Dear Valued Clients and Friends –

I wrote last week about an understanding of “trade-offs” being one of the defining characteristics of a grown-up, and what that means when applied to the life of an investor. Indeed, we make decisions around our finances every day that reflect either fully conscious trade-off thinking, or at bare minimum, sub-conscious, beneath the surface calculations. I greatly appreciated the feedback I received regarding this instructive.

This week I was enjoying my morning run through Central Park when a parallel hit me, and in reflecting back on my own writing of a week ago it put things in perspective for me. I was in California working from home for the entirety of the quarantine period (mid-March through late May). I have always been an early morning person, but market conditions and the general state of affairs had me waking up about 45 minutes earlier than even my normal wake-up time. Every single day of quarantine, I worked in my home office from about 3:15am until 5:45am, and then went for a run in my neighborhood. Every day. I had to do it for mental health, but I also know without my normal gym routine and such I risked putting back on the weight I had lost since mid-2019 (I was down 25 pounds over the prior nine months). I loved the morning run, and I have been determined to keep it going as my post-lockdown life has brought me to different settings.

This brings me to Central Park. It is a pretty special place to run. But there is one big difference from my daily quarantine run in Dover Shores … There are some serious runners in Central Park at 5:45am each morning – I mean, really serious. I want to be fit, and I want to feel good about myself, and when I see some of these other runners blowing by me, let’s just say I had a moment of feeling somewhat sub-par. This is where my trade-off reflection came in …

I want to be fit in my suits, but I also love food. All things being equal, if there were no corresponding trade-offs, would I like to really, really be in shape? You bet. And maybe one day I will be. I won’t give up on my daily runs no matter what – and I am trying to reasonably moderate my food intake (it is harder in New York than California, because New York has good food). But here’s the thing … whether I want to admit it or not, and whether I realize it or not, my decisions around my health, my fitness, and my weight are all trade-off decisions. I can’t look like those runners blaring past me in Central Park, because I am running three miles, not ten; because I am eating a ribeye, not tofu; because I work 16 hours per day, not eight. Trade-offs. I have the life I want.

The way in which all of this can be applied to COVID is another conversation altogether, but I will stay in my lane here. Investors can pretend all they want that they can look like a long-distance runner in Central Park, and eat at the steakhouse a few nights a week, but it is a lie. Volatility and expected returns are inevitably connected. The income generation of an investment in a time of zero interest rates is correlated to some risk – volatility risk, liquidity risk, something. And there is not necessarily a wrong answer. One level of risk is appropriate for one person and not for another. And one level of return (or income) is adequate for one person but not another. Each has to deal … with trade-offs.

For every 6% body fat runner, there is some not-exactly-thin investment manager who is fitting in his suits, and who really likes his dinner.

Trade-offs, indeed.

In this week’s Dividend Cafe we pour into the state of the economy, and cover all of these fascinating topics:

- A market summary of the week that just was

- Where the next stimulus bill may be heading

- Why QE is not acting like debt monetization (yet)

- What commodity prices are doing and what it tells us about “reflation”

- The tensions municipal bond investing now create, and why

- Fear and volatility as “lower but still really high”

- What Europe is doing (maybe) to address a key structural impediment

- Our Economic Progress Update (which we are now doing each and every week), with this week’s focus on credit card spending, small business optimism, industrial production, auto sales, and more)

- Politics & Money – why the market may be pricing in a Biden victory but not a change to corporate taxes

- Chart of the Week

… and so much more

My run is done and I am ready for a trip to the Dividend Cafe!

Market redux

I am typing this on Friday morning before the market has opened and the futures are pointing up 100 points, but coming into today we are +700 points on the week). The market has not gotten back to the 27,500 post-COVID closing high of June 8 since then, but is now within 2.5% or so. The major story of the week to me is the market’s resilience (three weeks in a row) against coverage of the COVID pandemic, case growth, and even tightening state restrictions.

We hit the heavy part of earnings season the next two weeks, and plenty of questions persist about how open the economy will be going into the fall. It is all moving very fast.

Ticking time clock on Stimulus 4.0

Why is there allegedly a mad dash rush to pass a multi-trillion dollar stimulus (or relief) bill? Well, in a slightly longer period of time, there is some point at which many city and state budgets are going to be devastated, and some form of what is in the plans coming out of both political parties is what these states are counting on to deal with these shortfalls. But there is a few weeks if not months for most of those situations, so while not exactly pleasant, it isn’t the textbook definition of imminent. But that $600/week federal supplement to unemployment insurance runs out in two weeks, and there are two arguments about this (both of which are reasonably valid).

One, is that it must end – it is artificially propping up unemployment by paying some people more money to not work than to work. Two, also legitimate, is that the economy is still requiring a safety net and there is a massive fiscal hole in national income for the lower income rungs displaced by government shutdowns.

I won’t veer into policy recommendations in these pages (I assume you know I do plenty of that as a leisure activity). Let’s just say that addressing both of the issues in my preceding paragraph can be done, and must be done. A $300/week compromise is something I hear is likely to have bipartisan support.

The talk of the White House is rejecting a bill if it does not have some form of payroll tax cut is interesting, as I really thought it was possible POTUS was giving up on that fight. The market has not discounted the possibility of getting temporary payroll tax relief, and if it does happen in some measure that would be well-received by markets.

Inclusion of a payroll tax cut would certainly mean needing to push the total cost much higher than $1 trillion, because relief to states and some unemployment extension/modification are not going to be cheap. The most market-sensitive component is not, in the short term, the total price tag, but probably the business liability protection that will have so much to do with getting people back to work.

I believe direct payment to taxpayers will happen again, but this time to a lower tax bracket threshold.

I really don’t know if there will be legislative support for specific restaurant aid, but I know the executive branch is open to it.

So many moving parts …

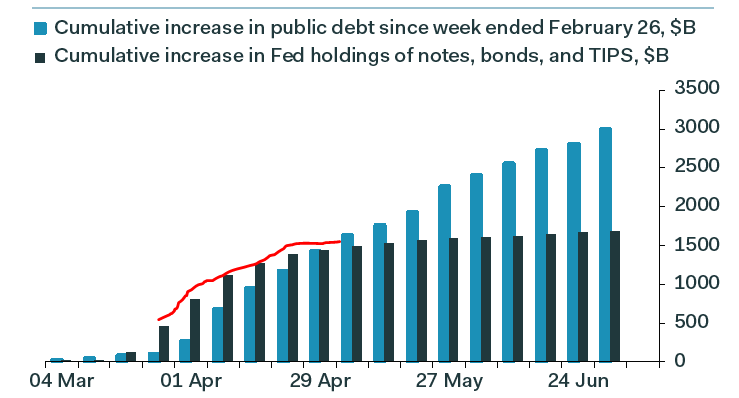

QE not Monetization

Several things are true at once. The Fed’s increase in purchases of treasury debt in the COVID moment was a sight to behold ($1.5 trillion in about a month from late March to late April). And, the level of cumulative increase and total balance sheet size remains astronomically high (and is likely to grow higher. But number 3, the growth of debt at the Treasury level has continued to skyrocket from late April through present, even as Fed bond buying has subsided dramatically. In short, the Federal government is running deficits, and the Fed has not been the buyer. The market appetite for Treasuries at sub-1% rates is a sight to behold.

* Pantheon Macroeconomic, U.S. Economic Chartbook, July 2020, p. 5

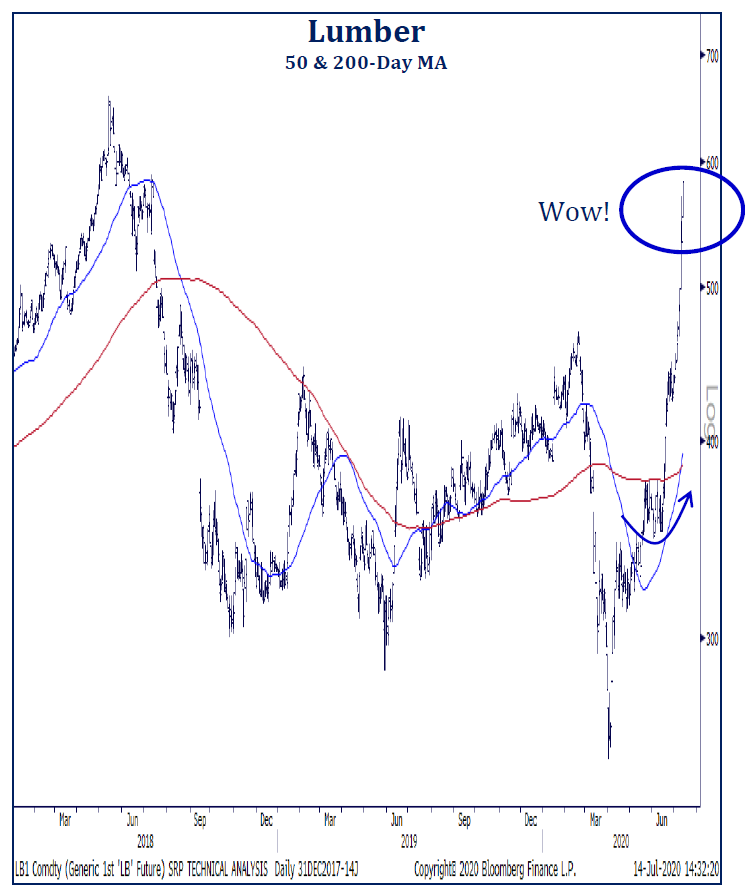

About that reflation trade …

One would think this tells you a little about the appetite for construction and building right now (because I don’t think it is fireplace season) …

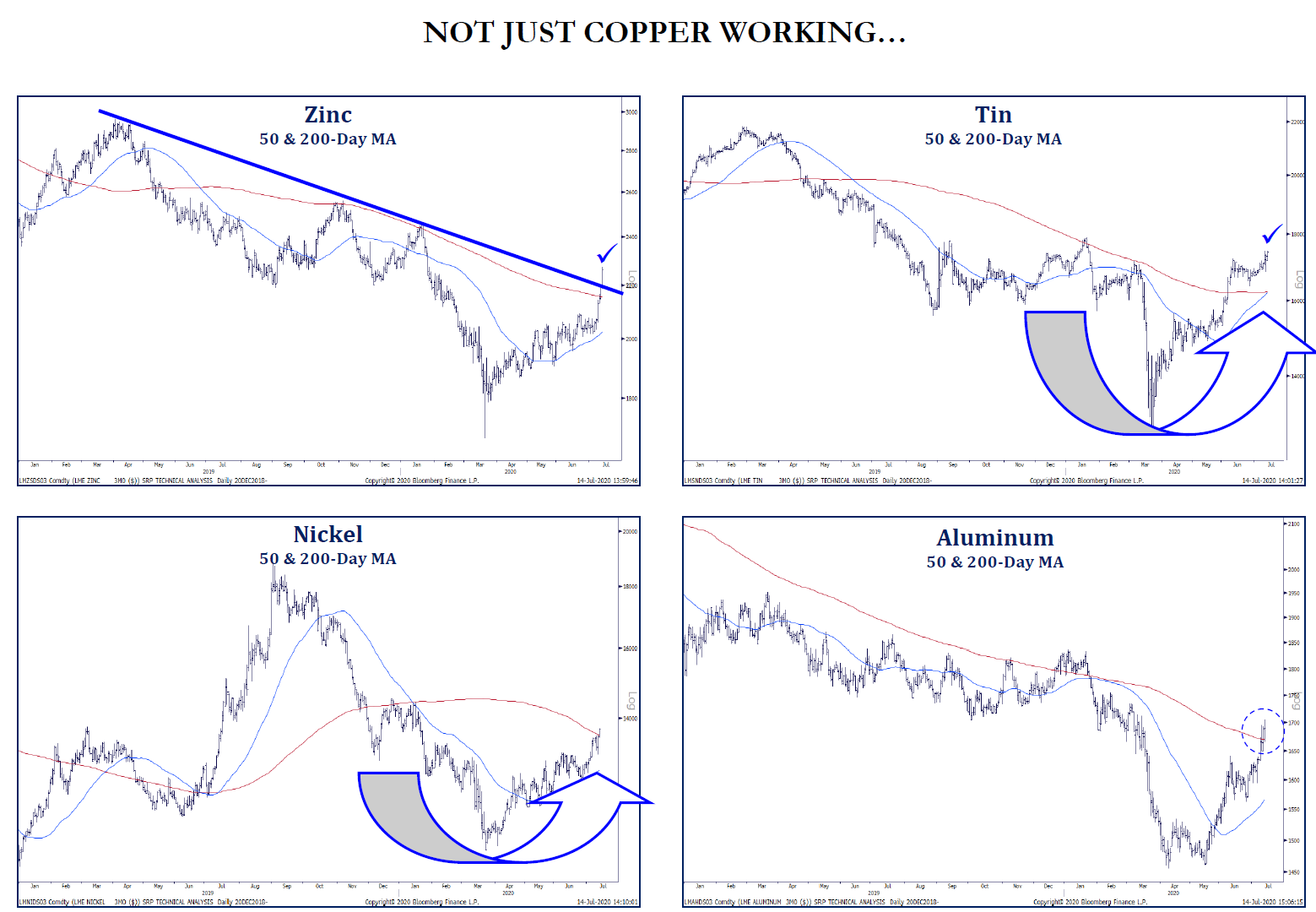

But then the confirmation in industrial metals really seems to speak to that broader reflation narrative, more than likely on a global scale …

* Strategas Research, Technical Strategy Daily Report, July 15, 2020, p. 14

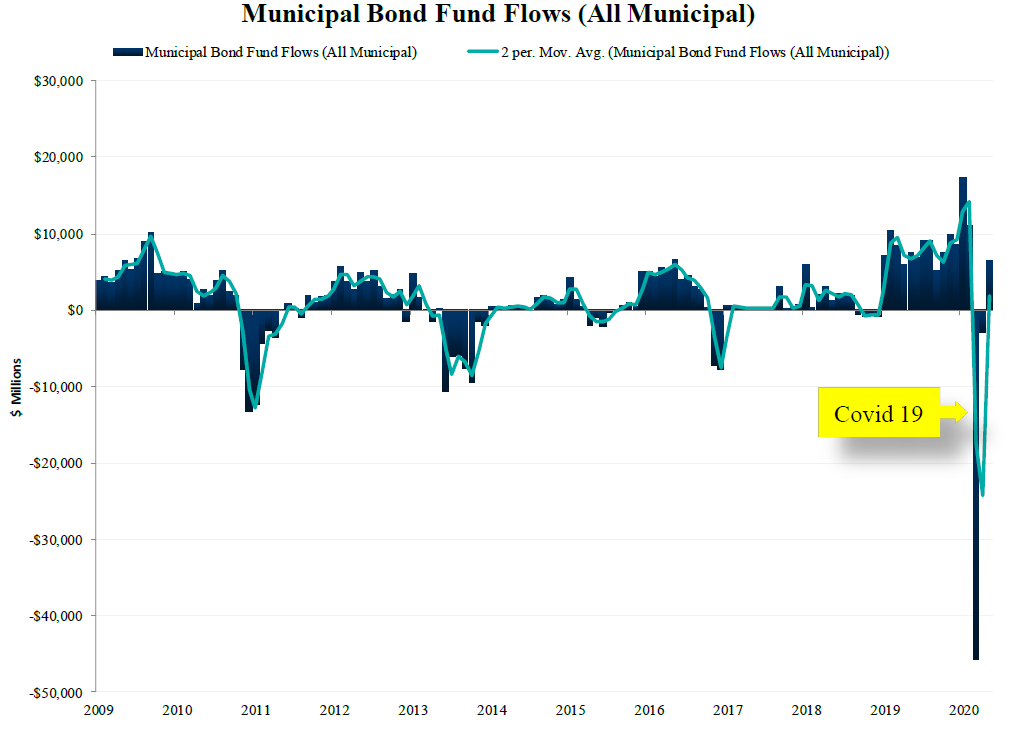

Municipal Tensions

I have talked a lot over the last two months (and thought about it 100x more) about the anxiety I feel about the long-term realities now being re-embedded in “bonds that act like bonds.” The basic thesis is that I remain fully convinced they serve as a great hedge in “really, really painful risk-off times,” and yet unlike most of the last 75 years there will no longer be a carry benefit – a positive coupon – during normal times. We won’t get paid any longer to hold these diversifying assets for the bad periods. I am working through the solution.

But Municipal bonds create a challenge all of their own. Do they even provide “bonds that act like bonds” benefits during periods of extreme distress? The lesson of recent times, is no. It may not last long, but in big equity sell-offs, the municipal space is so dependent on retail inflows, and retail investors are so keen to sell everything, that munis have been positively correlated with equities in truly distressful times.

* Cumberland Advisors, Lipper, Bond Markets Through the Virus, July 16, 2020, p. 6

This means that one of two things can happen: (1) Spreads stay wide enough in munis that they offer a reasonable return in normal times, but no hedge benefit in extremely bad times; or (2) Spreads compress, and munis provide no hedge benefit in extremely bad times, or reasonable return in normal times.

Volatility: Down, but not Normal

Obviously the “fear index” is substantially reduced since the explosion higher in March. But it is important to note that where the VIX has “settled” at is still nearly double its average, and is basically right in line with the four or five other “spurts” of the post-crisis decade. In other words, the cost of buying equity protection right now, while nowhere near COVID peak levels, is around the same as all the other dramatic moments of the last ten years.

![]()

Keeping our eye on Europe

In the midst of the mid-week U.S. stock market rally some may have been distracted by a couple other events taking place: (1) The Euro hitting its high vs. the dollar since the COVID moment began, and (2) European sovereign bond yields hitting their lowest level since the COVID moment began, most specifically ground zero of their trouble – Italy.

Why all of the risk on and positive vibrations across the pond? This €750 billion Euro fund is getting closer and closer (the first ever break from their long, long, vehement policy against “mutualization” of debt). A deal will mean that the first time there are funds collectively issues and collectively backed but dispersed to individual countries, It is done under the pretense of the COVID crisis, but it sets the precedent of stronger nations actually taking on the risk of the weaker ones, etc. Of course, to some degree, with a shared currency and through their various banking systems, they’ve all had contagion risk for years; but this is the first step towards formally admitting it.

Well, I don’t believe the market thinks it will only prove to be €750 billion Euros and the market certainly seems to think there will be a deal reached (remember, there are a couple countries not keen to this, and it only takes one to kill it). We don’t see fiscal and monetary manipulations generating real, organic, healthy productive solutions in Europe any more than we than do in the U.S. But what something like this means (or could mean) is at least some structural certainty that has been lacking for a long, long time.

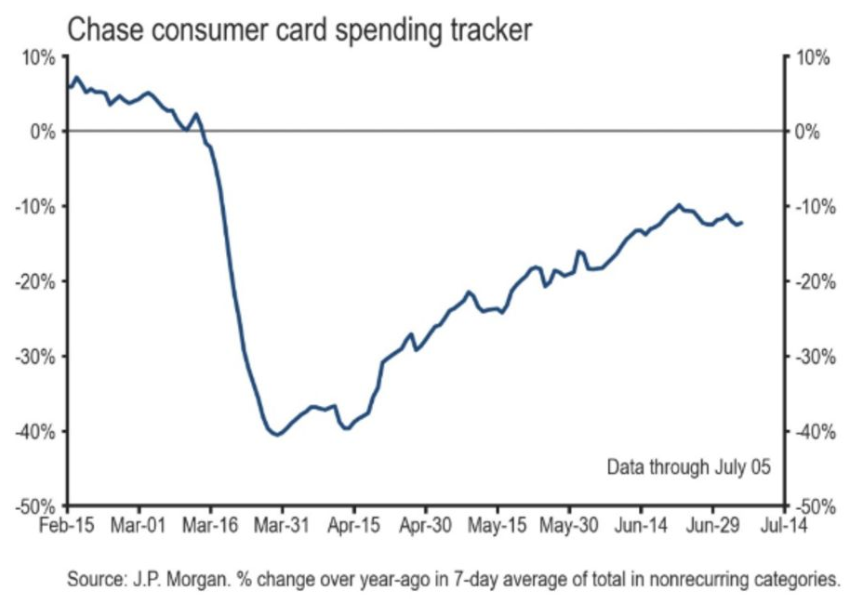

Economic Report Card

I have said it many times and will say it again. On the margins, consumer spending can always be affected by different things, and in a totally systemic way, it can be pulverized when you, ummmm, shut down the country. BUT, as a general rule, the basic desire of the American people to spend money is never, ever, ever going to be something I wonder about.

It is business confidence, business investment, capex, and so forth that I want to most see lead us in the next 2-3 quarters, and small business optimism is going to be a big, big part of this (for good or for bad, but recent survey data is really, really encouraging).

* Strategas Research, Daily Macro Brief, July 15, 2020

And beyond the small business optimism we saw this week, Industrial Production increased +5.4% in June, well ahead of expectations, and yet it was certainly off of a very low baseline.

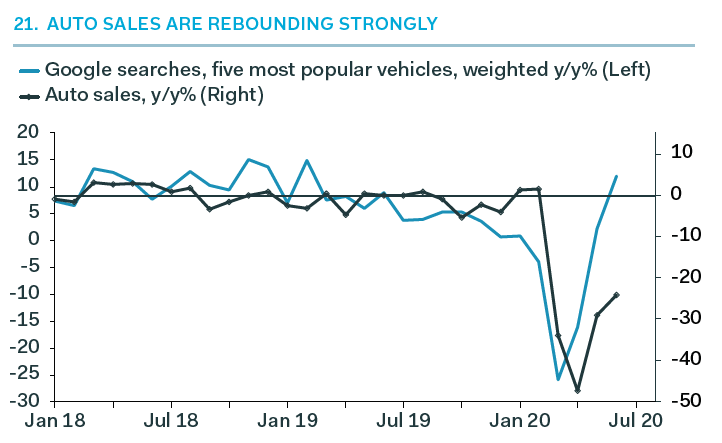

And finally, Auto sales are a positive indicator … and of course, rate sensitive.

* Pantheon Macroeconomic, U.S. Economic Chartbook, July 2020, p. 5

Politics & Money: Beltway Bulls and Bears

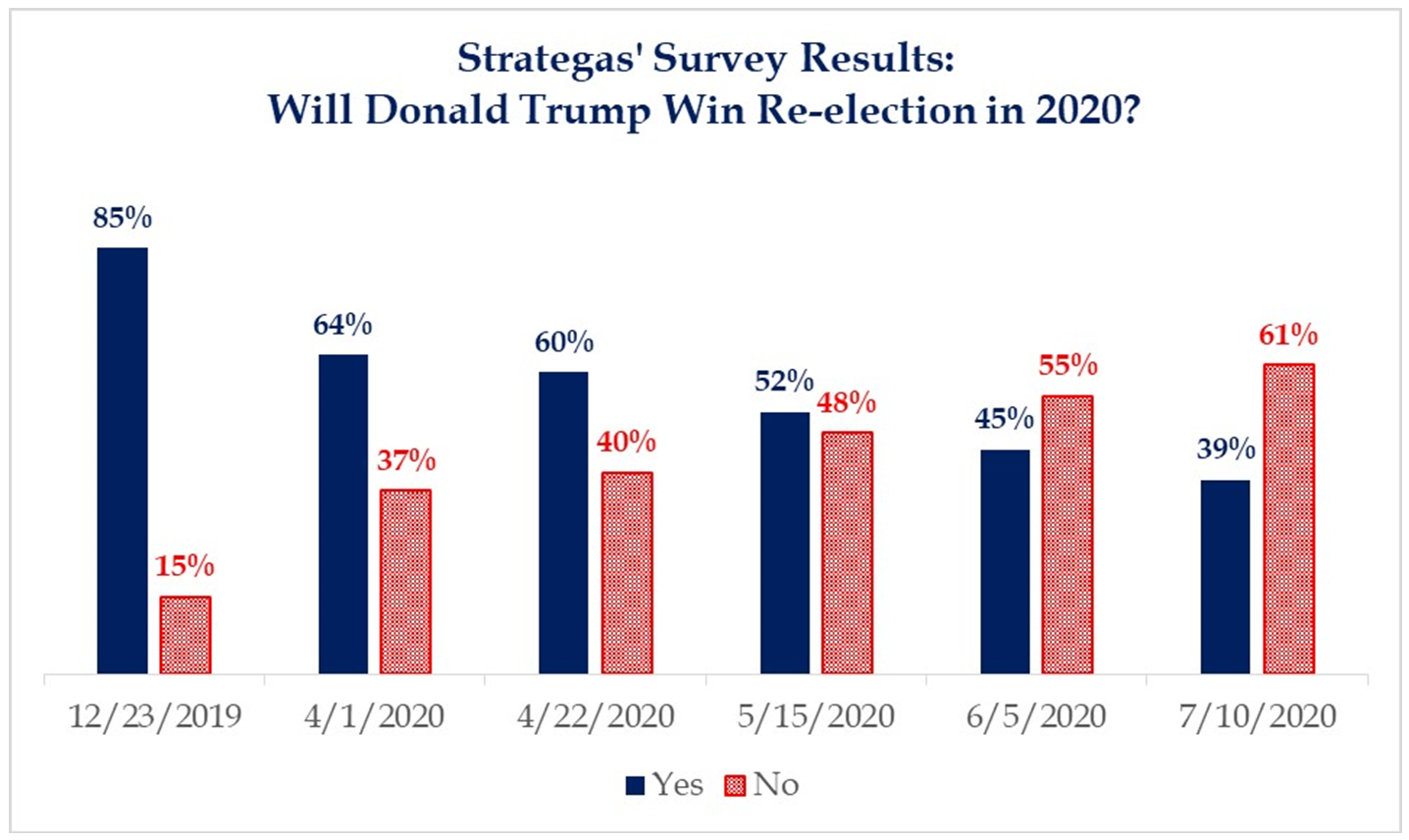

- I read a survey this week of 900 pretty significant institutional investors, wherein 61% believed Joe Biden would win the Presidency and 39% still believed President Trump would be re-elected. However, in that same survey, 56% believed the Republicans would keep the Senate. That suggests to me that, maybe, just maybe, some version of Biden winning is priced in to the markets, but the idea of the GOP losing the Senate majority is not (that is most directly significant to markets in what may come of tax legislation). Markets do not need to discount a higher corporate tax rate if they do not believe it will happen, and a Biden win/GOP Senate is not going to push the corporate tax rate higher.

- One of the most interesting things about this survey is how much and how quickly investor sentiment changed (in forecast, not wish) – from 85% to 39% in about half a year.

* Strategas Research, Daily Macro Brief, July 13, 2020

Chart of the Week

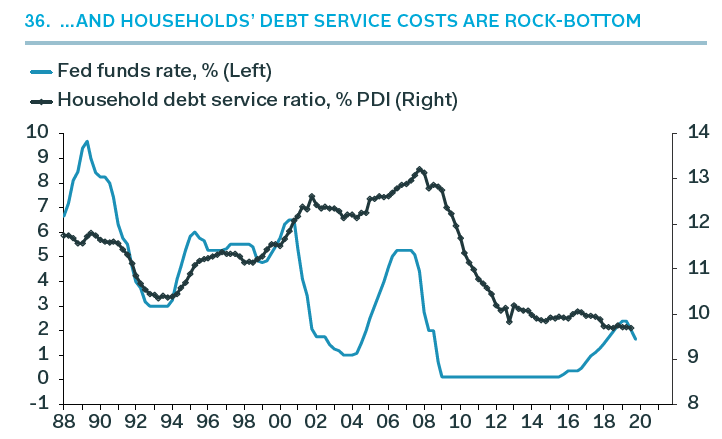

How are new homes being bought and auto sales surging and consumer spending picking up, even with modified quasi lockdowns, and even with a vicious recession? Because once you exclude the tragic amount of unemployed people, primarily in lower income levels, you have the still employed 85-90%, that all of a sudden have the lowest cost of debt and absolute debt service cost in history (thanks to Fed) … What are rate sensitive purchases (it’s not TV’s, vacations, or restaurants)? Houses, and cars.

* Pantheon Macroeconomic, U.S. Economic Chartbook, July 2020, p. 11

Quote of the Week

“Predictions are difficult, especially about the future.”

~ Yogi Berra

* * *

I wish you all a wonderful weekend, filled with jogging, sprinting, sitting, eating, and whatever else you choose. Isn’t freedom wonderful? Reach out any time – we are absolutely here to help each step of the way through these crazy times in which we are living.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet