Dear Valued Clients and Friends,

There are a couple things going on right now at The Bahnsen Group that make this a very fun time of year, and a very fun edition of the Dividend Cafe. I wrote last week about the annual money manager due diligence trip I have done since 2006 and how important it is to our business (and to our clients). The meetings of the last couple weeks, this year, coincide with the launch of our “Operation Magnify,” the largest portfolio undertaking we have ever experienced at our firm.

So today’s Dividend Cafe takes the reasons Operation Magnify became necessary, juxtaposes it with this COVID moment (what it supposedly means, what it most definitely does not mean, and what some think it may mean), and then applies lessons learned from our recent meetings and collaborations.

I am aware the world is mostly focused on the election event coming up a week from Tuesday, November 3. There very well could be ample uncertainty and market volatility that comes as a result of the election (or the non-result). It would be difficult for me to devote much more attention to that subject than I have.

But the topics I want to dive into today are leaps and bounds more relevant to investors, long-term, than whatever uncertainty volatility the election results create. And like many understandings of the connection between politics and our portfolios, I believe the topics I am addressing today are riddled with misunderstanding.

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.” (wrongly attributed to Mark Twain).

Let’s jump into the Dividend Cafe!

The Magnify Moment

I suppose it is fair to say that nothing prompted our Magnify campaign more than the reality of zero percent interest rates, and a yield curve up and down the term structure at or near zero. But in fairness, I really believe the separation of “Credit” from “Boring Bonds” in evaluating a portfolio, in constructing a portfolio, in addressing cash flow needs, in thinking about severe distress moments, and in thinking about capital preservation, should always have been separated. I understand why the mutual fund industry and consultants have enjoyed blending the two together into one “bond” category, but frankly, if I ever start comparing my rib-eye steak to my creme brulee, we have a problem in the logic and function of such an exercise (and my doctor might say we have two problems).

So yes, “Boring Bonds” becoming a 0-1% return expectation asset class is a big deal, and magnifies some realities in capital markets. But it isn’t peripheral. It isn’t for bond investors to deal with. It isn’t anecdotal.

Learning to crawl before we walk

All risk assets, and all financial assets, are priced against the risk-free rate, always and forever. On a relative basis, the way we talk about cash, mortgages, credit cards, borrowing, stock returns, FANG, portfolio goals, risk, results, and everything else in the orbit of capital markets, is fundamentally a by-product of interest rates.

The price of money drives almost every conversation one can have about money. If I have not communicated clearly on this over the years then I apologize from the bottom of my heart, but the centrality of money’s price (i.e. interest rates) is fundamental to understanding economics, and certainly to understanding investment finance.

And understanding economics and investment finance are fundamental to understanding the delivery of financial advice. Get A or B wrong, and C will be a disaster. An unmitigated disaster.

Professional resentment

This is why I hold so many in my profession with such contempt. It is not because they are my competitors (I am way too arrogant to actually believe I have competitors; just kidding) … It is because I find it incomprehensible that someone could get paid fees to delivery advice and to execute on a plan that represents someone’s hopes and dreams for peace and contentment, and would do so with disregard for the fundamental realities of money.

I met with a doctor-client this week who shared with me his frustration at the lack of intellectual curiosity in the medical world, and the lack of passion for applying science to the realities of humanity. It hit me that I am not alone at feeling frustrated with those in my profession, and in this case, the reasons are nearly identical.

The price of money (credit) drives everything, and to NOT re-investigate portfolio assumptions and asset allocations and risk tolerances and return expectations in this ZIRP (zero interest rate policy) moment is malpractice.

Taking the pejorative out of Boring

Boring Bonds may need to be a larger part of some client’s allocations. March’s equity collapse may have caused them to realize they emotionally desire LESS volatility, not more. But Boring Bonds have paid 3-5% for a hundred years, and they will pay 0-1% for a long, long time. They offered big risk mitigation from severe distress in times past. Mathematically, and with other country precedents, we see that as impossible going forward.

But …

They offered capital preservation for a hundred years, too, and continue to do so.

So the process must start with that trade-off. What sacrifice to income and/or return are you willing to take for the capital preservation benefit, without the other two historical benefits. It’s that simple.

Maybe 20% goes to 30% because of emotional needs.

And maybe 25% goes to 0% because you invest to make money, not park it.

But we have to start there.

Magnifying the rest

From there, we have to look to the “additional equity” categories besides our core, basic baseline (dividend growth) on which all portfolios are driven. Some clients have a need and desire and ability to supplement the growth of a portfolio with non-dividend strategies filled with equity risk. These “growth enhancements” allow us to go into emerging markets, small-cap, innovation/technology, and other such arenas, where volatility is higher, income is zilch, but potential total returns are higher. Some clients want no such thing, or at least shouldn’t want any such thing.

On the other hand, some clients need significant cash flow from their portfolios, and can take equity level volatility for a premium to income/cash flow … These “income enhancements” are not individual companies (stocks) like in our Dividend Growth portfolio, but rather are strategies or solutions we only want where premium cash flow is needed in the portfolio (i.e. preferreds, BDC’s, some EM high dividend, etc.).

Properly placing and weighting and evaluating those Growth and Income Enhancements has been a pivotal part of the Magnify process.

Alternatively speaking

We believe in most cases – not all – investors are underweight to alternative strategies that diversify sources of risk and reward in an investor portfolio. And we really, really believe this now (with an S&P over 20x forward earnings and a bond yield well less than 1%). Investors may want or need more equity volatility exposure, but they may not. And yet that return expectation and risk mitigation formerly held in Boring Bonds likely needs re-thinking. The world of hedge funds, real estate, private credit, private equity, middle markets lending, global macro, etc. is not remotely “risk-free” – but it ought to be somewhat “risk different” from the volatility risk in traditional equities. Talented managers are hard to find, but market inefficiencies, relative value arbitrages, and event-driven moments can be a major source of portfolio alpha. I am beyond proud of our track record in identifying such managers and sourcing access to such strategies. And we want to Magnify this across portfolios right now.

When you are not thirsty

And then there is illiquidity, which could very well be a subset of the alternatives category, but warrants differentiation for this reason. Alternatives have a “sale-ability” to them, even if only on an annual or quarterly basis. Some investment opportunities in the Direct and Illiquid space may have no liquidity at all, yet may be a tremendous source of return and opportunity, only for very select and specific investors. And this has become a major source of priority for us with our higher net worth client portfolio allocations.

Core Thinking = Core Dividends

After the Boring Bonds get set, and as we sort through the right allocations for peripherals and enhancers and alternatives and illiquids and all the things … at the basic core of the portfolio, is Dividend Growth. That represents our underlying philosophy in its purest form. And I am sure no one would say I have failed to talk about this enough.

Do I like it when the stock prices in those dividend growth holdings go up at a faster speed than the S&P 500? The answer is “huh?” I don’t care about it. You shouldn’t either. This was also well covered last week. But let me be less philosophical about this (generally beware people who go around taking pride in “not being ideological” – who in the world wants to get advice from someone proud of having no worldview or anchor to a set of beliefs?), and instead be very selfish.

On one hand, when stocks in our dividend growth portfolio go up faster than the stocks in the S&P 500, which happens in many years, there are plenty of clients who love it. That is nice, I guess. But for the 55% of clients who are reinvesting dividends, they are doing so at higher prices, not lower ones. And for the constant flow of new money, we are responsible to steward, we are buying at higher prices, not lower. Forgive me for not understanding why that is a good thing.

And yet on the other hand, apart from a terminal date of selling all the stocks, why the horse race of prices vs. the market matter is beyond me. If we desire perpetual portfolios with perpetual wealth creation and cash flow generation (we do), the whole conversation strikes me not as a good thing, or a bad thing, but just not a thing.

What IS a thing – is the sustainability of dividend growth inside our client portfolios, either to the benefit of those who withdraw the income or to the benefit of those accumulating more shares of future income generation.

Period.

Enough Magnify – let’s talk COVID

So yes, the national economy was shut down earlier this year in the initial phase of the COVID experience. And yes, much of the economy is still waking up or is re-opening incrementally. Ground zero for economic pain and uncertainty is in the lower end of the labor market where many hourly workers in the food/beverage, retail, and especially hospitality industries have been furloughed or laid off. And from a revenue deterioration standpoint, it is almost entirely in those same sectors, with no area hit harder than Travel and Leisure/Hospitality.

Some of the economic pain comes from the unavoidable tragedy of the moment. Some of it comes from certain public policies that are so stupid and unfair it defies moral and logical imagination. And some economic pain is transitory, already on its way back to normalcy.

It has been a scary year, a bizarre year, a frustrating year, a tragic year, and in the context of investors, an entirely unpredictable year (besides for those countless people who knew COVID would be the thing it was, and that the market would drop 36% in 31 days, and then recover as quickly as it did, etc.; those were the same people who got out of the market in 2007 and back in early 2009, and they are the same people who eat all the french fries they want and have 5% body fat).

But investors risk making huge mistakes if they draw conclusions from the COVID moment that are wrong. Allow me to lay out a summary of some key [truthful] takeaways I already see solidifying themselves in the economy and in the market:

COVID is not a disruptor, it is an accelerator

At first glance, this may seem really insensitive, but I do want to totally clarify what I mean. COVID has been incredibly disruptive to those families who suffered loss, and incredibly disruptive to those who got extremely sick and went through the scare of requiring medical care to get through it. It has been incredibly disruptive to those who lost jobs because of shutdowns, or who lost revenue because of ongoing draconian restrictions that seem to lack logic and thoughtfulness.

What I mean here, though, is that the lingering economic impact will be to accelerate trends that were already in place pre-COVID, that are not now disruptive to those trends, but accelerated them.

Food delivery was growing rapidly before COVID; that went parabolic during the shutdown. Younger people finally buying single-family homes in suburbia was happening pre-COVID; it has escalated substantially. Rates were very low before COVID. Now they are zero. The sunbelt was the nation’s hottest market before COVID (no pun intended), now it is, well, still the hottest market – just even hotter than before. San Francisco was falling apart before COVID; now it appears to face an existential crisis. Technology companies were becoming bigger tenants in NYC than new finance companies before COVID; now the big tech names are increasing their footprint in NY offices even as finance companies need less office space. Some states were running large unfunded pension liabilities before COVID, now they face financial calamity. Brick and mortar has been handing over market share to e-commerce for over 20 years; now it jumped up a couple years worth of pace in a couple months.

I could go on and on, and I actually have dozens of more examples. Hopefully, you get my point; COVID has been an accelerator of the pace of certain economic trends already in place, and that must be understood differently than how many are perceiving things.

What does COVID not mean?

I do not believe it means the death of offices, the death of amusement parks, the end of air travel, or the end of people going out to restaurants.

What lies ahead

I do not know what Governors and Mayors and future Presidents will do, so the policy side becomes the temporary unknown on the way to normalcy. But I do believe our society will learn to live with COVID, and I believe we have ample information now to do just that. I believe that outside the media and a few select politicos, the large preponderance of society understands it to be the highly infectious disease it is, often asymptomatic, with nearly indetectable fatality levels for many segments of the society. And that with that, I think most people know we must protect our most vulnerable, identifiable as they are by age and health, and take the precautions necessary to keep them safe. Our society is up for that task, and yes, when a vaccine comes it will help the whole cause. But in the meantime, what lies ahead is the great historical reality of HUMAN ACTION. Humans crave community. They crave recreation. They crave entertainment. And yes, they crave sitting down at a steakhouse with their friends or family or clients (okay, biographical interruption there).

It must be done safely. But it will not become obsolete. Ever.

Pent-up demand

Do I believe the areas most hurt by COVID (travel, leisure, hospitality) will be the areas that benefit the most on the other side? Yes, I do. Because I discount some perpetual fear and trepidation? No, not at all. But I know human action, and I see in the data know the unquenchable thirst people have to take that vacation, to get away to a hotel for a weekend, to do dinner with their family, to re-engage the norms and activities that give their life respite or happiness. That demand did not go away; it has built up, and it is going to be met with supply in due time. Timestamp this.

In conclusion

I will spend more time on money manager meeting takeaways next week. But where we stand now, we have a lot of uncertainty, we have been through a lot, and we have learned a lot.

And life is going to come back, just as restaurants are, entrepreneurs are, and just as Central Park already has.

What I want for all investors is to marry the two things well in their outlook – that there is nothing new under the sun, and certain deeply embedded institutions and norms are not going away from a coronavirus, and yet many trends and movements have picked up speed. And your portfolio (for clients of The Bahnsen Group) is well-prepared to Magnify all of this.

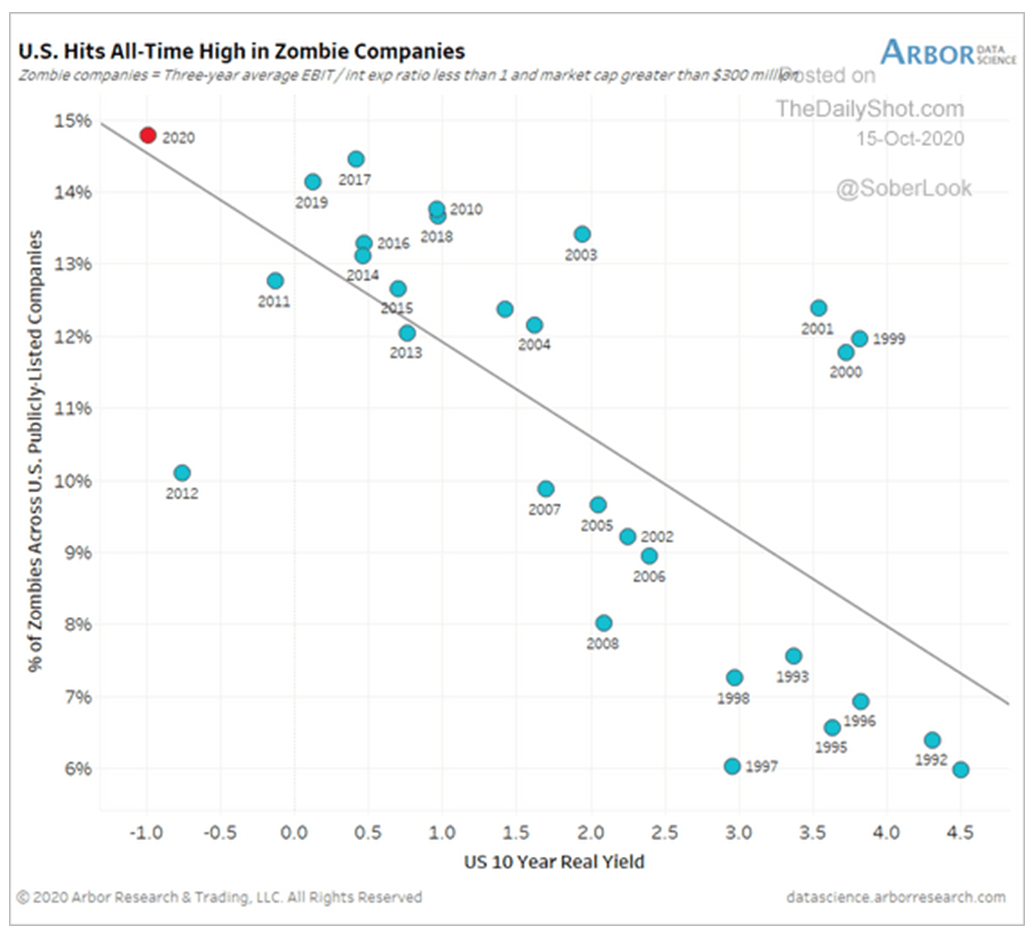

Chart of the Week

This week’s chart requires a little explanation. A “zombie” company is essentially one that is functionally dead, or should be dead, but is contrary to sound wisdom, allowed to stay alive. Intuitively, many people may believe a company staying alive that should be dead is a good thing (who wants businesses to die, after all). But the problem is that productivity is maximized in an economy when resources are allocated to their best use. What you cannot see when you see a dying and unsuccessful company left on life support is the productivity, job generation, profit optimization, and innovation that would come from those resources being deployed into more capable hands. Put differently, the short term gain of leaving a zombie company alive is more than offset by the long term cost.

Companies of a $300 million market cap or greater that have an earnings divided by interest expense ratio of less than one (that’s a pretty darn good definition of a zombie company when they earn less than just the interest cost of their debt) are now at the highest level they have been in history. What makes for this high percentage of “zombie” companies?

You guessed it – a central bank providing “permanent liquidity” through monetary policies that help such companies avoid their natural fate. In the most crude but economically cogent way of saying this, the economy is hurting by letting so many companies stay afloat when those resources could be better allocated elsewhere.

Quote of the Week

“How small, of all that human hearts endure, that part which laws or kings can cause or cure.”

~ Samuel Johnson

* * *

We remain fully engulfed in Operation Magnify, day by day, client by client, account by account, portfolio by portfolio, and we are loving it.

Reach out any time, clients and friends alike, and may all that you care about in your life be magnified.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet