Dear Valued Clients and Friends,

It has been an interesting week in the market, but as you will see in the first paragraph below it may seem like nothing happened whatsoever. That is more common than people think. Today we visit the state of the U.S. dollar, the “safe haven” of bitcoin, the politics of oil, the nature of contrarian investing, and more. Just a lot of easy-bite tidbits to edify you this beautiful spring weekend.

And before I remind you that a new and improved Dividend Cafe is coming any day, jump on in, to this Dividend Cafe!

|

Subscribe on |

Are you surprised?

As I am typing a couple hours after the market opened on Friday morning, with an Israel attack on Iran last night following Iran’s massive [thwarted] attack on Iran last weekend, after all of the market turmoil in the market the prior two weeks, the Dow is sitting at 38,000. It closed last Friday at … 38,000. Remember Bahnsen’s law for short-term market movements:

May go up a lot

May go up a little

May go down a lot

May go down a little

May be flat

I think you’ll find those five options will cover everything.

Some Electoral Action with the Strategic Reserve

I have been writing for nearly 18 months now about the various challenges the administration has had in refilling the oil stock they depleted from our Strategic Petroleum Reserves (SPR) in 2022. Some of it has been out of their control (refining costs not cooperating with the price of oil and the oil grade that we hold in SPR), and some has been governmental mismanagement (missing the mark in executing in the market when market conditions provided the opportunity to do so). As I have stated in a couple of places lately, my belief that, ironically enough, it is oil prices that represent the biggest upside risk to headline inflation in the next six months (something the Fed has basically no ability to control), several have reached out to wonder if I think the Biden administration might actually release more oil from the SPR in the [election season] months ahead. Understandably, many saw the outrageous release levels of 2022 coincident with the midterm elections to be convenient timing. My take is as follows: I have no interest in assuming the worst about politicians or in giving them the benefit of the doubt. Could I see a draw from the SPR (as opposed to the promised refill) if oil prices moved above $90 going into the summer? I suppose I would not be surprised by anything. But I would also suggest that the political backlash in something so cynical is likely worse than what one would be trying to remedy.

Dollar Confusion

I know, I know. We are supposed to be waiting on the imminent collapse of the U.S. dollar. In fact, no topic has seen nearly as much coverage in unique pockets of a certain sociological persuasion than various forms of dollar catastrophism. So you can imagine the confusion it generates when the actual Treasury Secretary of the United States issues a formal statement acknowledging the serious concerns of Japan and the Republic of Korea about the recent sharp depreciation of the Japanese yen and the Korean won. The dollar is rallying so much, and the currencies of other allies weakening so much that the three countries actually had to issue a statement inferring plans to intervene in these markets (i.e., for those wanting help reading between the lines, which is very understandable, they are talking about a coordinated effort for Japan and Korea to sell dollars from their forex reserves to support their own currencies). Just imagine what we are talking about here – the dollar’s fundamentals relative to other countries are so strong that governmental interventions and coordination are necessary to slow the dollar’s rise. If this is what the dollar bears meant, then kudos to them. Will they actually intervene, or was the veiled threat enough to send a signal to markets? Time will tell. But this is one area where I remain mystified at the persistence of those talking down the one currency that requires coordinated interventions to stop it from going up.

Contrarian Courage?

The S&P 500 is in the 90th percentile (and then some) in terms of its historical valuation. The Hang Seng, on the other hand (the Hong Kong index), is in the 4th percentile (trading 8x earnings). Who has the guts to enter the Hong Kong stock market at historically low valuations, with the imposition of CCP looming? Me neither.

Now, the UK, on the other hand … has traded at about a 20% discount in valuation compared to the U.S. stock market for nearly twenty years. The current discount in UK valuation relative to U.S. valuation? 47%. Hmmmm …

Contrary to Contrarian Wisdom

The underlying tenet of contrarianism is that consensus viewpoints are already reflected in the price of an investment, whereas out-of-favor views do not generally have a price where value is fully reflected. This is essentially true, and yet, of course, consensus views can get even more popular (read: excessive) before their reversion to propriety. More importantly, out-of-consensus views can often be wrong or, at the very least, require patience.

A better way to think about this whole subject is that with popular investments, you have the risk of overpaying, and with unpopular investments, you have the risk of being wrong. The opportunity comes where the price reflects the risk of being wrong and the risk/reward trade-off becomes favorable to the investor. It can’t be done perfectly, but it can be far more rewarding than buying with the masses. Ultimately, our version of contrarianism is to avoid crowds that behave like maniacs but also to avoid doing things just because others aren’t. Investing out of our own beliefs, philosophy, and processes seems like the most counter-cultural thing one can do these days.

Flight to safety

People can believe crypto “currencies” like Bitcoin are going to $0 in price or that they are going to $500,000. As long as everyone I care about understands that such speculations are as scientifically-grounded as a rain dance I don’t much mind anyone’s picking of a number out of thin air.

But when I set aside the “heads or tails” guesswork of this thing, a debate in which I confess my agnosticism, there is one thing that gets said in the Bitcoin world that ought to be, shall we say, “investigated.” And that is the idea that Bitcoin is a “flight to safety.” That when things are going bad in the world, bitcoin can be a place (like Treasury bonds) that investors choose to “hide out” in. I mean, what in the actual [blank] are people talking about? As Bitcoin routinely trades with more volatility than a doctom stock on margin in a third-world country during a terrorist attack, I am not sure where this narrative comes from (other than charlatans and liars who assume people can’t pay attention for themselves). Bitcoin dropped -9% in five seconds after Iran’s attack on Israel last weekend. It is down over -11% in the last few days but was up double digits in the month before that. Its correlation to the riskiest parts of the Nasdaq is tighter than any correlation you can find, and it is practically reverse correlated to traditional anti-fragile asset classes like Treasuries.

So believe it is going up or believe it is going down or don’t care whatsoever (bingo), but please don’t buy the line that it is a “flight to safety.”

Explaining the Fender Bender

Several asked why auto insurance was up so much year-over-year, impacting the CPI last month with his 22% year-over-year increase. It’s a fair question and not one I had thought about a lot other than to reflect on what the reasons were not (that is, some view that fiscal or monetary policy was inflationary for auto insurance but not for airfare or apparel). But with an h/t to Ben Carlson, I think the following thoughts seem prima facie reasonable to me.

Replacement costs of automobiles are way up because, well, auto prices went way up. This seems like a classic lag effect. New and used auto prices inflated in 2022, and voila, insurance prices inflated in 2023. The same principle can apply to parts and services as well.

Now, Ben also pontificates that drivers got worse over the last few years. I don’t know if that is true or not – I have never felt that many drivers belonged on the road, and that includes people I live with, but this take may or may not be at play. What I know is that the smart phone use and car accidents have gone up in tandem, so this seems logical.

Cronyism as a productivity issue

A free marketeer like yours truly bemoans the atrocity of crony capitalism all the time, and I largely do it on the basis of moral grounds – it is not right for the government to pick winners and losers, and a framework that rewards the big and powerful at the expense of the less-resourced is unbecoming of a fair and just society. And yet I don’t think we spend enough time pointing out that cronyism is also a productivity issue! It misallocates resources, it distorts price discovery, it creates a cost to taxpayers, it transfers expense from one party to another, and it undermines confidence in markets. It enhances risk premiums and introduces a regulatory burden on the private sector.

So yes, a productivity issue AND a moral one.

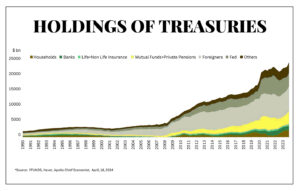

Chart of the Week

The Fed went to zero interest rates and quantitative easing in 2008. Foreign ownership of U.S. treasuries has not gone down in this period, it has expanded. The Fed’s ownership via QE bond-buying is the biggest change since 2008 (and since 2020), but it has come down a lot since 2022. Meanwhile, households are back as a big buyer, both directly and through mutual funds.

Quote of the Week

“Let us be thankful for the fools. But for them, the rest of us could not succeed.”

~ Mark Twain

* * *

I do believe the new Dividend Cafe is a game-changer. Having a Friday Dividend Cafe in line with what I have always done (macro commentary), a Monday edition covering all the current “things” (like we have done in DC Today for a few years), a daily market recap each and every day on the site’s home page, a variety of guest content from Trevor’s Thoughts on Money to Steve’s Alt Blend to much more, and finally a real-time ASK TBG to engage with your actual questions, I think the whole site will really simplify the delivery of our thought leadership yet expand the content itself. Of course, we will welcome your feedback along the way.

And with that said, send your questions, have a great weekend, and feel the peace that comes with an advisor who works for you. To that end we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet