Dear Valued Clients and Friends –

I thought it appropriate to devote this weekend’s Dividend Cafe to the election, now that this long-awaited event is almost here. I thought about calling it an “Election Eve” edition, but considering 82,042,050 people have voted as of press time pre-market on Friday, which is about 64% of the total number of people who voted in all of 2016, it hardly feels like “election day” is “election day” … Hopefully it will just be the day they count the votes.

One way or the other, we are well into voting (28.3 million people have voted early in-person; 53.6 million people have returned mail-in ballots; 36.7 million people have outstanding mail ballots, and then there are all those who vote on Tuesday). And we are getting closer to this year’s election being over. It has been the strangest election season I can remember when all is said and done.

I already wrote a more extensive Dividend Cafe on the broader investment implications of this year’s election. There is really nothing I would change in that piece, yet I thought some more specific reflections today may be useful going into the actual election. The day after Election Day, we also will be hosting a national video call to debrief what we know and don’t know and lay out some perspective, forecast, and general takeaways 24 hours later …

But today in the Dividend Cafe, we’ll make it a little more personal, a little more specific, and with apologies to those looking for me to throw punches, a lot less tribal. Opinionated? Yes. Fiduciary? Above all else. Objective and fair? To that end, I work.

Two Themes for Markets

There are a couple of plotlines that will play out next week as far as markets are concerned. Investors will see prices impacted throughout the week by two different major themes:

(1) The certainty, clarity, and timeliness of a result – any result

(2) The results

So before #2 can impact markets – and #2 includes who wins the Presidency, which party controls the Senate, what the margin is in the Presidential race, what the margin is with the Senate – all of those actual empirical results – we first need #1 to play out. It is not just possible that we will not know #2 next week, but I would say it is in the range of 60-70% probable. I expect #1 to be more of the story in markets next week than #2. Now, #2 (results) will have their day, but markets can (and do) discount known realities. Why #1 matters is that markets can’t get discount very well the very concept of uncertainty (in case you are wondering, that is a tautology).

Geography meets politics

How could this play out next week as far as category #1 goes? Well, if the results that do come in Tuesday night show Florida to be a lost cause for President Trump, it really does pretty much mean the Presidential election is over. No analyst I am aware of, and certainly no one inside the Trump campaign, believes they can or will win the race without Florida. We may not get a concession speech Tuesday night, and we may not know the results in all other states, but if Florida were to be crystal- clear going against Trump, that would at least tell markets how the Presidential side is going to go.

But here’s the thing – that is highly, highly unlikely to happen. Not only if President Trump neck and neck with Joe Biden in the polls in Florida, but Florida is famous for tight races and even recounts, etc. Republican Governor Ron DeSantis, and Senator Rick Scott, both won their 2018 elections in Florida on a night that saw mostly Democratic wins across the country, after trailing in polls coming into the race, and in a spectacularly close fashion (both races were razor-tight).

In other words, Biden may win Florida, and Trump may win Florida, but I don’t expect a crystal clear, quick, large margin result in the early hours of Tuesday evening.

From there, all eyes will be on North Carolina and Pennsylvania. A surprise win in New Hampshire for Trump would stir things up but isn’t likely to happen. And a Trump loss in North Carolina (he won in 2016) would start to hurt his electoral college odds, but it would not in and of itself be a knockout (like Florida would). If into the earlier hours of the evening the prospects are looking good for Trump in all three east coast states (Florida, Pennsylvania, and North Carolina), it will probably excite Trump fans, and it will certainly mean we’re not getting a clear result any time soon. In that scenario, even a Biden win would only come about after more states, and close/contested races are resolved.

As we head west, other states will start to become significant. Iowa, Ohio, Michigan, and Wisconsin will all get significant attention. Polling looks good for Trump in Ohio and Iowa, but not a sure thing. It does not look good in Michigan or Wisconsin for the President from a polling perspective. Of course, he won both states in 2016 and was not expected to, but one thing I believe has never been fully appreciated was how unbelievably close those margins were.

As we go west from the rust belt, most polling and campaign rhetoric (from both sides) expect Biden to win in Colorado and Nevada, with Arizona becoming a potentially significant state in determining results (another reason besides tight margins in other states that we are unlikely to know a winner Tuesday evening).

A political prognosticator I am not

I would not look to me as any kind of expert in forecasting this race. I have studied all polls, betting odds, and talked to more campaign insiders and political scientists than anyone you have ever met. Still, my own instincts believed Romney was going to win in 2012 and believed Hilary Clinton was going to win in 2016. I was wrong about both.

So, yes, I can tell you that my general feeling is that FL, PA, and AZ will determine the election result, meaning that Biden will win Wisconsin and Michigan (if he doesn’t, Trump will be re-elected), but you would infer expertise in my feeling at your own peril. A simple way to summarize expectations:

Trump has to win Florida and Pennsylvania and hold North Carolina, Iowa, and Ohio. He can lose Michigan and Wisconsin from his 2016 map and seems posed to, but if all these other states are held or too close to call, we are looking at a nail-biter.

Biden has to win Wisconsin and Michigan, then pick off one state between Florida, Pennsylvania, and Arizona.

Both sides have a path. Polls indicate an uphill climb for President Trump. If you talk to strong supporters of either candidate, you will hear a compelling and impassioned case for why their guy is going to win.

I can see a Biden win on election night.

I can see a nail-biter that Trump ends up winning.

I can see a nail-biter that Biden ends up winning.

But if Trump is holding his own in FL and PA on election night, I still don’t see how we would know he has it won with all the late voting and mail-in ballots to count in the days ahead. And from there, it could break either way.

So yes, I expect #1 (back to the top) – uncertainty, “wait and see”, volatility – to play out next week, with a few wildcards potentially taking such away.

The ‘world’s greatest deliberative body’

But then there’s the Senate. To recap, the Republicans have a 53-47 edge right now, and are very likely to pick up a seat in Alabama (the one they lost in the special election when Roy Moore was the nominee – good memories, ay yi yi). So at 54-46, thinks start pretty strong for the GOP and then go down from there. Polls indicate that McSalley in AZ and Gardner in CO are very likely to lose, so unless those polls are just a total disaster, that brings things to 52-48. Then the close races are expected to be: Maine, Montana, Iowa, and North Carolina. If three of those four go to the Democrat challenger, that will tilt the balance of the Senate to a Democrat majority.

This assumes that the Democrats do not win Georgia and that the Republicans do not win Michigan or Minnesota. In Georgia, I do expect the Republican nominee to win, but their “run-off” system will mean a fresh vote in early December as two Republicans are splitting each other up on Tuesday. And I do not expect the Republican challenger to win in either Michigan or Minnesota, but the polling margins do not render it totally impossible. So we shall see …

In these four races (Iowa, Maine, Montana, North Carolina), all four could go blue, all four could stay red, or there could be some combination in between. Iowa and Montana look best for the Republicans, and North Carolina and Maine look best for the Democrats. Some of these states are not super easy to poll. This just isn’t something that is setting up to be predictable, one way or the other.

Not all majorities are created equal

One thing I will say is that if the GOP holds their lead in the Senate, I will be very surprised if it is more than 51 or 52 seats. And if the Democrats take the lead, I think it will likely be with just 50 or maybe 51. This is important, because some of the legislation or appointments or approvals or what have you that investors may fear has a different hill to climb if it can’t have any defectors at all versus if there is a margin of 3 or 4 votes. This applies to both parties and could make for a very important asterisk on the results.

Personnel is Policy

In the event that Joe Biden is elected President, one of the first things markets will look to is his choice of key cabinet appointments to get a feel for the ideological direction of policy. Talk will escalate quickly from all networks about an Elizabeth Warren appointment to Treasury Secretary (some to push for it, some to create fear around it), but candidly, I would be shocked if he went that direction. We know that Warren wants that role, but it strikes me as very unlikely for a lot of political, pragmatic, and agenda reasons.

In the event that President Trump is re-elected, a lot of current first term players are likely to head out of D.C. (pretty common), and a fair amount of seats will need to be re-filled. Personnel vetting and appointments have been a mixed bag for this administration, and it could create some uncertainty in markets as to whether or not a new cast of characters comes in that is ready for prime-time or if they seem less polished and experienced. I know of some senior officials who I believe have been agents for good in the economy and market that I do believe would look to move on if there were a second Trump term.

So for both candidates, there are some unknowns around personnel that will matter to investors.

Okay, what else matters in the aftermath of the election?

So the Presidential race may be resolved this coming week, or it may not. It may be close, or it may not be. It may surprise people, or it may not. There may be a stunning rebuke of Trumpism in the results, or there may be a stunning rebuke of progressivism in the results. I don’t know. And contrary to popular belief, I have much less of a dog in this hunt than is popularly assumed. Yes, I went door to door for Reagan in 1980 as a 1st grader. But I do not believe my ideological commitments are really represented by either candidate, and I have written about this plenty. I feel I have been an impartial and fair commentator over the last four years, evidenced by how many people on both sides of the aisle get mad at me. =) So when I say what I am about to say, it is not with a leaning for one candidate over the other (I can criticize both all day long) or a partisan bend. This is meant as a purely objective statement of fact:

The heat, polarization, toxicity, and emotion around this election is not economic, and it is not related to markets, and everyone pretty much knows that. It is cultural. It is entirely cultural.

And whoever wins this election will win with a mostly evenly-divided country on matters of cultural import more than economic.

And what our country has to deal with in front of it is largely cultural, as well.

And I love my country, and I pray these sources of division can and will be addressed. But as this is an investor writing, I believe that while there is obvious economic overlap in the culture wars and ample areas of significant economic policy relevance in the aftermath of this election, the primary tensions and questions in front of us are about issues less central to markets. I truly believe this to be an incredibly non-controversial statement.

But ????

So with that said, let’s look at a few specifics and a few nitty-gritty issues that, while not the main subject at the family dinner table, are relevant to investors with political and electoral connectivity:

(1) Capital gain taxation – earnings multiples have always declined when increases in capital gain taxes have passed. Do we know this will happen? No. Do we know when it will happen if it does? No. But we do know that it is part of Joe Biden’s platform, and it seems possible to do two things: Cause investors to sell certain high gain assets in 2020 believing they would face a higher capital gain tax later; and put downward pressure on earnings multiples later.

(2) Private equity – the carried interest PE sponsors, achieve (where their promote interest is taxed as cap gain and not ordinary income) would be backdoor-eliminated if the cap gain rate was equal to the ordinary income rate, as this arbitrage would go away. It would affect the after-tax compensation of private equity GP’s but not much else, and there are compelling policy arguments both for and against this change (in 2016, Donald Trump ran on eliminating the carried interest advantage). The other area pertinent to private equity is the idea, floated by some policymakers on the left but not addressed by Biden specifically, to eliminate the deductibility of corporate interest expense. This is highly unlikely to happen, in my view, and will be watched closely.

(3) Big pharma – in every election cycle of my adult life, more so in the last few than the first few, we have heard that some policy idea or another posed an existential threat to the pharmaceutical industry. In 2016 it was particularly concerning as both candidates were campaigning around who would be the bigger thorn in the side of the drug industry. Well, returns have been just fine through the Trump administration, as they were in the Obama administration, and Bush before that, and Clinton before that. I think policy suggestions on the margin should be watched but I do not believe the pharma and biotech industries in our country are touchable. If we learned anything from COVID, our nation wants our drug and biotech industry doing what they do – creating life-saving and life-enhancing treatments.

(4) Health care – however, almost half of health care spending in our country is government accounts, so reimbursement rates matter. We take a less favorable view of the insurers and managed care companies due to the permanent policy overhang and recognize that risk exists with pharma as well (to a lesser degree).

(5) Energy – I won’t get into the environmental merits of each candidate’s position here, and some of the policy positions are hard to pin down (which is not uncommon in politics), but there is a general feeling that Trump is more friendly to the oil and gas industry than a Biden administration will be, which I suppose is fair enough. The only thing I would point out is that it hasn’t mattered much in the past – oil and gas were on a tear in Obama’s first term and have had awful results in Trump’s term. Non-political factors drive returns more than political ones, apparently. That said, I believe it behooves investors to be aligned with the companies that benefit from more pressure and regulation in the industry, as the larger players pick up market share when the smaller players are snuffed out.

What both candidates will never have to deal with

There is not a single issue involved in this election as relevant to investors as the national debt, the monetary policy implications of the national debt, and the inflation/deflation debate that these dynamics create. Investors will be directly impacted by all things liquidity, all things credit, all things interest rates, and all things deflation/inflation – exponentially more than any of the aforementioned policy topics (as important as they are).

And there is no result from the 2020 Presidential election that is going to change this broad category relative to another result. Put differently; I expect four years of high government spending, of zero percent interest rates, of disinflationary headwinds, of bond yields at zero, of a highly interventionist central bank, and of abundant credit and liquidity, under a President Trump, and under a President Biden. It isn’t like one candidate is running on trimming the size of federal spending, and the other is running off the opposite. It isn’t like one candidate wants a tighter Fed than the other does. It isn’t like one candidate can wave a wand and deal with the collapsing velocity of money tied to low rates and high spending. I could go on and on.

In ten years, many investors will talk about how what they got right and wrong about these topics impacted their portfolios; very few will talk about the specifics of the 2020 race.

One final thought …

I know some of you are big Trump supporters, and I know some of you are big Biden supporters. I am writing to you as investors, not politicos, not partisans, not fans. I love talking about policy any time, any place, though I insist on doing it thoughtfully and lovingly, not belligerently and with the threat of friend and family relationships on the line (sorry, I don’t go there). But no matter what you’re policy and candidate inclinations are, as an investor thinking about the future, for good or for bad, I ask you this question:

Do any of you believe that we will not get a vaccine if the candidate you support loses?

And – do any of you believe that they are not going to pass some form of additional fiscal stimulus if the candidate you support loses?

I believe we all should know that both of these things are going to happen regardless of who is President. And it seems to me investors are more focused on those two things than anything else (at least as it pertains to 2021). For what it is worth …

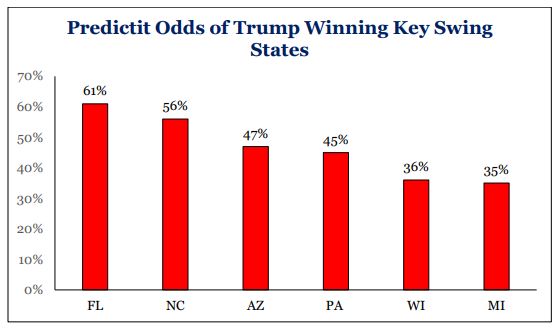

Chart of the Week

Why I believe it could be a very close race in the end (electoral college):

*Strategas Research, Policy Outlook, Oct. 28, 2020, p. 3

Quote of the Week

“There’s more to citizenship than voting, and partisanship is not patriotism. If casting a vote is all you have in you, then, fine — by all means, do what you believe to be best. But consider the possibility that the duty of the patriot in these times is … to insist that the free and self-governing men and women of this struggling republic deserve better than what is on offer. We can have better than what we have had because we can be better than what we have been.”

~ Kevin Williamson

* * *

Here’s wishing you and yours a lovely calm before the storm. I look forward to delivering next week’s Dividend Cafe for a lot of reasons. Join us for the call on Wednesday. Cast your vote. And reach out any time, any place. We are here for you for the entire next four years, and there are no term limits to our fiduciary duty.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet