Dear Valued Clients and Friends –

You’ll only have to read a few sections of today’s Dividend Cafe to be reminded of the uncertainty that exists around the world today. Europe may seem to have rectified some parts of their uncertainty, but they invited new uncertainties in doing so. The U.S./China tensions are not solving themselves, and you may have read somewhere that COVID case growth hasn’t solved itself yet either (highly contagious viruses are interesting, that way). It is a both unavoidable and unsettling reality of life right now – many conditions, globally and not just domestically, are uncertain.

So perhaps it was appropriate that I chose to throw in the middle of this week’s Dividend Cafe a little refresher of some of the most basic investment principles I believe in, applied to the methodology The Bahnsen Group has built its business around – dividend growth. The sequence in which things happen is not always as intentional as I may like to pretend, but in this case I think it is highly apropos.

I couldn’t make light of all the uncertainty in the world right now if I tried to, and yet I am a beneficiary of rich and zealous appreciation for history that helps me to navigate such uncertainties. No part of studying history gives anyone a crystal ball for the future, but it at least provides perspective and context. No, my friends, the world was not more stable in years gone by, or decades gone by. What changes is never the existence of uncertainty, only the shape and size and packaging.

It was around that uncomfortable reality that my appreciation for dividend growth grew as an investment philosophy. 1960’s social unrest – clip some dividends. 1970’s stagnation – clip some dividends. 1980’s growth – dividends. Roaring 1990’s into a tech bubble – dividends did just fine, thank you very much. Tech implosion. Dividend names still alive and kicking. Lost decade – not for dividend growers. Etc, etc. The only challenge I have run into in my professional career managing dividend growth is when people believe “other things are doing better, even as dividend growers are doing well.” Yes, that is an objection I can live with just fine. But here’s the thing about all those decades, and the five decades before those – each had monumental uncertainty. Geopolitically. Technologically. Economically. Wars. Weather. You name it. And yet, somehow someway, underneath the surface of a very unstable world, there are companies who generate cash flow by delivering goods and services in a free enterprise system, optimizing the glorious division of labor that free markets have unleashed, and sharing those cash flows with us.

Uncertainty in history, uncertainty in the future. And through it all, the time-tested benefits of cash flow generation inside free enterprise. We will survive. We will thrive.

In this week’s Dividend Cafe we will cover …

- A summary of the market week that just was

- The top ten things to remember as a dividend growth investor in the COVID moment

- All things China

- The United States of Europe?

- The difference between an investor and a speculator, and where the danger lies

- Speaking of speculation … a blast from the past!

- What the Fed is doing (and not doing) as it pertains to government debt, and why it matters to you when you think about interest rates

- Why not all commercial real estate is created equal right now

- Where a very unnoticed and under-appreciated opportunity may exist right now in the financial sector …

- The pros and cons in today’s energy infrastructure realities

- The basic economic report card of the week, from airline travel to hotel traffic to plenty more data points giving us light on what is going on in the economy around us

- Politics & Money

- Chart of the Week

With all that said, let’s dive in to this week’s Dividend Cafe.

Market redux

Coming into Friday morning, the market is completely flat on the week. We had been up roughly 350 points the first three days of the week, then down 350 points on Thursday. As of press time, the market is down a hundred points a couple hours into Friday morning market action. The bulk of the market volatility this week has been in the Nasdaq.

Top Reminders about Dividend Growth

I do not believe I repeat enough the basic principles behind our belief in dividend growth investing. If there is one thing I wish I did better in these pages it is reiterate with the appropriate level of repetition the evergreen and timeless nature of the principles behind dividend growth investing. I shudder to think I would ever give the impression that certain macro conditions matter in making it more attractive or less attractive, at a certain point in time. We believe in dividend growth investing for all the right reasons, which are principle-driven, never tactical, seasonal, or cyclical. You can decide which of these factors may or may not be more standout-ish during this period of time.

(1) Companies positioned to support dividend growth are companies with strong balance sheets and defensible business models. In other words, they are better companies.

(2) Dividend growth investing provides a consistency of cash flows for investors who may need such a thing in their financial objectives.

(3) Market volatility affects the price return of a portfolio, but dividend growth investing immunizes or protects the portfolio from the impact of price volatility on the underlying cash return.

(4) Dividend-paying companies have historically out-performed non-dividend paying companies with lower levels of volatility, in full cycle periods of time. Not every month. Not every year. But when looks at 5-year, 10-year, 20-year cycles, dividend vs. non-dividend paying companies have easily measurable metrics in both performance and volatility.

(5) Dividends have historically represented about half of the total return of an equity investor. To rely much less on dividends is to either assume a lower total return expectation, or believe somehow the price appreciation you receive will be much higher than it has historically been.

(6) Dividends do what accountants and regulators and shareholder groups often can’t do – hold management in check! Inefficient capital allocation happens with bad M&A deals, ill-advised capital projects, or excessive stock buybacks that may be poorly timed. A cultural commitment to dividend growth regulates capital allocation in the C-suite, and has historically led to less bad decisions and more prudent ones.

(7) A period of secular low interest rates makes bonds less attractive and boosts demand for where dependable income and growth of income may be available

(8) Stock prices are set by Fundamentals and Sentiment. Well, the fundamentals are essentially at the end of the day different ways of looking at a company’s cash flows. Stock prices often trade off of sentiment and expectations. Sentiment is exponentially more volatile than Cash Flows are. Ergo, the more you are relying on fundamentals, and less reliant on positive sentiment, the less volatile and more predictable of a portfolio you will have.

A period of huge disproportionate demand for “big tech” and other non-dividend components of the market have led to an embedded discount in how dividend payers have functioned in line with the market index. But never forget: Financial assets are mean-reverting instruments.

Dividend growth cannot be indexed. Historically consistent dividend payments matter a lot, and can be measured in a passive construction. But a commitment to future dividend payments is qualitative and cultural. No index can monitor or capture these components.

Escalation with China

In the middle of the week the U.S. announced it was closing the Chinese consulate in Houston. Markets mostly shrugged it off (what’s a consulate? why should I care?). On Friday China’s Foreign Ministry announced it was revoking the license for the U.S. consulate in Chengdu. Many analysts (okay, this one) had to google Chengdu to understand why I should care. And truthfully, I didn’t care much more after the google search than I did before it.

The right mentality about all of this is probably somewhere in between. No, these two consulates closing are not the dawn of a new cold war. But I would not ignore the increasing tensions in what is right now a cat fight, either.

Little shots here and there do not mean much, but in the broader narrative of increasing tensions between the two super powers, it is another dimension of uncertainty in an already uncertain world.

Did Europe just get investible?

As mentioned this week in COVID & Markets, the European Union agreed this week to a 750 billion euro stimulus package ($860 billion dollars) – an unprecedented fiscal response as a collective. Member states (27 of them, to be precise) had to unanimously agree. The program will give out 390 billion euros in grants and about the same in low-interest loans.

What is most noteworthy is not the stimulus itself, which will likely have varying degrees of success and efficacy like most government programs. Rather, it is the solidarity behind it where effectively you have Germany now explicitly providing support to Italy, etc. The deal is being funded by debt that is backed by the collective European Union – a “mutualization” that has not existed until now. It is a step of economic integration that has a lot of pros and a lot of cons to it, depending on your views of a lot of things. Monetary union without fiscal union has always been the achilles heel of the European Union. They just got one step closer to fiscal union, which in theory strengthens their, well, union.

What it doesn’t do is make it more investible. More focused efforts on a real fiscal union may make more consistent the policy landscape of the European Union, and it may grant more power to a centralized body to issue debt, raise taxes, and direct funds, but it can’t create economic growth. It inevitably and inherently hurts some countries (long term) and helps others (short term), and does so for the purpose of maintaining the European Union. As we learned from Brexit, though, countries are not obligated to stay if they wish to leave. And “doubling down” on the European Union with debt mutualization may firm things up within the union, but it doesn’t do anything to keep countries on the losing side of the union in it.

Short term, it is a positive stabilizer for the Euro currency and bond markets. Longer term, it does not address what is at the heart of present European challenges.

Wisdom that has stood the test of time

From the greatest value investor of all time, Buffett’s mentor and guru, Benjamin Graham:

“The problem … is not speculation per see; speculation has always been part of the market and always will be. Our failure as professionals is our continuing inability to distinguish between investment and speculation. If the professionals can’t make that distinction, how can individual investors? The greatest danger investors face is acquiring speculative habits without realizing they have done so. Then they end up with a speculator’s return — not a wise move for someone’s life savings.”

Maintaining an understanding of the difference between speculation and investing, for good and for bad, with cost and benefits to each, is a deep commitment at The Bahnsen Group. To that end we work.

Putting valuation concerns in perspective

Whether it is those big tech companies trading from 40 to 140x earnings, or looked at differently, 10x top-line revenues, some form of valuation concern surely must exist even for the most bullish of big tech bulls, right? I was reminded this week of a gem of a synopsis from former Sun Microsystems CEO, Scott McNealy, on the dotcom/tech bubble valuation of his company … (h/t Louis Gave)

“At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends… That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that assumes you pay no taxes on your dividends, which is kind of illegal. And that assumes with zero R&D for the next 10 years, I can maintain the current revenue run rate… Do you realize how ridiculous those basic assumptions are? You don’t need any transparency. You don’t need any footnotes. What were you thinking?”

This week’s reminder that the Fed is not buying all the government’s debt

From late March and into May the federal outlays from CARES Act commitments (and the “normal” deficits government already was set to run) totaled about $2 trillion above revenues to treasury, and the Fed’s purchases of treasury debt in that time period was, well, about $2 trillion (not quite, but close). Since then, the government has added about $1.5 trillion or so more to deficit spending (i.e. actual outlays for expenses above and beyond actual revenues received), and yet the Fed has added about $85 billion or so to its balance sheet. In other words, the government has funded over $1 trillion of deficit spending in the last six weeks without any support from the Fed, and without any increase in interest rates.

There are a couple implications to this: (1) At least for now, there is an appetite for the safety and liquidity of U.S. Treasury debt, regardless of interest rate; (2) The Fed has significant latitude – if it wanted to use it – to buy even more government bonds with money that doesn’t currently exist (quantitative easing).

The point of #2 is not related to smooth functioning of market operations, and normal liquidity in the market. We already know the Fed has said they will take a “whatever it takes” approach to all of that. But those worried about interest rates going higher on longer term debt (or hoping it will) just have to realize the Fed has a big backstop sitting there, waiting, ready, if it deemed it necessary to hold rates in place. That is fighting a very large object.

As for the market’s appetite for the next $1.5 trillion of deficit spending (on the low side of what we expect Stimulus 4.0 will cost), let’s just say I do not expect Treasury will find as many non-Fed buyers lining up this time for the next trillion or so of debt issuance. Maybe I am wrong, though. We do seem to live in a bizarro world right now.

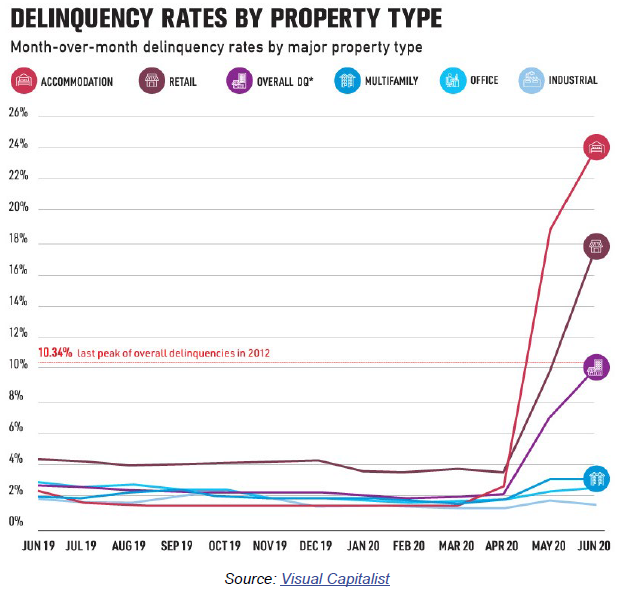

Not all Commercial Real Estate is Created Equal

The delinquency rate on commercial mortgages is very different for hotels than it is for apartments, office, and industrial. There is still a lot of uncertainty over what ultimate arrangements will be made in the hospitality space, but what we do see is really very stable performance of cash flows in the multi-family, office, and industrial world, and obviously more uncertainty in the areas more directly affected.

* Over My Shoulder, Mauldin Economics, July 23, 2020

Everybody is so worried about Gordon Gekko

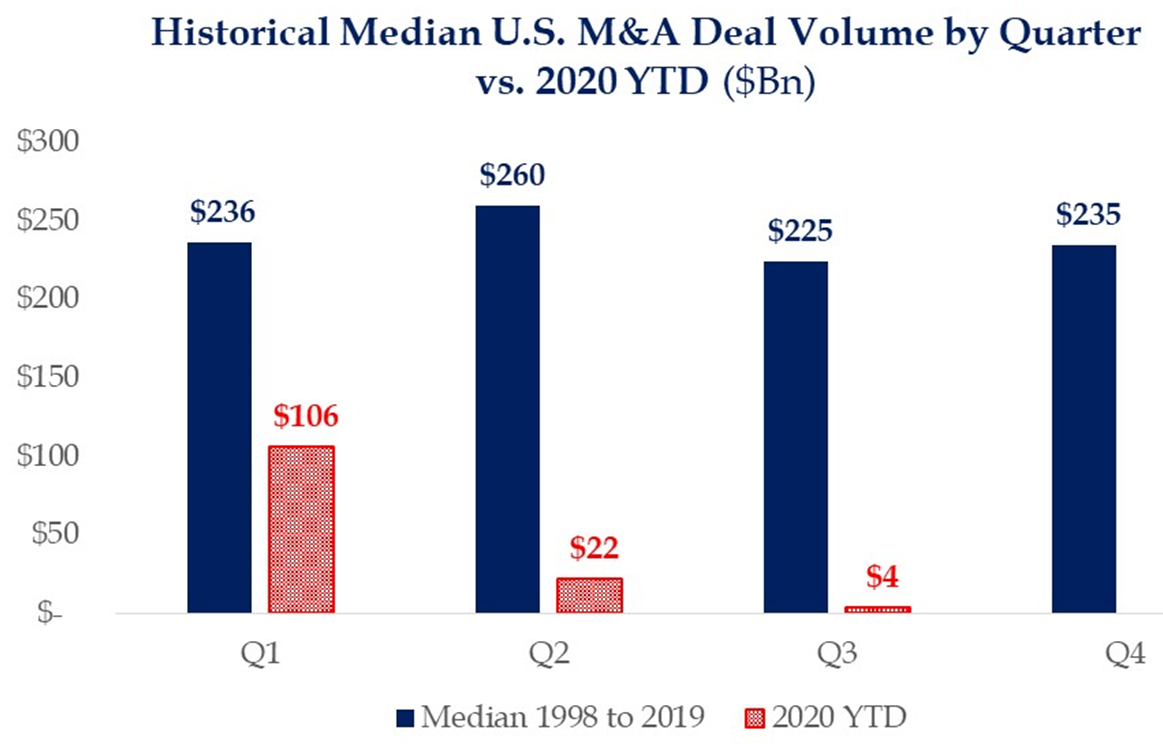

Investment bankers may not be atop many people’s list of concern during the COVID crisis, but individual class envy aside, an investment point is worth making about the future of M&A when we come out of this period … Most focus on the mega-banks has been on their loan book (and loan loss provisions), and net interest margin in the low rate environment (never mind that NIM is always focused on curve steepness, not absolute level of the 10-year bond). But I would suggest that investment banking activity is being ignored unwisely. Growth through acquisition is going to be a bigger part of our economy post-COVID, as (a) Low rates facilitate transactions, (b) Organic growth is harder to come by, and (c) More companies need/want to sell/transact.

The pent-up demand in M&A right now and across corporate finance is like something I have never seen my entire career. When it plays out, no one knows. But I believe “financials” must be more than deposits and loans into the future.

* Strategas Research, Daily Macro Brief, July 22, 2020

Pros and Cons

I thought this quote from Howard Hinds, an Infrastructure Portfolio Manager I have been reading on MLP’s for nearly a decade was a just outstanding encapsulation of the good news and bad news in the energy pipeline space:

“Energy and Midstream investors are waiting for things to get back to normal, too … The market doesn’t appear to have much hope on that front. The pace of renewable development, the disdain for fossil fuels in the global community seems to be an overwhelming trend.

The implication for investors is a new normal that requires a quicker payback and a lower terminal value. For MLPs, it means higher upfront yields to compensate for the market’s reluctance to place a residual value on the infrastructure that’s critical today and could not be replaced in the current regulatory environment.

This new “grand bargain” could mean that midstream yields will remain higher than historical average for longer.”

Income investors will like this. Those not invested for the long-term, the real under-current of the story, where the highest quality assets lie, will not. Midstream energy infrastructure is fine. But the balance sheets of many companies are not. Selectivity matters.

Economic Check-in

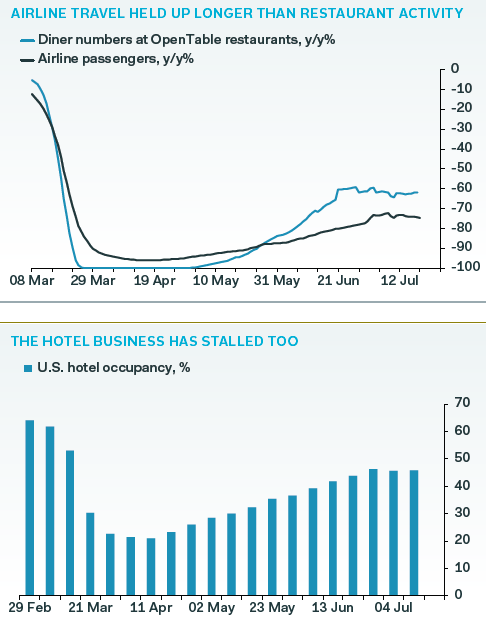

- Let’s start with airlines and hotels – way down, then nice pick-up, now a stall …

* Pantheon Macroeconomics, U.S. Economic Monitor, July 20, 2020, p. 1

- Shipments of desktops and laptops increased 11.2% year-over-year in Q2, which is obviously a by-product of the shutdown and e-learning landscape. But it happened.

- Initial jobless claims moved higher this week – not good. Continuing claims dropped quite a bit this week – good.

Politics & Money: Beltway Bulls and Bears

- The polls continue to point to the same lead for Joe Biden and the betting odds have not moved much either. I am hearing an increasing amount of people reference not believing the polls, and that will stay steady throughout the next few months. It will be interesting to see if late July polls reflect any tightening of the race since early July. My paper on full election ramifications to markets remains in heavy research and preparation.

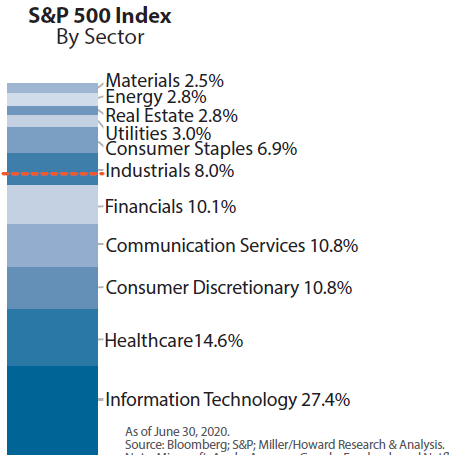

Chart of the Week

Does this sector concentration look familiar to any of you who once partied like it was 1999?

Quote of the Week

“Reading the financial press is bad for your financial health.”

~ Charles Gave

* * *

I hope you have gotten something out of this week’s Dividend Cafe. Enjoy your weekend. Reach out with questions and comments. And be certain of this, uncertainty is the old normal.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet