Dear Valued Clients and Friends,

I have written about a lot of different topics over the years in the Dividend Cafe. For many weeks, I had the topic planned out well in advance, and in many other weeks, I pivoted plans based on something that transpired in that particular week. A lot of the time, I start typing on a Friday morning and let it go where it goes without a lot of planned topical inspiration ahead of time. I have my favorites over the years (and my least favorites), and I suspect some readers have their preferences about style, but I also feel it best for the Dividend Cafe to stay flexible – to do evergreen topics, to cover economic theory, to cover weekly market events when warranted, or even to bounce around covering a lot of different things. I have learned the wisdom of Robert Burns’ claim that “the best plans are laid to waste” when it comes to how I plan the Dividend Cafe.

I have no interest in writing every single week about the valuations of Mag7, the over-concentration of 5-10 companies in the S&P 500, questions about AI capex, the uncertainties and complexities around tariffs, and the importance of tax reform in 2025. However, if someone asked me what the five biggest stories are right now in the market, I would say:

- Valuations of the Magnificent Seven,

- The over-concentration of 5-10 companies in the S&P 500,

- Questions about AI capex,

- Uncertainties and complexities around tariffs, and

- The importance of tax reform in 2025

And I am not sure I would have much in terms of a sixth or, seventh, or eighth story. Things will come up. The way 2025 earnings results materialize will be a story (second half of the year). Geopolitical issues float around but are reasonably unknowable. So the aforementioned “five things” are not likely to go away any time soon, and I suppose that includes here in the Dividend Cafe.

That said, one could argue that there is a reasonable case to be made for how none of those things matter, either. I am going to make that case this week, but with the important nuances and caveats, I feel are important in my worldview of investing. So buckle up, and let’s see if I can’t pull this off – a treatment on the “five things that matter” (for markets, in 2025, as of right now), and how they are also “five things that don’t matter” (for investors who are also human beings with goals and a life expectancy).

Let’s jump into the Dividend Cafe …

|

Subscribe on |

Valuations Matter!

First, the good news after what appears to be a roughly -3% drop in the S&P 500 in the month of February (this is before Friday’s market action) … What started as a 22.5x forward multiple for the market at the beginning of the month (on consensus expectations of $268 of earnings on the year) ended the month at only 21.9x … (sometimes I write to entertain an audience of one).

The argument that valuations matter is because valuations matter, by definition. They may not matter as a timing concern (in fact, the more forceful and honest way to say this is that valuation is a terrible timing tool), but valuations matter as a basic mathematical reality of long-term returns. And because markets are mean-reverting forces, a “reversion” to historical valuation ranges will either mute returns (if positive earnings growth and multiple contraction are happening in mathematical proportion) or very often contract returns (where the math of multiple contraction exceeds potential earnings growth). Obviously, this is standard, normal, reasonably benign stuff – it has nothing to do with the actually bad stuff when earnings themselves contract and multiples contract. That is generally called a recession. I am not talking about anything like that right now. I am referring to an environment where earnings are growing, and stock prices are not, because the stock price is blending the math of earnings going up and a multiple going down. We call that a range-bound, sideways market and history is full of them. I believe we will be talking in a few years about how 2022-2029 (I am making up that end year because I haven’t the foggiest idea when it ends) was just such a period for just such a reason.

In a moment we are going to be talking about top-heavy concentration in the market index, and that is going to be pertinent to the valuation discussion (they are adjacent issues), because we do essentially have a valuation excess in the market because of and mostly isolated to the top-heavy tech parts of the market. But regardless, valuations matter to investors in the same way how your organs are doing matters to your bodily health. It is a matter of basic vocabulary. Excess valuations can be subject to sudden and violent corrections, but that does not happen all the time. It happened to technology in the year 2000, a year that will live in infamy (but hey, we survived that Y2K thing … [wink]). It happened to the housing market in 2008. It happened to “work from home” and plant-based meat garbage stocks in 2022. However, excess valuations can also be corrected slowly over time (hence the sideways market dynamics). History has several precedents here, but the important thing is that 100% of the time throughout history, that which cannot continue does not.

It is a fair question to ask why 22x earnings is expensive (or in the case of some of the truly expensive parts of the market, 138x, or 32x, or 41x, 34x, 38x, etc.). I like to put it this way: Would you buy a company if you got your money back if one hundred percent of the profits came to you for 22 years, and then you were back to even? Now, this is simply not an accurate assessment of these companies because when earnings are growing, not static, that time period is accelerated. But if one buys the CURRENT earnings stream, they will wait 22 years to get their money back. The market has an average multiple of a little over 16x earnings throughout the last 35 years (though that has moved up and down a lot), and earnings in the S&P have grown about 7% on average for a very long time. So the math becomes less than 16 years, but the basic corporate finance idea is impenetrable: All you are buying when you buy a public stock is a claim on earnings, and the multiple reflects some hope about the growth of earnings going forward (which is subject to risk), and a time value. Period. That’s the deal. When we get into a world of mass valuations beyond the realm of normalcy, it is not like some rich, smart investor is saying, “I would like to wait 138 years to get my money back on Tesla.” That becomes either (a) A really, really bold expression of optimism about accelerated earnings growth OR (b) A really, really bold speculation on how other people will speculate. That first option is what growth investing is supposed to be about. The second option is what we call “greater fool theory.”

In both cases, positive returns are possible. In both cases, a trip to the investor graveyard is possible and becoming a story in a future David Bahnsen Dividend Cafe is possible.

Valuations Don’t Matter!

The easiest way to set the stage for why valuations do not matter is to focus on dividend growth investors at The Bahnsen Group. Lots of readers do not fit into that category, so bear with me, but one easy way to be somewhat outside the impact zone of excess valuations is to wait for it, not be invested in excess valuations. Various portfolio strategies running at 16 or 17x may be in a very different position than those running at 22x, let alone 30x or more. Various portfolio strategies running at a 0.59 beta or 0.71 beta may be in a different position than ones running at a 1.0 beta (S&P), let alone a beta well above that of the market itself.

But I kind of hate those metrics. I don’t think a lower volatility, or a lower market sensitivity, or a lower valuation multiple, or intrinsically indicative of anything – they become noteworthy when looking backwards, after market contractions. They are not predictive, and in fact, there are many times when one would want to say, “Thank God I had a higher beta than the market because market sensitivity was a positive factor last year.” I don’t hold out the lower beta or the more reasonable valuations of our dividend growth strategy as a predictive or timing measure, but rather a philosophical difference. We believe quality matters, that the ability of companies to sustainably grow their dividends matters, and a lower beta and lower volatility and more reasonable valuation that follows is, well, something that follows, not something that creates. In other words, our companies have better quality metrics because they are good investments; they are not good investments because they have better quality metrics.

But let’s say someone owns the S&P 500 index weighted by market cap, as almost all index investors do (our clients do not). Does valuation in 2025 matter to them? It is entirely possible that the index will end the year still trading at 22x earnings and succeeding in generating 13% earnings growth this year. The return may be muted (that much is baked in already), but it is hardly apocalyptic! It is in the realm of possibility that the market ends the year at 25x (don’t hold your breath, but the late 1990s stretched the timeline of these things once). Because valuations are not a timing factor, the current excess may not be a factor in 2025.

And because we want to actively buy companies at reasonable prices, we believe our own orientation has less exposure to this overall consideration (which is not to say no exposure; even companies whose names do not rhyme with Shevidia are trading richer than their own historical valuation these days).

If someone were asking me what I do or believe about the overall valuation story, it can be summarized as thus: I care not a whit about not participating in certain excess moves forward of companies outside our philosophical orientation, and identify valuation in the dividend yield, the Free Cash Flow Yield, and the growth of the Free Cash Flow and actual dividend payouts, themselves – not the stock prices. And once we prudently operate in that mentality, we have a pretty iron dome around us.

Concentration Matters!

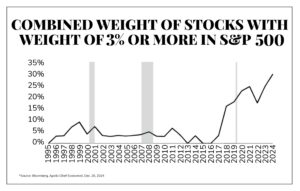

This section can be shorter than the prior section because, as I mentioned, a lot of it is adjacent to the valuation discussion. The concentration issues in the market are, in a lot of ways, the source of the valuation excess discussed above. I have been excessive in my coverage of this topic for some time, but for much of my young adult life, there were no companies in the S&P 500 that were even 3% of the market, and the total amount of such companies was well south of 10% of the market. That number is now more than 30%.

So while the relative under-performance of the Mag-7 to the market itself in the first two months of 2025 has brought this number down a teeny-tiny bit, the S&P 500 basically entered this year with ten companies being something in the range of 40% of the market, and 490 companies being 60% … This concentration is fine if those few companies keep doing well, but it is just a very different phenomena (for risk and reward) than the diversification benefit people believe they are buying when they buy a basket of 500 companies. And when the 5-10 companies that make up a massive share of the market are the very ones that hold all (or at least most of ) the market’s excess valuation, it compounds the risk and vulnerability.

Concentration Doesn’t Matter!

So I will start by saying that, again, it is easy for me to say why it doesn’t matter to us. We don’t own the cap-weighted index, and our portfolio has no top-heavy concentration issues. We have companies that are 4% of our portfolio and companies that are 1.5% of our portfolio, and various weightings in between, but we do not have companies that are 6% while others are 0.01%. Each company has attribution to the result, positive and negative, and the diversification reality is no different in concentration, weighting, and attribution than it has ever been. The concentration drift in the S&P is massive and unprecedented; we have had no such drift.

But again, let’s assume you are not a client of ours. Does this matter to you in 2025 if you own a cap-weighted index? Not if the top-heavy stuff carries the market again like it did in 2023 and to a lesser degree in 2024. And not if your long-term focus allows you to tune out what could be a mean-reverting year, and you believe future years will reverse such a correction and mean reversion. In other words, one may believe 5-10 companies will see their stock prices outperform all else in perpetuity, even if there are reversals of this trend in certain years. Several things could happen that mitigate concentration risk for index investors.

The concentration dynamic as market risk is not a statement about 2025, and to be very clear – it is not even a prediction about the fate of those five companies’ stock prices themselves (no matter how much some want to fight about it). Rather, it is an expression of a changed risk-reward dynamic versus that which many investors thought they had bought.

AI Capex Matters!

A looming risk to markets that I wrote about a month ago after the initial DeepSeek reports was that we simply did not know the entire story of where all this capital expenditure around artificial intelligence would end up. A good portion of the stock market has become dependent on hyperscalers still spending ungodly amounts of money to prep for AI use, and a good portion of the market has, therefore, become dependent on those hyperscalers finding ways to monetize that investment. Adjacent to that story are data centers being built for such, power companies providing the power for it all, and, of course, related economic activity around all of this. A chain reaction takes place if this capex fails to materialize, slows, moderates, or especially if it ends up lacking economic rationale.

AI Capex Doesn’t Matter!

There is no reason not to have some exposure to some parts of this potential thesis, and covered in the aforementioned adjacent category of it all is a truly unavoidable exposure for all investors. Real estate, infrastructure, utilities, technology, and more – there is exposure. But I happen to believe it is not if but when the story begins to change, and the reason it does not matter is because change is good – evolution of how this plays out – greater information and knowledge that impacts positioning enables a greater rationality in how resources are allocated. That the first stab of how people think AI will play out will prove to be wrong has massive precedence in history (see: MySpace). And the fact that Apple’s phone browser failed seems to have been one of the most profitable things for a company in history. In other words, the evolution is not about failure but rotation. Prudent investors will not be over-exposed to that which plays out differently than expected, and nimble investors will rotate accordingly, as will markets at large.

Tariffs Matter!

The mere existence of tariff discussions is causing a lot of uncertainty in markets. More or less, no new tariffs have been implemented, but the constant back and forth, up and down, and looming possibilities represent a risk premium that stands in the way of full economic output and confidence and renders clarity in economic calculation impossible.

I have written about this ad nauseum, but I haven’t tweeted as nauseum about it! The tweets from the administration are all over the map, and whether or not we end up with an administration that believes tariffs are a good idea to implement, we absolutely have a President who loves to talk about tariffs, at the very least.

Should tariffs end up transcending negotiation and actually be implemented, they represent a cost paid by American importers and consumers. They will be a drag on corporate profits and a drag on economic activity. Retaliatory tariffs will be inevitable, and the potential of a trade war could lead to something as severe as a global recession.

Or, not.

There could be nothing more than sound and fury signifying nothing. Tariffs matter, at the very least, because of the unpredictability of it all, and potentially a lot more.

Tariffs Don’t Matter!

They don’t matter in the end if they don’t happen. Or if they happen and are quickly rescinded. And between those two outcomes, you cover a lot of the total percentage odds of possibilities!

Tax Cuts Matter!

This one shouldn’t be difficult. Less taxes paid by businesses means more after-tax profits for businesses because of the way the English language works, and more after-tax profits drive stock prices (and for the companies we like, more dividends back to shareholders). Less taxes paid by individuals means more money available for savings, and more money in savings means more money for investment, and more money for investment drives productivity and growth. I know many want to focus on the individual demand benefits of lower taxes – that a given family may have more money for consumption, and that drives a certain activity in the economy, which stimulates economic growth. I am quite confident that it is true that households with a lower tax burden benefit from a higher cushion towards more lavish spending, and I am all for it. But that is not the aggregate economic data point I care about for our purposes here – when it comes to sustainable economic growth and investor outcomes. Tax cuts matter for Mrs. Smith when she can buy more toys for her kids. Tax cuts matter for all of the Smiths, Jones, and Johnsons in the country when there is a greater allocation of capital and a more productive investment base in the economy.

In the particulars of 2025, tax cuts matter because there is a looming risk (i.e., a violent tax increase if the 2017 Trump tax cuts sunset) combined with a looming opportunity (i.e., additional tax reform on top of extending 2017’s tax cuts). In 2025, economic activity will be impacted by expectations of where this is all going, volatility will be enhanced (or subdued) by the way we get there, and some end result is coming that will have an actual economic impact. So, there is a lot on the line regarding how this issue affects the ebbs and flows of 2025 economic activity and market results, and potentially, it will have a lot of impact beyond 2025. If, hypothetically, a 2025 tax bill ushered in immediate business expensing or at least some bonus depreciation, it could create business activity that promotes more growth in the years to come. If, hypothetically, a 2025 budget bill cuts taxes but doesn’t address spending, it could drive deficits higher in the years to come.

Bottom line – there is noise, and there is substance coming from what happens with the 2025 tax policy, and there is potential for its impact to go well beyond 2025.

Tax Cuts Don’t Matter!

There is a sense where a supply-sider like me (a zealous supply-sider who will never get over the fact that the supply-side economic philosophy has been successfully branded as a mere “tax cutting” group, as opposed to a holistic worldview rooted to the creational reality that God made mankind to produce, and that human nature and corresponding incentives matter) should never write a paragraph that starts with the heading “Tax Cuts Don’t Matter.” They do. But what I can say here is this: As it pertains to investors, if one believes some tax bill is coming (I do), and one believes that one way or the other, the 2017 tax cuts are getting extended (I do, and so does pretty much everyone else), it can certainly be said that long-term investors can ignore the noise, impact, and volatility along the way. And to be clear, even to the extent tax cuts matter for 2025 (see the paragraph right above this one), what exactly is an investor supposed to do about it? Buy when Speaker Johnson gets the votes, sell when he loses them, buy back when Trump tweets that they are voting again, sell again when Politico says Massie is a no-vote, buy back when CNBC reports that Hassett is meeting with lawmakers on the hill for a new deal, and blah blah blah blah blah.

Do you want me to replay for you the up and down drama of the 2017 tax bill, where it started (does anyone remember the brilliant “Border Adjustment Tax” malarky?), where it died, where it came back, where it changed, where it changed again, where it died again, and where it finally ended? Because I can do so. What I know was that markets loved 2017 (the best risk-adjusted return for the market since 1995), and the economy loved the results of that tax bill.

(For what it is worth, The Bahnsen Group hosted Treasury Secretary Mnuchin and then Presidential advisor Ivanka Trump in our Newport Beach offices in 2017 as the tax bill was being negotiated; hearing two different versions presented by the Secretary showed me that one way or the other they were going to get it done, yet that even they didn’t know at that time how).

I believe a tax bill is coming, I believe a possibility still exists of a decently good one. I believe it could be done in the first half of the year in “one big, beautiful bill.” And I believe all of that could fall apart. The volatility along the way is not very important to a long-term investor like me, but it is real. In the end, I am optimistic that a good outcome will come. For now.

Conclusion

I have gone on long enough, so I need to hit submit. We have a few significant themes playing out in markets, and we have a lot of considerations to consider. But what we also have are our first principles, which transcend headlines and politics and are inherently unknowable. The more your portfolio is tethered to durable principles, the less you have to care about any of this. To that end, we work.

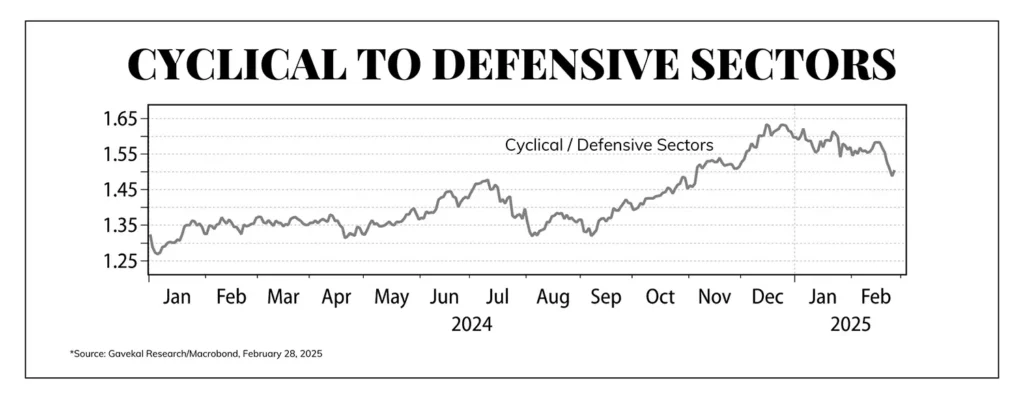

Chart of the Week

The defensives have begun to be the story of 2025, and the cyclicals have begun to fade relative to the defensives. This is not called a bear market – it is called a recession. This may prove to be a head fake, but it seems overdue to us.

Quote of the Week

“The investor of today does not profit from yesterday’s growth.”

~ Warren Buffett

* * *

The Monday Dividend Cafe looks like it is headed towards some robust coverage of a continuing resolution to keep government funded, the latest on a rare-earth minerals deal with Ukraine, where we stand on tariffs with Canada and Mexico, and so much more. 2025 will be through two months by the end of today. The month of March is coming, maybe the greatest month of the year.

Go Pacifica! Beat Fairmont … It’s a championship weekend for the Tritons!

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet