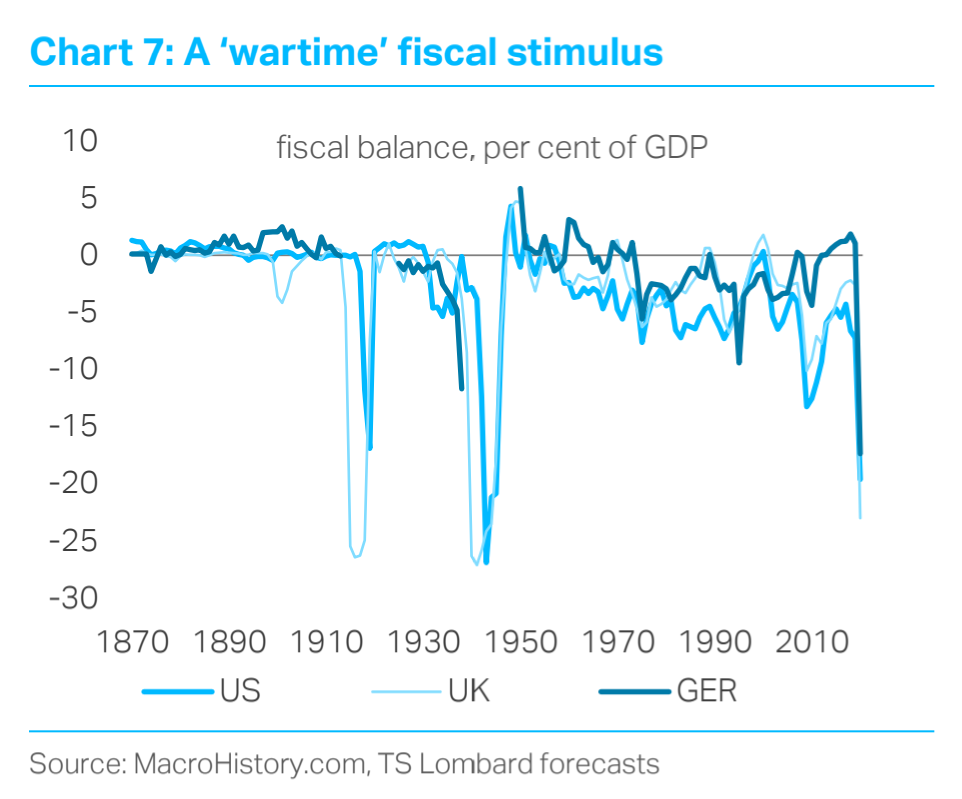

I do not claim the fiscal stimulus is going to work. And I am rather adamant that there are parts of the fiscal stimulus I very much believe were misguided. But regardless of the political, economic, and personal opinions one may have for and against some or all of the fiscal interventions to counteract the negative effects of the COVID crisis, it is imperative that we at least take serious the size and magnitude of what is being done (again, fiscal only – not even including Fed/monetary efforts). This percentage of GDP being addressed through fiscal channels only has two precedents in the last 100+ years – and both were literal world wars.

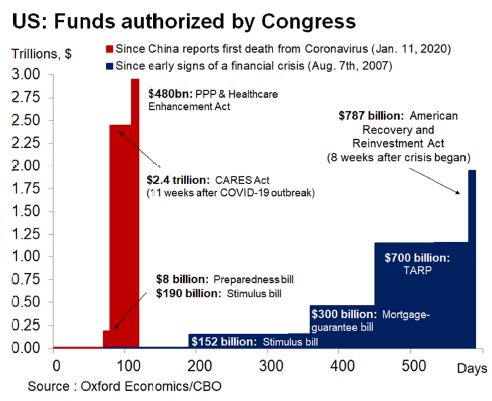

And I would add … the above chart demonstrates the magnitude of this present fiscal intervention. But note here the speed with which this stimulus has been passed and been circulated (vs. past fiscal stimuli).

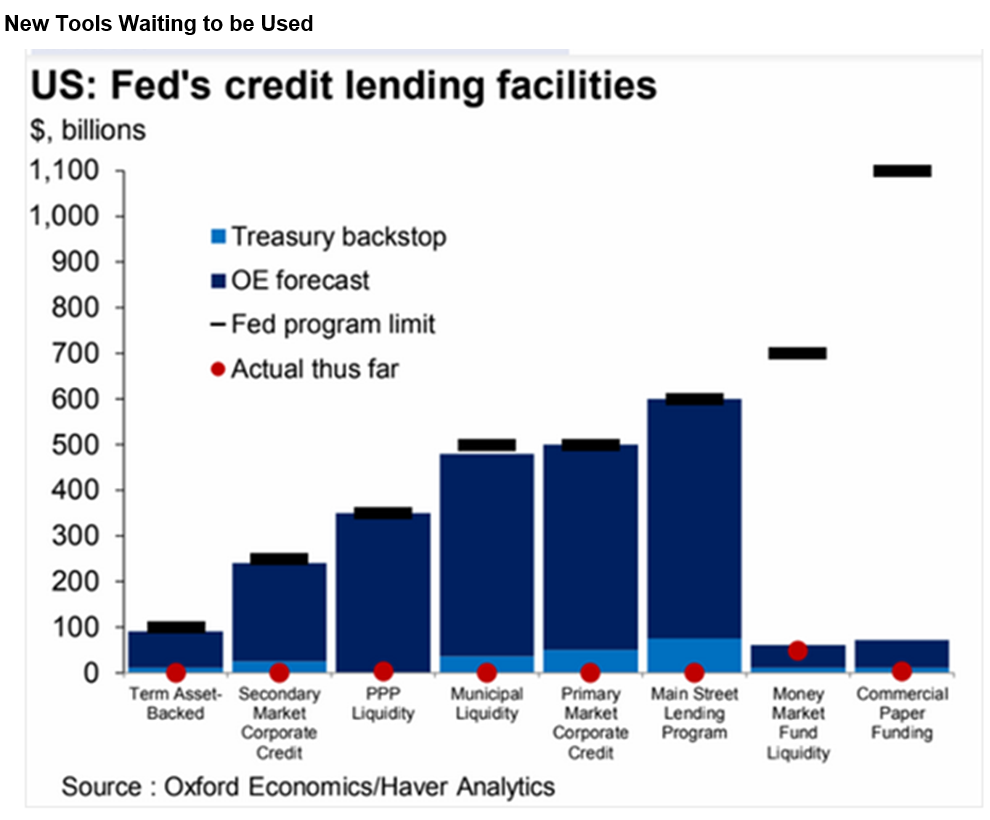

What the Fed did do this week

They basically reinforced their commitment to bond-buying (QE) and zero interest rates (ZIRP) as long as is necessary. It is really important to note how much they are setting up to do, but have not yet done.

I am not prepared to unpack this all right now, so look for more on this in the next missive from COVID and Markets, but there was a significant opportunity for the oil and gas industry packed into the Main Street Lending Facility changes this week.

Quick thought on munis

There was some not totally unreasonable speculation that it was Sen. McConnell’s comments about troubled states pursuing bankruptcy if they needed to that caused muni yields to rise this week. The fact of the matter is that flows into the muni space have slowed substantially even as new issue supply is picking up. Combine that with the clear facts on the ground that actual Fed municipal buying has not yet really started, and you get an idea of what supply/demand factors are impacting the municipal market.

Politics & Money: Beltway Bulls and Bears

- To the extent, there is anything to talk about politically these days with POTUS eliminated from doing big rallies and Biden stuck in his basement quarantine, the VP selection for candidate Biden will perhaps be the next newsworthy event in the Presidential election. The pressure is building for Biden to not select Elizabeth Warren, and various “shortlists” are circulating. Biden has already declared he intents to select a female running mate. From a markets standpoint, it is hard to imagine the decision will have much impact unless it is perceived as being impactful in the likelihood of winning or losing the race itself (and it never really is). For those who may view Elizabeth Warren in the VP role as a negative either for the Biden campaign or the country, I would point this out: Warren not being selected for VP (and I agree, it is highly unlikely) means she is free to be picked for something else … Would markets like to hear she is an actual regulatory role, as opposed to a mostly symbolic role like VP?

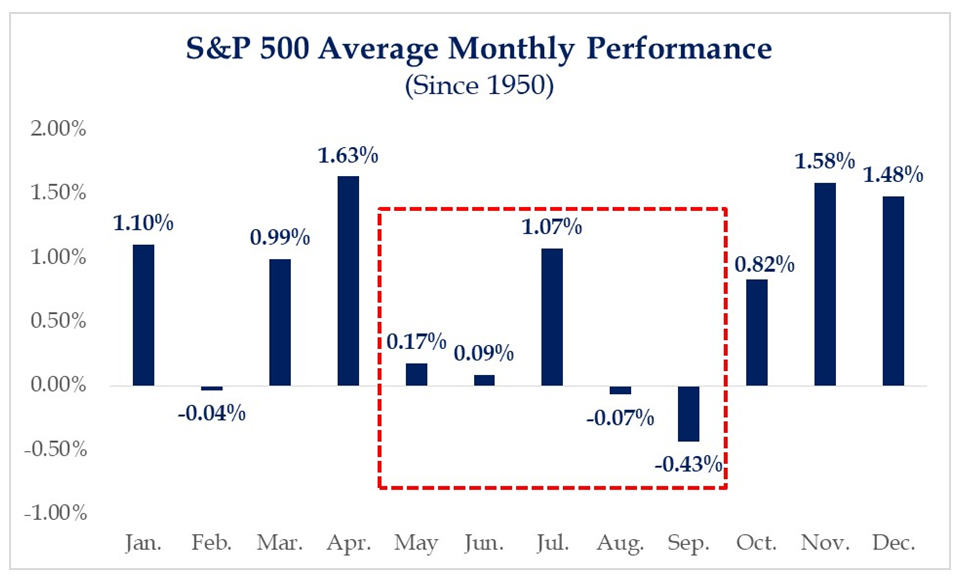

Chart of the Week

I have written dozens of times if not hundreds of times over the last twenty years about what I believe the fatal flaw to be in forming investment policy around “calendar trends” (first, they are riddled with exceptions; second, there is no causation to assume in noting the correlation; third, “averages” in past periods mean nothing to the next period). That said, the calendar averages around the next few months are at least anecdotally worthy of being shared with readers of Dividend Cafe.

* Strategas Research, Daily Macro Brief, May 1, 2020

Quote of the Week

“Courage is not simply one of the virtues, but the form of every virtue at the testing point, which means at the point of highest reality.”

~ C.S. Lewis

* * *

I congratulate you if you made it all the way through. We covered a lot of ground, I know. Join us Monday for our bi-weekly national video call. And reach out, always, with questions. Anything we can do to help you avoid the big financial mistakes. To that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet