Dear Valued Clients and Friends,

I really did mean to write this entire piece last week but simply ran out of time and space. I will give you a recap today of last week’s takeaways but then make sure this week’s wraps a bow around our updated point of view on inflation.

This is not merely a philosophical exercise. There is an abundance of empirical support provided for my position, and I think you will find a lot of the information about the present state of affairs surprising. You may draw a different conclusion on the matter than I do, but my conclusions on what this means for the decade ahead have profound implications for citizens and investors alike. Again, this can’t be armchair stuff for a real asset allocator; this is what we call fiduciary responsibility.

So grab a cup of coffee and get comfortable. This is one of those truly Dividend Cafe editions. Jump on in…

|

Subscribe on |

Week in Review

I will just quickly do a Reader’s Digest on last week’s Dividend Cafe, but if you haven’t read it yet at all, do so now.

(1) My views on inflation are the same now as they were before and during the inflation moment of the last 18 months. If I believed I had gotten the “big picture” wrong, I would admit so in a heartbeat. As my wife would attest, I am big on apologizing when wrong.

(2) That there has been massive price inflation over the last 18 months is undebatable and inarguable. What the causes (primary, secondary, tertiary) have been is not only debatable but not provable.

(3) Housing inflation is a bigger problem than all the other inflation combined, and housing inflation has been exacerbated by the artificially low cost of borrowing and unnecessarily low level of supply of new housing stock.

(4) The broad, non-housing manifestations of inflation we have seen are primarily a by-product of numerous challenges in the supply-side of the economy, not interest rates or helicopter money.

(5) The bond market continues to scream that short-term inflation is short-term, and long-term inflation is, well, non-existent.

(6) Why this matters is not political but rather economic – meaning, what the real economic narrative and takeaway need to be in the decade ahead.

Why I Care as an Economist

I live in constant fear that those of us on the “economic right” will do again what happened in the 1970s, which is conceding monetary economics to the academic left out of a slew of false prophecies. I think we have been living with an implied acceptance that we need the neo-Keynesians to do the heavy lifting, and right-wing economics will just mean asking for tax cuts. Supply-side, Austrian, pro-market sympathizers CAN and MUST make the case that excess government indebtedness suffocates growth. I believe economics is how human beings act in their God-given nature to allocate scarcity, create abundance, and meet human needs. I believe the suffocation of growth stunts this. I want to fight it, reverse it, explain it, and repair it. It’s my economic passion.

The Aggregate Demand curve may have shifted outward, but it was the failure of the Aggregate Supply curve to move upward that I believe warrants the real conversation here. This is an economic concept that is entirely comprehensible to people being sensible and objective about it.

The diminished [failed] return from monetary medicine and fiscal medicine must be better understood and communicated. When inflation inevitably subsides, the interventionists are going to claim victory despite the persistent existence of our real malady – stunted growth (i.e., Japanification).

But diagnosing the problem correctly and diagnosing the solution(s) correctly will provide the moral and intellectual upper hand needed in the years ahead.

Why I Care as an Investment Advisor

I suspect that if someone believed we were going to have 5-10% inflation for the foreseeable future, it would cause them to have a very particular outlook on their investment portfolio. And if one believed we were going to see Volcker-like monetary interventions to curb inflation, it would have a big impact on their risk exposures. If one believed that the government has the ability to just turn on the “economic heat” whenever it wanted, they may have a pretty sanguine view on growth (after all, if it were a government-led choice versus a challenge requiring incentive, risk, and effort, that would be pretty encouraging). From rate policy to growth expectations to valuations to the bond market, there is an abundance of implications that comes from this subject.

I meet financial advisors every single week – whether it be at professional events, over social media, or in the elevators of various buildings I am in. And almost every advisor I meet (besides ones with a TBG logo on their business card) believes in allocating client capital according to historic rates of return and in a passive, indexed approach. It provides more bandwidth in their practice for client service, financial planning, golf outings, and of course, family time. It saves the expense of resourcing a robust investment services department. Passivity does not require research, analysis, or trading, and I assure you – those things are expensive!

This is all good, and I am jealous. I am not criticizing my peers here (at least not with a rough edge); I am merely pointing something out. If indexing is based on a return environment where real GDP growth was +3.1% for sixty years, and GDP growth is not going to be close to that again, is it possible indexing is sub-optimal for the future?

I’ll ask it another way. If bond yields were 5% (on average) for sixty years, and they now are going to be lower than that, is it possible indexing is going to be sub-optimal for the future?

One’s view on all this does not merely impact their predictions of the price of a vacation; it impacts their capital markets assumptions, and it impacts the approach they take to capital allocation. My beliefs on this subject lead me to believe that passive index investing is ill-advised for the reality of the moment.

Inflation is High

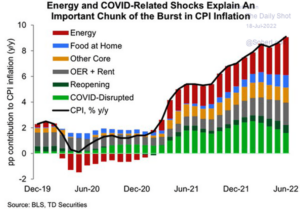

So we know the Consumer Price Index (CPI) released in July for the year-over-year Consumer Price Index (headline, inclusive of food and energy) through June 30 was +9.1%. The same report measuring core inflation (exclusive of food and energy) was up +5.9%. Energy was up, ummmm, +41.6% from June 2021 through June 2022, so that probably didn’t help. Food prices were up +10.4%.

Look at that data any way you want – it’s all there – and June 2022’s report will, I believe, represent the peak inflation report we see in this cycle.

Inflation is Going Lower

Goods inflation has peaked, with the rate of inflation growth down four months in a row. Used car prices, a hefty source of 2021 CPI’s increase, are growing at 7% (and declining); they had been up +40%.

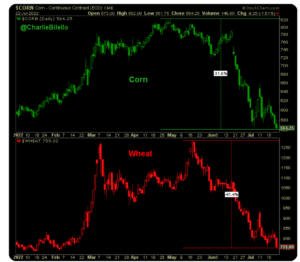

Agricultural commodity prices have collapsed.

*Bloomberg, Charlie Biello, July 24, 2022

At press time, Oil prices are at $100, down -20% from their June highs. These current oil prices are astronomically high, and, I believe, staying high, but they have dis-inflated from their peak, which puts downward pressure on headline inflation. If any commodity price could break through prior peak levels, though, it is crude oil. Geopolitical realities and challenges to the feasibility of supply solutions simply make this a volatile part of the inflation discussion (and also an idiosyncratic one).

The lagging effect of “Owners Equivalent Rent” will start to come down in the months ahead (the survey component in CPI that accounts for housing expense). COVID-related elements are already coming down. Energy remains the wildcard, but the sum of parts is easy to see as past peak levels.

The most recent Empire Manufacturing Survey saw a collapse in Future Prices Paid and a collapse in Future Prices Received.

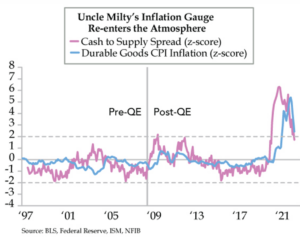

The Cash-to-Supply spread (deposits at commercial banks over business inventory) is the lowest it has been since the pandemic began, dropping significantly in the last few months.

An end to China’s lockdowns around COVID would put downward pressure on inflation. Will that ending come? Well, what do you think? Do you think they work? I don’t understand why they ever tried them, but I do believe they are not going to last much longer. The CCP may be evil, but it usually isn’t stupid – at least not for long.

Could a peace settlement between Russia and Ukraine come? I would be surprised. I would say there is less than a 20% chance of a satisfying ending to this and only a 40% chance of even an unsatisfying ending. But regardless of how it is handicapped, any such ending, should it overcome the odds to surface, would be a huge accelerant to disinflation.

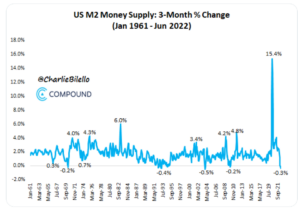

Even for pure monetarists who tend to not understand velocity, the M2 money supply reading that flew higher after COVID has now utterly collapsed and just experienced its biggest contraction since 2003!!!!

*Compound Capital Advisors, July 26, 2022

Inflation expectations in the TIPS market have fallen from 3% to 2.3% over the last three months. Remember, this is market actors voting with their real dollars through the real yields they will receive what they believe about inflation over the next decade. 2.3% is really quite close to the Fed’s own 2% policy target.

Bottom line: Across commodities, housing, potentially energy, food, general goods, etc., inflation rates have peaked, in some cases are coming down slowly, in other cases coming down rapidly, and speak to some cooling of the present narrative, for whatever that’s worth.

So does this mean deflation is here?

An inflation rate that goes from 9% to 6% is not deflation, but it is disinflation. I do believe disinflation will be the welcome narrative for a while, but I lack the arrogance to predict how quickly all of that will play out. It could be slow, it could be quick, but my point is – disinflation is not inflation, and that changes expectations for stock valuations, bond yields, and more.

But isn’t that a good thing?

Seeing the rate of increase of price growth contract (disinflation) is a good thing, and it is a crucial thing from the levels we presently see. But when we get on the other side of the supply constraints that caused this 2021-22 blip in inflation, what we face is not a good thing, and that is all I have ever, ever, ever been focused on. And it represents something more concerning to the cause of economic prosperity than this season of high inflation.

It is … low, slow, no growth. And that low, slow, no growth is a by-product of excess indebtedness and excess monetary interventions that are, and here’s the real punch in the face, the proposed solutions for low, slow, no growth.

Do you see my entire point? Our cycle of fiscal and monetary interventions to treat business cycle disruptions (which are normal and unavoidable) has created a phenomenon where, all at once, we end up with more business cycle disruptions and have a diminishing return on what we prescribe to treat the malady.

Tangled web we weave

I am not against the country having a central bank. I am against a hyper-interventionist one. I am against the mandates and machinations that the institution has taken on. I am against the idea of the Fed becoming a quasi-hedge fund (that can’t absorb losses) with infinite alphabet soup facilities out of every economic downturn. But no, I do not agree with many of my Austrian friends that a “lender of last resort” is an inherently statist concept. I agree with the great 19th-century journalist Walter Bagehot, on what a limited but legitimate role for the Fed ought to be:

“To avert panic, central banks should lend early and freely (without limit) to solvent firms, against good collateral, and at high rates.”

The “lender” of last resort has become the “spender” of last resort (h/t Lacy Hunt). They have expanded the concept of lender of last resort to mean things that defy the imagination. They have become responsible for an entire stewardship of the U.S. economy that requires a hubris unimaginable to classical economists. They are expected to see and know things that no one of any academic pedigree could really be expected to see and know. We now assume interventions from the Fed that are dangerous, disconnected from a real cost-benefit analysis, and that exacerbate booms and busts.

But more than anything else, they have become a facilitator of profligate spending that has made caused the pool to become filled up on one end while it is being drained on the other. In other words, as Congress spends and borrows, downward pressure is put on economic growth at the same time the central bank believes it is affecting policy that will drive economic growth. Rinse and repeat, as I like to say in this context.

Does the Fed cause inflation or deflation?

Yes.

Now, I actually believe the worst thing they do is cause distortion, and I favor an economy (and investing markets) as free of distortion as possible. But to the degree we are analyzing monetary consequence here, the hard truth is that the Fed doesn’t so much create one or the other as they create monetary instability, that is, both.

Monetary growth in a range of economic growth, population growth, and other rational and measurable constructs is not only harmless but necessary. It is outside the scope of this essay to consider what criteria should be used to calculate such (there are many competing ideas from Milton Friedman to John Taylor to Alan Meltzer to Scott Sumner), but what is very much at the heart of this essay is that totally discretionary policy completely divorced from rules and objective standards lead to instability.

And instability is bad for growth.

In the long run, we’re all … looking for growth

I appreciate the caginess of Keynes’ famous line that, in the long run, we’re all dead as much as the next guy, but it’s a stupid thing to say. In ten years, most of us won’t be dead. Or twenty. And I bet a lot of us reading this have 30 and 40 years left in us. And maybe Keynes didn’t care about this, but when I’m gone, and you’re gone, our kids and grandkids will still be here, too. Long-term growth matters for us, and it matters for the generations behind us. Period. This is an economic, theological, moral, and existential truism. And I can’t believe how little we care about it anymore.

The current moment

I believe as the economy sits in what has always been considered “technical recession,” we face the reality of an economy that is, by no rational person’s mind, “too hot” – yet in need of equilibrium in supply/demand. We need the growth of goods and services to absorb the liquidity in circulation and to optimize the aggregate supply curve upward appropriate to where the demand curve is.

Yet we face $30 trillion of national debt sure to go higher by somewhere around $1 trillion per year for as far as the eyes can see. Economic actors know this, and it carries with it two harsh realities:

(1) The money used to pay the servicing of this debt is literally, dollar for dollar, extracted from the private economy (i.e., sum aggregate of goods and services we just said constitutes the growth we need), and …

(2) This is known by economic actors who would otherwise be responsible for risk-taking and capital investment and face the painful dynamic of decision-making in an environment of heightened instability and downward pressure on growth.

A debt-deflation cycle is a scary thing to deal with, wherein a high level of debt causes people to pay down debt out of fear of lowering economic output, but in so doing, lowers output further (more money went to debt reduction than the production of new output), causing the denominator to shrink (output) more quickly than the numerator (debt). In that case, you worsen your debt-to-output ratio by reducing debt. It is the debt-deflation paradox that Irving Fisher wrote about almost a hundred years ago.

Japan has lived in it for thirty years. We have not. We have lived in a miniature version, I suppose, and we certainly went through it with the Great Recession. But we have maintained enough positive output that the price we have paid has been unimpressive but still positive growth for 15 years. It’s not good. But it’s not Japan, and it’s not the Great Depression.

My argument is that we can do better. Economic growth equals Population Growth combined with Productivity Growth. My argument is that our Productivity Growth is hampered by the dynamics I describe above.

Forget this month’s report. Let’s talk 50 years.

China’s population is presently 1.4 billion people, 17% of the world’s population. It has more than doubled since 1980, a statistic that is truly unfathomable to behold. And yet, in 2022, their population will be lower year-over-year for the first time since 1961 (yes, the 1961 of Mao’s Great Famine).

China averaged a fertility rate of 2.6 for many years yet is barely at 1.1 now (and has been below the replacement rate for nearly twenty years).

Japan’s fertility rate is 1.3. The United States is 1.6.

The low fertility rate of Japan is well-known, well-documented, and well-discussed, and the implications for its national productivity are not forward-looking – we have three decades of observation to say that it is an unmitigated disaster for growth.

The American decline in fertility is more recent (it began at the time of the financial crisis), and it does seem to be worsening. And it is my major concern because, well, I am an American.

But why am I focused on China’s fertility rate? Because their denominator is 1.4 billion people – ours is only 330 million. In 75 years, it is estimated that China’s population will be 587 million, less than half of what it is now.

America may or may not address its fertility issue. But for now, allow the gravity of a multi-decade decrease of 750 million people from one country to sink into your expectations of deflation. Decade after decade of that kind of population decline is extremely deflationary on a global scale. The last 30 years, we saw a high dispersion of fertility realities around the globe. But if China joins the west and Japan in not meeting its replacement rate (it already has), I just suggest to you that this is a more significant contributor to inflation/deflation expectations than anything we are presently discussing.

Conclusions

I do not want to leave you with platitudes about the state of economic growth. I want you to understand what I am saying as we navigate through this period.

(1) The monetary instability that Fed policy has created (really, that our political and societal demands of the Fed have created) is a contributor to downward pressure on growth.

(2) The excessive indebtedness we face as a nation (sovereign debt) puts downward pressure on economic growth as moneys are diverted in the future from productive use (the meeting of human needs through more goods and services) to less productive use (paying debt), and as economic actors have to price in this reality to their own calculations about future risk and investment.

(3) The problem I identify in #1 and #2 (downward pressure on growth) is so far treated with actions that exacerbate monetary instability (Fed interventions) and with actions that exacerbate excessive indebtedness (more spending). This negative feedback loop of self-reinforcing downward pressure on growth can only be countered by a commitment to a stable price level and an end to ditch-digging (that is, making the fiscal indebtedness worse).

(4) For investors have to understand that my proposed solutions above are NOT the most likely scenario. Therefore, they have to assume that they face more monetary policy creativity, more government excess, and more instability. This creates both a temptation to be drawn into bubbles and the risk of severe pain from bubble bursts.

(5) Economists predicting how it will play out are wrong, in the sense that it is guesswork, riddled with incomplete aggregates that serve as variables in our calculation, and highly susceptible to surprises and shocks along the way.

(6) Invest in productivity because it will carry a massive return premium for the rest of your life. It is not a shiny object, but it is needed in a way now that we have never seen before.

(7) Invest in stability, because instability is going to rule the roost, and therefore stability will also carry a massive return premium.

(8) When you re-read #6 and #7, understand the benefits of dividend growth over shiny objects and really any instrumentation that is subject to the policy regime of the Fed and the central planners. Nothing can be done infallibly, but as a general direction, emphasis, trend, and criteria favor productivity and stability in an economy desperate for growth that is treating its deficit with more instability.

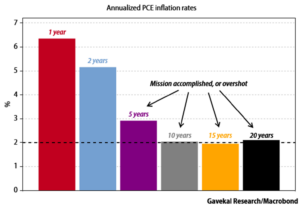

Chart of the Week

High inflation over the last two years has now caused the 10, 15, and 20-year inflation levels to, wait for it, be at 2% per year. You know, the Fed’s claim for their own target policy objective.

Quote of the Week

“There is nothing new in the world except the history you do not know.”

~ Harry Truman

* * *

I know you may feel that this Dividend Cafe went too long, and I know that combined with Part 1, it was really, really long. But I have tried my best to express these things today with a clarity that will enable you to think a little more holistically about the economic environment we are in. We have seen high inflation over the last 18 months. We are likely to see that begin to reverse now. And in all our assertions about what is wrong and right in the economy, we will likely continue to grant to two [sort of] distinct bodies (the Fed and the Congress) the presumed power and ability to fix it. What they will do with that is likely to make it worse. And that will cause investors and citizens alike to continue to come up short of the economic growth they need, all the while suffering through more instability.

And so, we will invest in productive stability where ever we can. To that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet