Dear Valued Clients and Friends,

I loved writing the Dividend Cafe for many years with a “jump around” approach, basically covering a wide array of topics that would enter my orbit of interest each week. I made a decision late last year to start writing “single topic” and to write the entire thing in “one sitting” – basically Friday mornings – so as to make it a more coherent and cohesive read. I do like it better that way, and the feedback I have gotten suggests you do too.

Today is a little old school, which happens every once in a while when no singular topic is inspiring me. There are a number of things I want to look at today, from the Value/Growth discussion to the impact of debt on the economy to so much more. I did write it all in “one sitting” (yes, Friday morning – I am a serious creature of habit), but it covers a handful of different topics that entered my world this morning from a plethora of inspirations.

So off we go into the Dividend Cafe, a read that will be well worth your while.

One person’s bubble is someone else’s resentment

Charles Gave reminded me this morning of a line I had not heard in some time:

“A bubble is a rising asset price that I am not invested in.”

There is humor and truth to it, right? What so often drives people’s feelings about investments is what they want for their own interests. People want things to go up and be of great value when they own them; they want to believe things they are not invested in that keep going up are “in a bubble.”

And sometimes they change their mind very quickly, coincidentally just as their circumstances or positioning change.

A Presidential candidate five years ago said repeatedly throughout his campaign that “the stock market is one big, fat bubble.” Then, after that person was elected and the market went much higher (and I am very happy to concede much of its’s ongoing advance was his own policy portfolio of lower taxes and deregulation), he then (understandably) lauded the stock market hundreds of times.

I am actually not critical of that about-face – politicians innately present opinions around such circumstances and opportunities. But it almost humorously demonstrates a certain fact of life – that without governing principles, an evidence-based approach to investing, the benefit of significant experience, and other empirical means of forming a process of analysis, investors have nothing much to rely on but hope and alignment.

So how does one get to use the label “bubble”?

I have often argued that technically speaking, a “bubble” has almost always been attached to debt. When an asset is “over-priced” but not heavily levered, it doesn’t quite reach the level of “systemic” or “bubble.” But “over-priced” can still be a very bad outcome for that investor, and so putting aside the semantics, some degree of price consciousness seems quite appropriate in our estimation.

I also believe labeling an asset or asset class a “bubble” based on a metric that more or less ALWAYS labels something a bubble is quite unhelpful. The CAPE Schiller index is a good example, and many media or newsletter writers cling to it like it is the Bible, when in fact it seems to be a great way to identify something as over-valued, no matter what. You can imagine those conditions make it hard to make beneficial investment decisions.

Some Rules of Thumb

(1) When everyone takes for granted that something just can’t be over-priced, that is prima facie reason to start being skeptical. Another way of putting this – crowd optimism, confidence, and euphoria are not confirming indicators of price legitimacy; they are cause for skepticism.

(2) Excess crowd euphoria usually means the 6th or 7th inning, though, not the 9th inning. Those last few innings of crowd euphoria are where disciplined, value-conscious investors are most tested. See: Buffett, 1999. Burry/Paulson, 2007. Many more examples to cite.

(3) Any time you hear anything remotely sounding like “it’s different now” or “valuations / cash flows / fundamentals / [fill in the blank] don’t matter anymore” be very, very nervous. The hubris of people who lack any economic foundation or true north is worse than their sub-par intelligence.

(4) Excess stability does, indeed, lead to market instability. This is the great contribution to my worldview from Hyman Minsky. Complacency sets in over time, and market distortions become invisible. This does not help with timing, but it is a cyclically indisputable part of financial markets. This is one of the reasons I like volatility in equity markets, if I could just get all our clients to like it as we do – extended periods of low volatility always seem to be setting us up for something unfortunate.

(5) There is no reason to ROOT for something to be in a bubble. This is not personal. The type of person who cheers someone else losing money is an unattractive personality (or much worse). My opinions of “hot tech” or frothy valuation spots in the market is not an aspirational opinion; it is an objective one based on past experience, economic valuation, and evidence-based mean reversion realities. It is also, absolutely, forever and ever, not something I care to time. I have never offered an opinion on the timing of any of this because I do not believe I or anyone else can time such a thing.

Where Value Gets Hard and Growth Gets Stupid

It has been said that value investing is buying a dollar for fifty cents and that there simply isn’t that kind of opportunity set anymore. I think it is certainly true that easy opportunities to buy things that are mismatched from fair value are hard to come by.

But I also think that paying $1.30 for what MIGHT be worth, well, $1.30 someday (and could be worth less) is not exactly exciting growth investing, either. Growth investing is supposed to be paying full price today for what may be worth a lot more later. Value guys don’t like paying full price, but good growth managers knew that paying full price was fine if the future growth of revenues and earnings made it worthwhile. But paying the FULL FUTURE price today simply means asymmetrical risk and reward, and not to your favor.

Did someone say China?

Far be it for me to make it a whole Dividend Cafe without mentioning China, but I do feel it noteworthy that it is not just direct exposure to Chinese equities that has hurt investors this year, particularly in the Chinese internet sector or other niche growth industries. U.S.-based companies with significant revenue exposure to China have lagged as well – not necessarily with negative returns but certainly subpar ones.

And I would add, while our theses on Chinese currency and Chinese sovereign debt have stood out impenetrably over these last couple of months, the Chinese High Yield corporate sector (that we have avoided through and through) has gotten hit as well.

That bifurcation in the thesis about risk-adjusted opportunities in Chinese risk and spread assets vs. the sovereign/currency paradigm is incredibly important.

Lower for Longer

As the Fed gets ready to begin their quantitative easing tapering, and as I begin to mute my television more often than normal, it is worth looking beyond Fed activity on their balance sheet, and to Fed activity with the Fed Funds rate.

In 2018 they were raising rates a quarter-point every meeting, while forecasting more rate hikes into the future, while speeding up their “quantitative tightening.” Markets eventually revolted (Q4 2018) and the High Yield market froze. The central bank hit a point where they “went too far” and they then had to do a rather humiliating about-face.

I see almost no chance of them taking that chance again. My best guess is that they leave the Fed Funds rate in place all the way through the entire tapering of bond purchases (wherein they are still adding to their balance sheet, not subtracting it), and for some time thereafter. But this is the most important part – getting off of zero to 25 or 50 basis points is practically a non-event, other than its signifying value.

The worry list

Bloomberg last Friday gave a list of ten things investors should be worried about. I thought it hilarious that #1 and #2 on their list were not even anywhere on my list (i.e. Delta variant and Washington’s fight over the debt limit) – I mean literally not on my list. It also had some issues like “central bank plans to dial back monetary stimulus” whereas my list has “central bank plans NOT to dial back monetary stimulus enough.”

But the truth is a list of items investors who have a 20, 30, or 40-year time horizon should be worrying about in the next 20, 30, or 40 days is utterly absurd. There are short-term issues that are damaging to consumers, producers, and the economy (i.e. labor shortage, supply chain, limited capacity ports, etc.). But long term, I believe the list is primarily cultural, and heavily centered around a growing dependency on the Fed. Energy prices this month and food prices last month and this Congressman’s fight with that Senator barely stay in the headlines day-over-day, let alone decade-over-decade.

Closing thought

We still mostly have a market-based economy in the United States, despite occasional moments of inconsistency. But we increasingly have a market-based economy with a flawed system of capital – distorted cost, distorted access, manipulated liquidity, etc. Thus far most of those distortions have been to the benefit of investors. That is not sustainable. Boom-bust cycles have two words in the hyphenation.

A market-based economy is one of modernity’s gift to us.

A flawed system of capital cost is becoming our gift to the next generation.

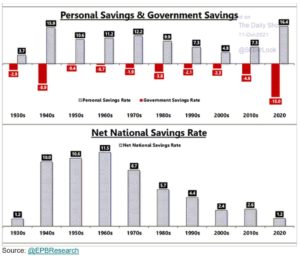

Chart of the Week

Don’t let the vast volume of bars in these two bar charts throw you off. My fundamental thesis about future growth is that …

growth comes from greater productivity,

productivity comes from greater investment,

and investment comes from greater national savings …

And in fact, Investment = National Savings, such that a decline in National Savings MUST mean a decline in investment, which leads to a decline in growth (inevitably).

What this chart shows is the relative stability in the Personal Savings Rate over the last eighty years (with the decade of the Great Financial Crisis being an outlier), yet the National Savings Rate collapsing decade by decade as government borrowings (the inverse of savings) erode at the aggregate level. I believe the domino effect is entirely predictable.

Quote of the Week

“We don’t have to be smarter than the rest. We have to be more disciplined than the rest.”

~ Warren Buffett

* * *

Thank you for taking this week’s ride in the Dividend Cafe. Enjoy your weekend. There is a 0% chance USC will lose this weekend. That’s all I have to say about that. In the meantime, we are here to answer your questions and do our part to ensure that your discipline as an investor will meet the moment when it counts. To that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet