Dear Valued Clients and Friends,

I hope you will take the time to read this vitally important Dividend Cafe before your Independence Day weekend begins. I did my best to fill it with interesting stuff, but of course I think I always do that … =) In all seriousness, this is one that I am confident you will be glad you read. And then, the Fourth of July weekend begins!

I recently read Steve Schwarzman‘s autobiography, What It Takes, and it was really informative as to what the great leaders of our financial system did post-financial crisis (back in the ancient history of 2008-2010). In this case when I say ”great leaders,” I am not referring to the policy makers who were at the helm post-crisis, but rather the great investors and great business leaders who navigated through those stormy waters. The post-crisis era was more financially vulnerable by leaps and bounds than what we face now. That was a truly existential crisis, not a transitory one. And yet the quest for opportunity and vigorous maintenance of a long-term vision propelled great leaders and investors to extraordinary results. There is so much of being back in New York City that reminds me of the post-crisis feelings of early 2009. I missed some opportunities then, captured some, but was in much less of a position to understand and apply what the needs of the hour were. I am very hopeful to approach post-Covid markets differently, no matter how long this era may last.

It is a very different experience, and there are major categories which I have no desire to conflate (between now and then). But there is this commonality – both periods were trying, both were learning experiences, both will end (one already did), and both presented opportunities that those playing offense can capture. But like any sports team, in investing you never have the luxury of only playing offense … You have to be playing defense and offense at the same time, always. And what makes it even more challenging in the field of private wealth management where I reside, is that one person’s defense has to look categorically different than another’s – there is no “one size fits all.” Customized, tailored portfolio management is not for a 9-to-5er.

Well I am not a 9-to-5er, and those who excelled out of the financial crisis 10+ years ago weren’t either. This week we look at the first half of 2020, and plan and project for the second half of 2020, and beyond. Those looking for simplicity and ease will not get it. It will be complicated, and it will be tough. But those who care to will benefit from history. To that end we work.

In this week’s Dividend Cafe we will look at:

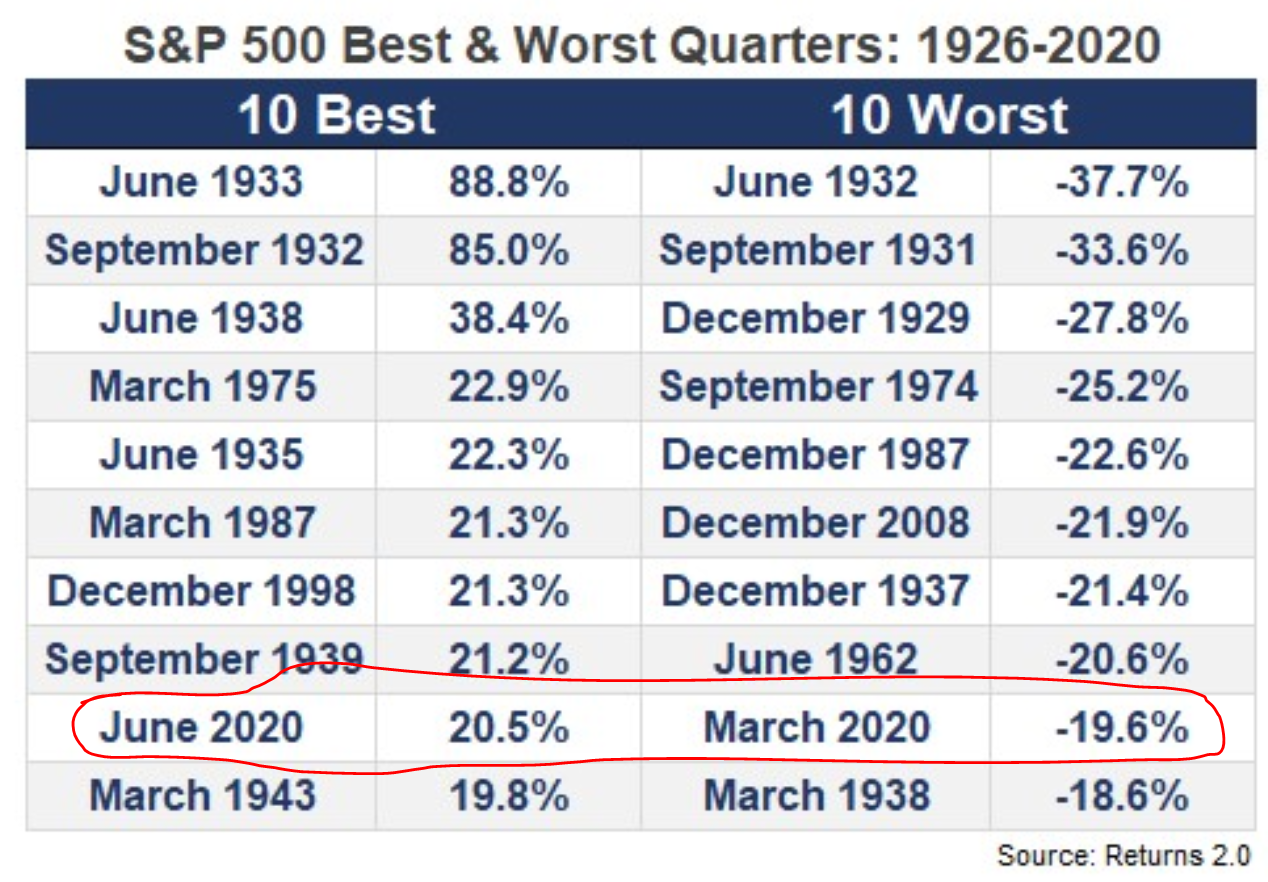

- The real lesson of 2020 so far, evidenced in Q1 being the 9th worst quarter in history, and Q2 being the 9th best quarter in history, and what behavioral lessons some investors may want to pick up from this.

- We do an extensive dive into what lies ahead for 2020, and our views on economic recovery, stimulus, a vaccine, volatility, and so much more.

- What the jobs report yesterday did to encourage us, and what is still lacking – and will be for quite some time

- Why Fed liquidity provisions may or may not matter to the real economy (i.e. jobs), but certainly matter to investors

- The under-appreciated tensions coming to the surface with China after Bejing’s passage of this Hong Kong security measure.

- What history says about an investor’s timeline and corresponding expectation

- How foreign investors apparently feel about American markets right now

- And all the economic data for the week to form that perfectly mixed picture of ambiguity. Retail. Consumption. Jobs. Capex. Copper. Checking account balances. We have it all.

- And in Politics & Money … the betting odds are blowing out for Joe Biden; what does that mean for investors, and what might the next three months of the stock market tell us about what to expect in November

- Finally, in the Chart of the Week, some calendar history to take us home

Let’s jump in to the Dividend Cafe!

The lesson of 2020

Q1 was the 9th worst quarter in market history. Q2 was the 9th best quarter in market history. No one has enjoyed what has happened in 2020 so far, but only one type of investor has been irreparably harmed by it: The investor was caught the 9th worst quarter in history but did not catch the 9th best quarter in market history. Market timing is a fool’s errand. If I say it too much, it’s because I need to say it a lot – morally, and professionally.

* A Wealth of Common Sense, Ben Carlson, July 2, 2020

Second Half Redux: Our Best Stab at a Forecast

Our economic projections continue to be: (1) A substantial recovery in Q3, the magnitude of which is to be determined; (2) A continued recovery in Q4, the pace of which will slow down from Q3; and (3) A 2021 recovery that will be more dependent on business than consumer engagement. The unprecedented monetary and fiscal stimulus already put into the equation, with more surely to come, makes it hard to take the under on these possibilities, and the uncertainty of the moment makes it hard to take the over.

We do believe a vaccine is coming, but we think what is more pertinent is (a) A growing acceptance of basic cases (and recoveries) in the economy, and (b) Continued improvement in treatments and therapeutics (which we believe is already happening relative to March/April).

It makes it very hard to see ongoing volatility that goes both up and down not being a reality for the foreseeable future. The stage is set for a vacillation between good news and bad news in most categories. Liquidity is everywhere (thanks to the Fed), and market sell-offs are buffered by that reality.

We believe another stimulus bill is coming, but with significant politicking and ugliness along the way. If the talk is that House Dems want $3 trillion and Senate Repubs want $1 trillion, I will get really bold and predict that they settle on $1.5-$2 trillion.

Ultimately, despite our focus on range-bound volatility for the foreseeable future, the combination of a very likely vaccine approval coming, in a period of extraordinary liquidity and monetary actions bidding up risk valuations, causes us to be biased towards a higher equity price level going into Q1 or Q2 2021.

Our focus simply cannot be only on the impact of current events on the next few weeks or even months. We simply must couple that focus with a really serious and sober perspective on long-term ramifications. We will write over and over again in the months ahead about longer-term realities out of this COVID era, while still providing you the information you want in current events.

On this hinges so much – jobs jobs jobs

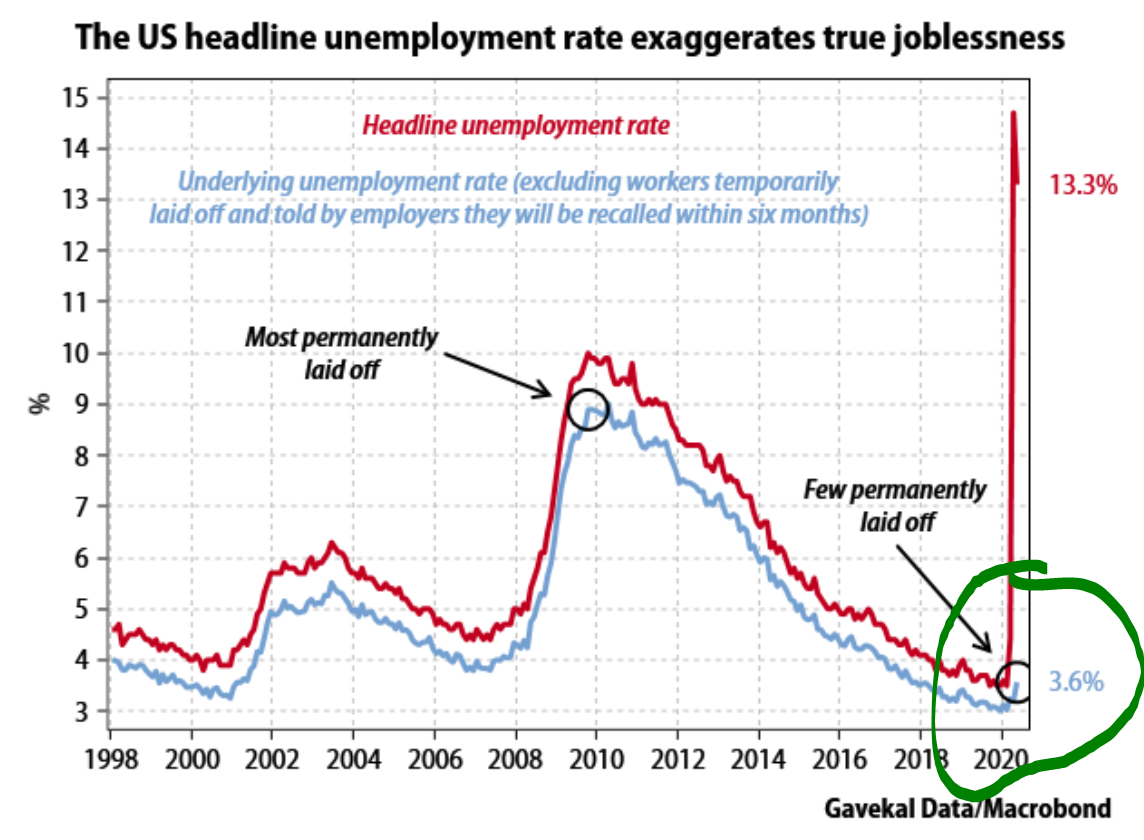

I believe that there has been ample sensationalism over the past few months, some of it forgivable, some of it not. The headline level of unemployment was (and is) horrific, and I do understand it receiving the press attention it received. And in that moment, I do understand how personally devastating it was to so many people, with hopefully some form of economic offset coming their way to better the situation.

That all said, the skyrocketing unemployment in the actual shutdown was always a “present” issue and never the “actual future economic issue.” The real data point to determine structural joblessness was, and is, permanent layoffs. That data point is hard to forecast and measure when at first all you have to go off of is employer’s intentions and expressions, and not necessarily what their capabilities will prove to be.

A “best case scenario” is by no means assured, but the hope that unemployment benefits closed the gap for household income during the last couple months of distress, and that a significant majority of these jobs is coming back, remains the “best case hope.”

Thursday morning’s job release data for June was significantly better than expected, saw a pick-up in permanent job losses, a huge drop in unemployment, 4.8 million new jobs (many re-hires), a massively better picture for hospitality and leisure, and a somewhat better picture for manufacturing. All in all, it was a very good report relative to where we very well could be at this point.

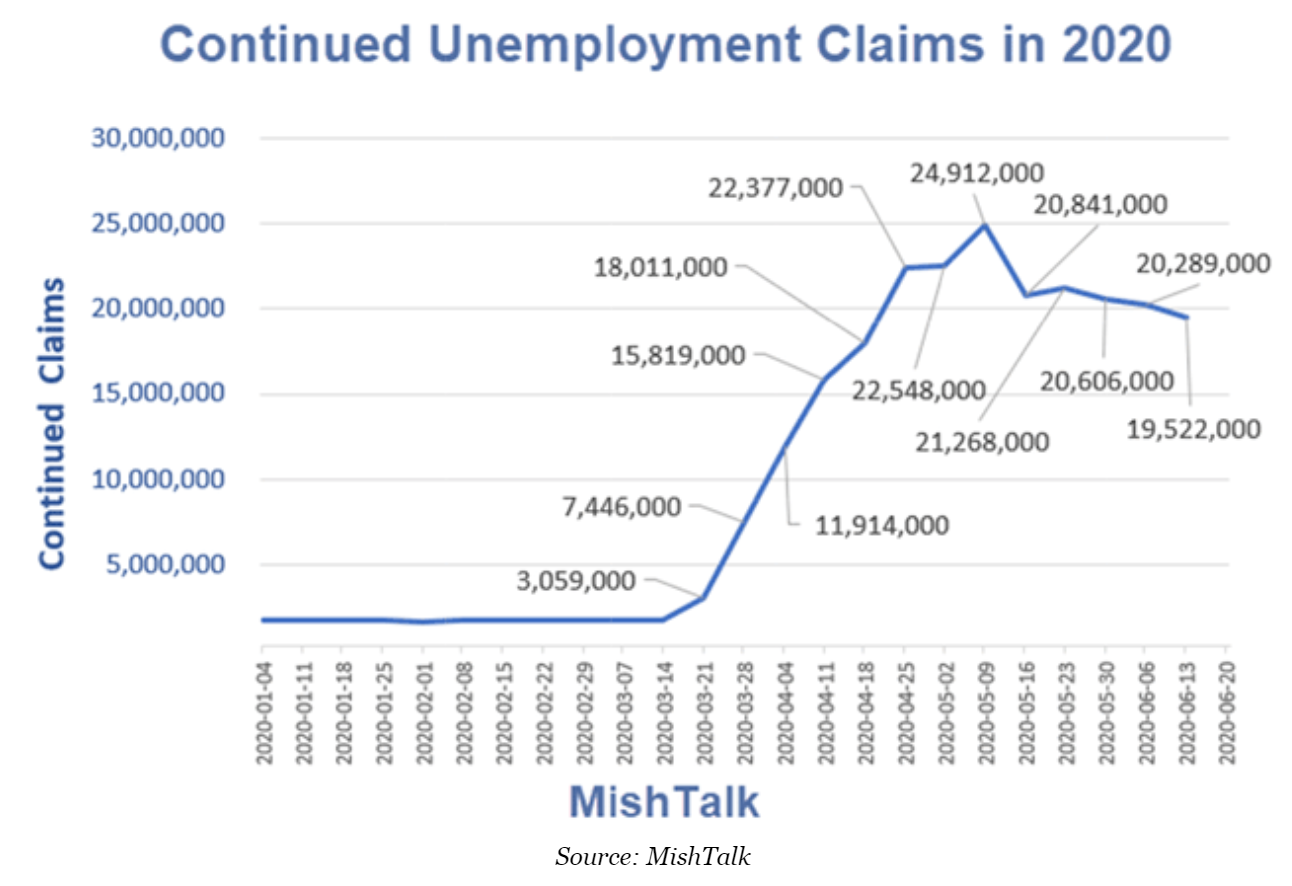

Closely connected to that is …

The continuous unemployment claims present both bulls and bears a talking point. We have seen 5.5 million people come off this number from the peak (bulls), but the 19.5 million figure remains way, way too high. As of this morning, it came in lower but still above

And that liquidity thesis?

The jobs picture matters a great deal to the real economy (more than anything else). But the liquidity picture matters a great deal to investors – and while earnings ultimately matter more than anything else – it is liquidity that most effects the pricing of risk assets in short term windows.

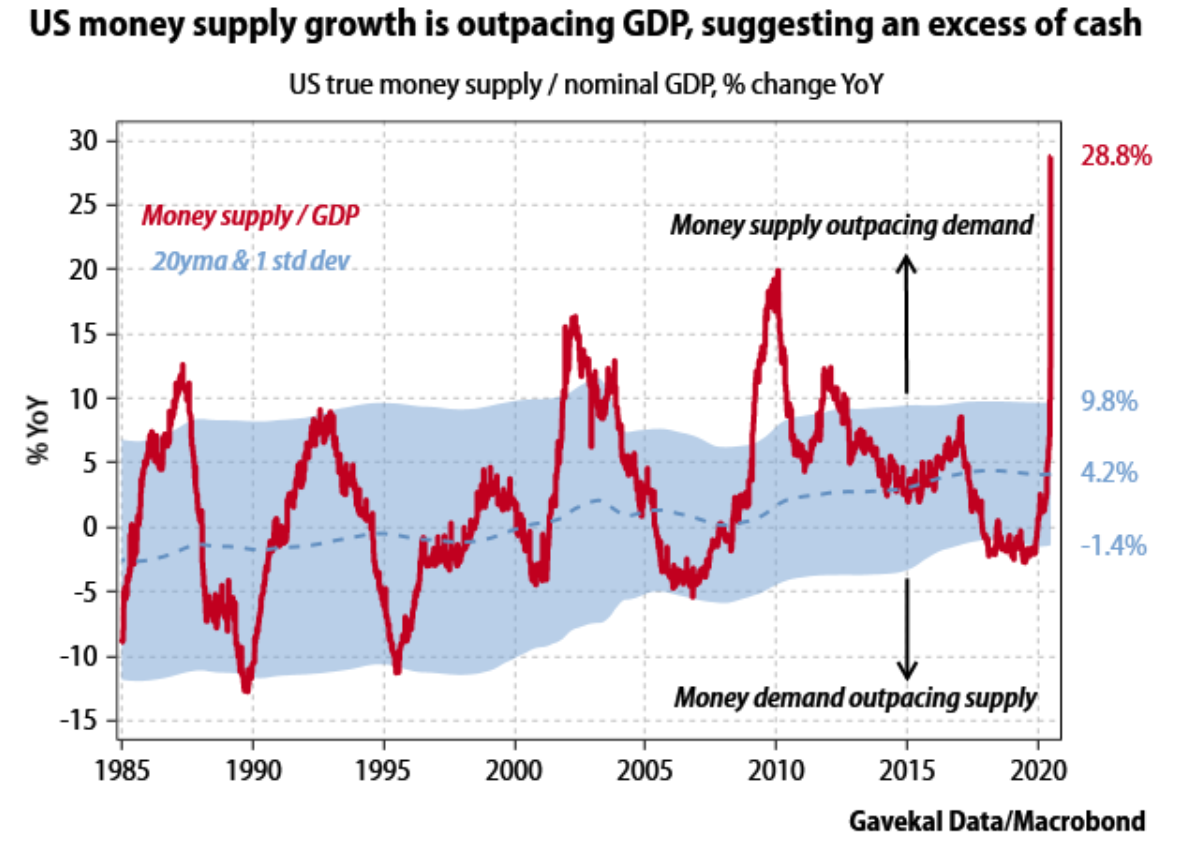

Here we have the tension picture perfectly encapsulated:

There is ample amount of cash out there – but inadequate demand on that cash due to the recession and poor economic conditions.

But then we see this:

And we know two things that matter to the point I am about to make:

(1) The Treasury running down this cash balance works its way into investment markets, supporting stock and bond markets.

(2) The Fed buying $120 billion of assets per month further pumps liquidity into the system, supporting stocks and bond markets.

It is hard to see how this reality is not already priced into bond markets, but perhaps spreads can come down further. I am finding that risk/reward trade-off less attractive. But despite all the reasons to fear risk assets in a time of uncertainty, the liquidity realities (money pumped into the system that does not find its way to the real economy, yet, but does find its way to risk assets) continue to be under-appreciated.

June’s popularity contest

It is no secret that we think much of the momentum and euphoria and popularity in the tech sector is headed towards some sort of very unfortunate ending (we just don’t know when). But I have to say, as a contrarian, this Health Care data point from June is both shocking, and exciting.

* Strategas Research, Technical Strategy Report, July 2, 2020, p. 14

The story the media forgot this week

On Monday the Hong Kong National Security Law was unanimously passed by the standing committee in Beijing, and it is effective immediately. It states that Beijing has ultimate responsibility for national security in Hong Kong, and generally entitles Beijing with various tools and weapons to oversee Hong Kong. The anti-western provocations of the bill are stunning, and reflect an acceptance in China that their status in the west is not as important to Xi as maintaining support domestically.

But I think (and am thankful to Corbu for their work here in persuading me) that much of Xi’s provocations with Hong Kong are driven by a desire to poke the United States and gauge how far he can take things. The U.S. response to Beijing’s newfound aggressiveness with Hong Kong will dictate where this goes as a market story in the weeks to come. I say “market” story, because that is genuinely up in the air right now.

What is not up in the air is that this is a “geopolitical” story, now, and will be one for some time. Sanctions are very likely coming, and even international financial actions are possible. The latter would be market-sensitive, and the former would depend on details. My general feeling is that it is a “when” and not “if” regarding U.S. escalation of the general tensions with China. The entire saga is being watched, closely.

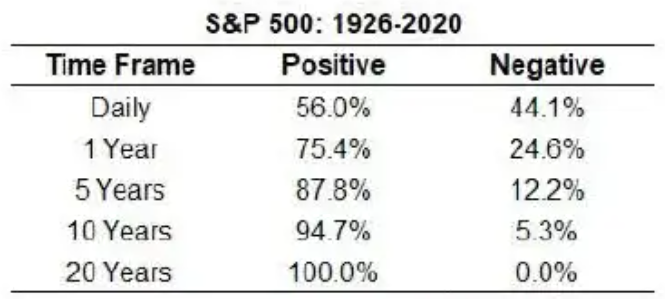

Perspective, History, Reminder

The truth is that this chart is best read with a focus on the right column, not the left. It is one thing to say, “only 56% of days is the market up, but in all long-term periods it has been.” But to remind ourselves that “44% of days the market is down” just sounds more potent. The ten-year periods below reflect the Great Depression, by the way. The basic point captured below is that the less one looks, the less it matters. 56% of days are positive, so 44% are not. But then it is a little higher positive and lower negative when you look at weeks, and higher/lower still with months, then quarters, etc. The continuum of time matters – just like the timeline of the investor matters in all practical sense.

* Wealth of Common Sense, Ben Carlson, June 27, 2020

What open markets do for you

Foreign investors (whose ownership represents 16% of U.S. public equity ownership, by the way) bought $187 billion of U.S. stock in Q1 this year, further reinforcing the TINA trade I speak about so often. The ferocious appetite foreign investors have for U.S. assets speaks to the U.S. dollar’s perceived relative value to competitive currencies, and the overall earnings power of the U.S., even in periods of distress, compared to other markets.

Economic check-in for the week

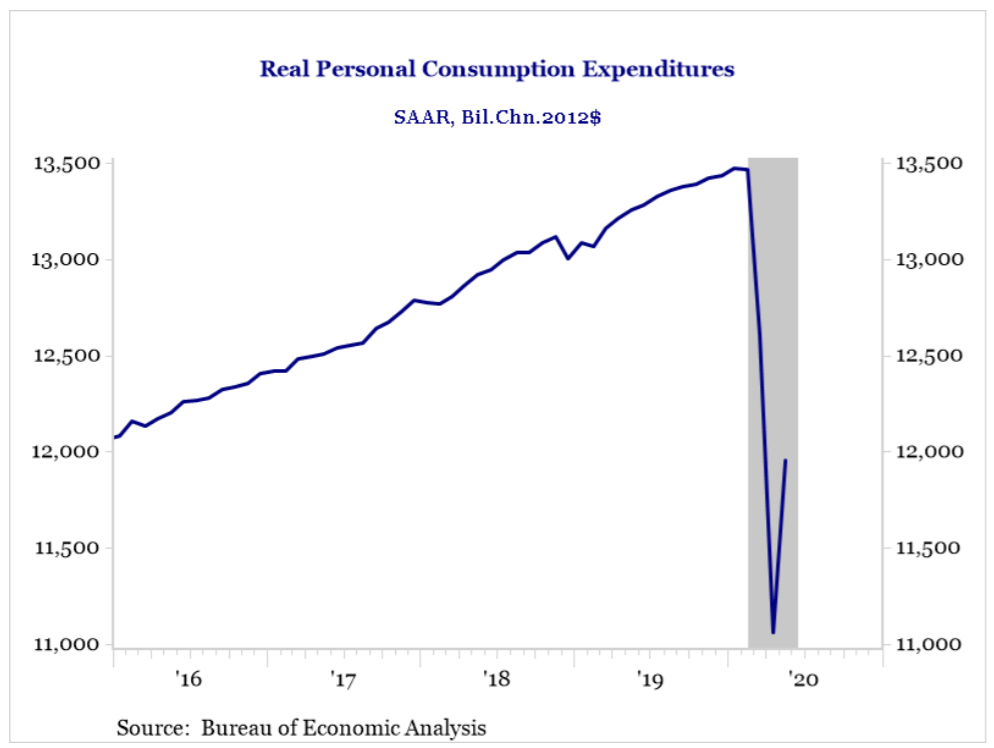

Yes, the consumer seems to be making their way back into the mix – slowly, but surely:

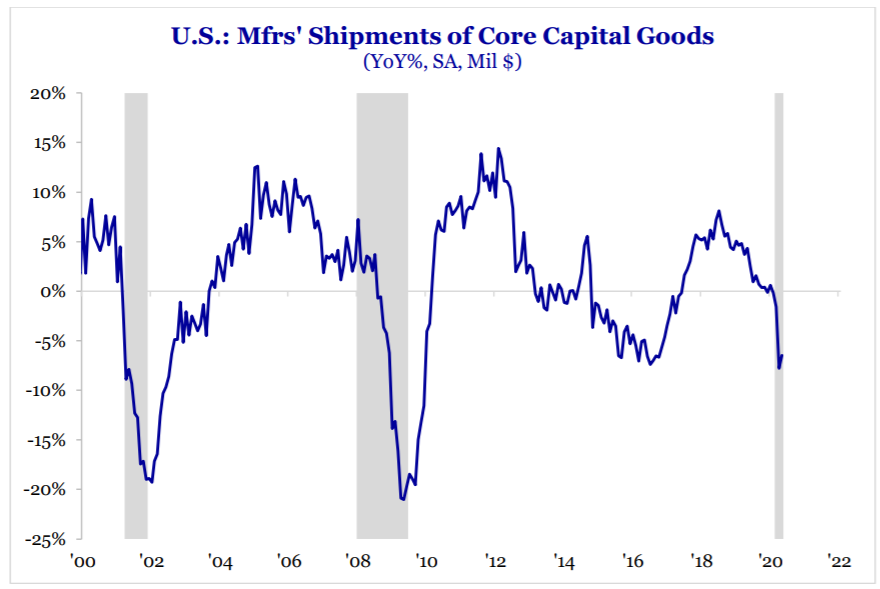

But as for our very high conviction belief that it is business investment which will most determine the fate of economic recovery in 2021 and beyond, we note the following in the manufacturing realm … Durable goods may well have bottomed (I am highly confident they did), but a rebound has a long, long way to go.

* Strategas Research, Weekend Reader, June 27, 2020, p. 3

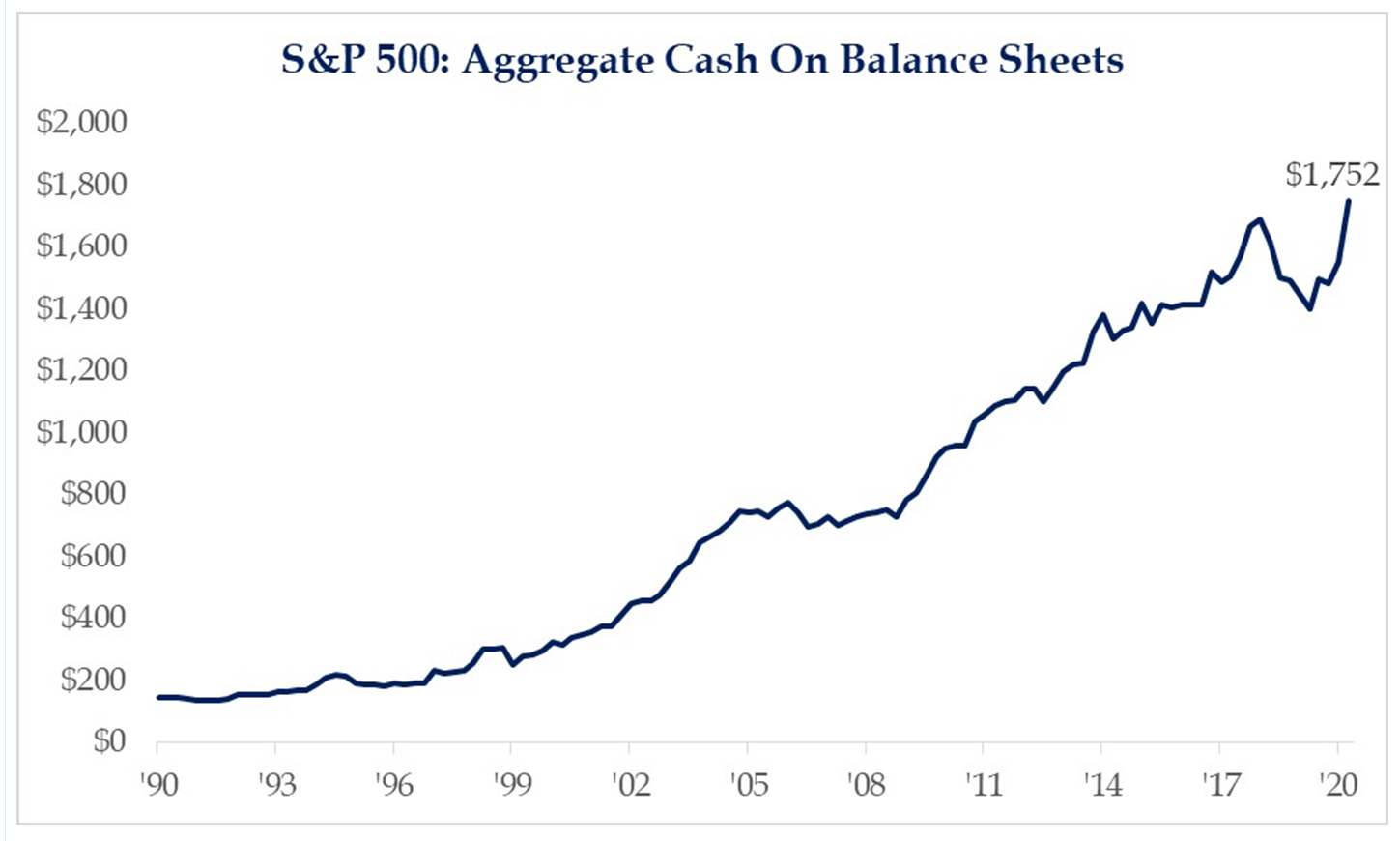

Now what would give me a little optimism that there could, maybe, might, should be the opportunity for a resurgence of capital investment when we come out of this recession?

*Strategas Research, Daily Macro Brief, June 29, 2020

I also think one has to wonder why commodity prices, particular industrial ones, have begun a reflation as they have if there is not industrial production resurgence on the horizon? Of course, it could simply be that supply has been choked off pushing prices higher … But all indicators are that it is the supply and demand side – and that points to reflationary conditions.

Politics & Money: Beltway Bulls and Bears

- I have written a lot over the years how high the correlation is between incumbent Presidents (and their parties, if after two terms) being re-elected and a strong stock market during their overall term in office. But sometimes there are nuances over a 4-year term that make simple and universal application tricky (i.e. a strong third year in the market but weak fourth year; or vice versa; etc.). A great example is Bill Clinton’s second term, where 1997, 98, 99 were among the strongest years in history, but the Nasdaq tanked in 2000, and of course Al Gore lost that election. Well, perhaps a simpler metric is available than even my own “full nuanced assessment” … I read a report this week that 87% of the time since 1928 just the three months prior to the November election have determined the winner (and 100% of the time since 1984). So maybe all of this is a waste of time, and we just watch August/September/October to see? History would indicate so …

- One of the reasons POTUS may really, really want a strong market in the 90 days before the election?

* Bloomberg Finance, Predict It, June 30, 2020

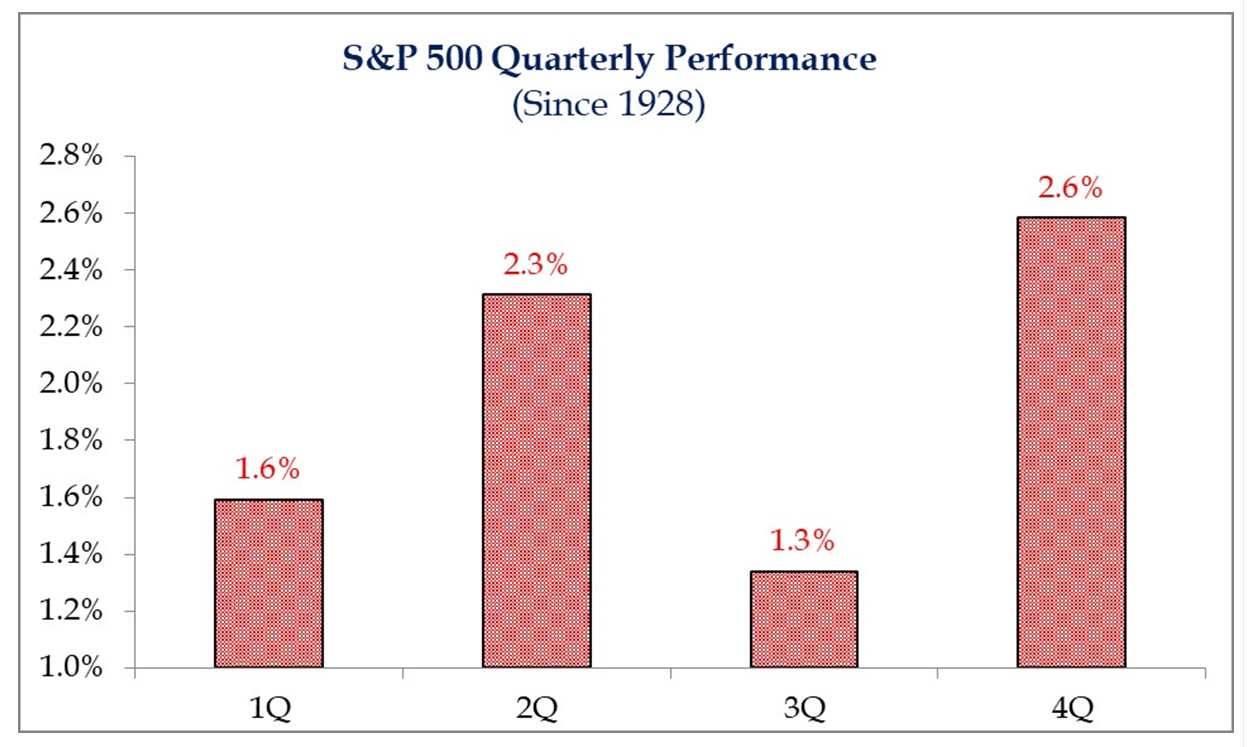

Chart of the Week

I picked an odd selection for this week’s Chart of the Week, because I really don’t feel that these kinds of things have any predictive value at all. And yet, I sure couldn’t think of any reason not to share it? I guess the reason not to share it would be if readers failed to understand that the way you get to an “average” over a 100-year period is with a heck of a lot of numbers higher than the average, and a heck of a lot lower, and the net result being the “average.” Will Q3’s return this year be lower than Q2? I would say that’s a pretty safe bet this year (Q2 was a big rebound quarter).

Will Q4’s be higher than Q3’s? Who knows. Election, COVID, economic recovery questions – a lot is unknown and uncertain. But years down the line, 2020’s quarterly breakdown will be just another of many inputs in how these are calculated. In the meantime, take it for what it’s worth …

* Strategas Research, Daily Macro Brief, July 1, 2020

Quote of the Week

“I am well aware of the toil and blood and treasure it will cost us to maintain this declaration, and support and defend these states. Yet through all the gloom I see the rays of ravishing light and glory. I can see that the end is worth all the means. This is our day of deliverance.”

~ John Adams

* * *

I love this country very much, and I love the principles on which it was founded. I am grateful for the freedom and opportunity this country has provided me, and grateful for the free enterprise system in which we work each and every day. Happy Birthday America, and may the second half of our 2020 be better than our first half, not so much for markets, but for our country at large. Happy Independence Day!

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet

The Bahnsen Group is a team of investment professionals registered with HighTower Securities, LLC, member FINRA, SIPC & HighTower Advisors, LLC a registered investment advisor with the SEC. All securities are offered through HighTower Securities, LLC and advisory services are offered through HighTower Advisors, LLC.

This is not an offer to buy or sell securities. No investment process is free of risk and there is no guarantee that the investment process described herein will be profitable. Investors may lose all of their investments. Past performance is not indicative of current or future performance and is not a guarantee.

This document was created for informational purposes only; the opinions expressed are solely those of the author, and do not represent those of HighTower Advisors, LLC or any of its affiliates.