Dear Valued Clients and Friends,

A couple out-of-the-ordinary things are happening this week. No, I am not referring only to the “will he, won’t he” talk about the Biden campaign in the aftermath of last week’s debate, though perhaps that news event has you captivated. But over here in markets land, we have (a) The halfway point of 2024 upon us and (b) A holiday week where the Fourth of July lands on a Thursday, leaving markets open on Wednesday and Friday but not in between. We decided to take these two special events and blend them into an “early Fourth of July weekend Wednesday edition” Dividend Cafe focused on a mid-year assessment of markets and the economy.

Our annual tradition of a “Year Behind, Year Ahead” white paper was never meant to have its progress judged in July. “Year” means “year,” though sometimes forecasts play out sooner than expected, other times they play out the opposite of what is expected, and other times, still, it is worth just checking in on to see if there is anything to point out that might make one look smart, or anything to ignore that might make one look dumb … (I kid, of course). This mid-year assessment is an added feature to today’s halftime report.

And all of it is the perfect way to take in your extra long holiday weekend. I can think of nothing that better screams American independence than the Dividend Cafe, besides hot dogs, BBQs, beach parties, and fireworks. But besides those obvious aspects of American exceptionalism, I present to you that which is deeply entrenched into the tenets of free enterprise … jump on into the Dividend Cafe!

|

Subscribe on |

Market Recap

The numerical side is the easy part. The Dow was only up +4.7% in the first half of the year, and the Russell 2000 small cap index was only up +1%. Yet, the S&P 500 was up +15%, with the Nasdaq up a tad more than that. You can call it is a “risk-on” rally if you want, but it is hardly a monolithic one, with small cap basically flat, the Dow being in the middle of the road, international markets up high single digits, and big cap growth/tech pulling the S&P and Nasdaq up into the mid-teens or better.

If one is looking for red ink, the taxable and tax-free bond markets barely provided some, each coming in around -0.70% for the first half of the year (essentially 2-3 points of price depreciation being offset by 2-3 points of yield). Bond yields started the year in the high 3’s (10-year), got up to the high 4’s (4.7%), and settled June 30 in the 4.35% range (so in the middle of the starting point and the high point). It was enough of a yield move to move prices down and then halfway back up, but with a protective cash flow offsetting that price volatility.

Oil prices were up +16% year-to-date, with a +21% rally into April being followed by a -16% drop, then being followed by a +13% rally. Volatile? I suppose so, but not extraordinarily so. And not like natural gas, with its 50% drop and 100% rally all within the first six months of the year. As has been mentioned a lot in the Monday Dividend Cafe, midstream energy has been the big equity market winner in the sector, up +18% on the year and still offering superlative yield.

Technology was atop the leaderboard for S&P 500 sectors in the first half of 2024, with its cousin sector, Communication Services, closely behind. Only Real Estate was negative year-to-date.

The VIX basically didn’t move from the beginning of the year until the end of Q2 in terms of start and end points, but there was a bit of movement inside of each quarter. The bottom line, though, is that protection against market downside has remained extremely cheap, likely a by-product of (a) a benign earnings environment, and (b) expectations of eventual Fed easing. Some may say the first half of the year was volatile, and April did see some market downside. But a -5.5% peak-to-trough max drawdown doesn’t even register. And there have only been seven days all year where markets were even down -1% (child’s play). Only one day all year saw markets up even +2%. And candidly, fourteen days of +1% or better moves to the upside isn’t much, either (though it is double that of the down days to that magnitude). It just hasn’t been a high volatility year so far.

If the breadth of market returns had been wider and more areas of the market had participated more healthily, with less feeling of top-heaviness in the return attribution, it would most certainly feel like a far more robust market year-to-date. The thinness of where market superlatives have come from just makes it feel like a far more fragile market than the top-line numbers at first indicate.

Economy

Economic growth has been positive but muted. Job gains have been positive, but slowing. The consumer has been spending plenty but with increased delinquencies and credit card balances. M&A activity has picked up but remains below peaks of a few years back. Activity has been resilient to the impact of higher rates but with pockets of activity suffering immensely. Housing prices have not dropped, but housing sales have collapsed. Inflation has come way lower, but there are components staying stubbornly high. Jobs are high, but auto loan defaults are picking up. Wages are up, but savings have evaporated. Owning assets has been great. Owing money has been rough.

And if that doesn’t clear it all up, I recommend this or this. Perfect clarity, right?

Credit

Demand for corporate debt has been perfectly received by markets all year, with spreads on both high-yield and investment-grade corporate debt staying quite tight. In English, what I just said is – companies aren’t having to pay more interest to get people to buy their debt; they are perfectly happy buying it at low yields (relative to treasuries), I would expect this to hold for high-quality debt if economic conditions stay reasonably stable, but likely worsen for lower quality bonds. In other words, we expect divergence whereby investment grade will correlate highly with treasuries but high yield will correlate highly with equities.

Semester report card

So the full-year themes and perspectives of the 2024 Year Ahead paper are re-provided here, along with a point-by-point check-in on how they are doing:

(1) “Fed Particulars Will Be Over-Rated”

If the market started the year expecting SIX rate cuts, got ZERO thus far, and yet the market is up +15% year-to-date. I would say I am on track for an A+ on this one, along with AP and Honors and college credit boosts to the GPA.

(2) “Biggest Contest of 2024: Deglobalization vs. Productivity Boom”

I wouldn’t be able to “grade” this halfway through the year, but I can say that the underlying tension of deglobalization costs vs. productivity/capex upside remains alive and well. I have a feeling we end the year with a lot of this in limbo and no clarity around the tension, but that wouldn’t make the tension any less real. Manufacturing continues to be weak. Capex investment remains a question. And deglobalization costs remain elusive. The beat goes on.

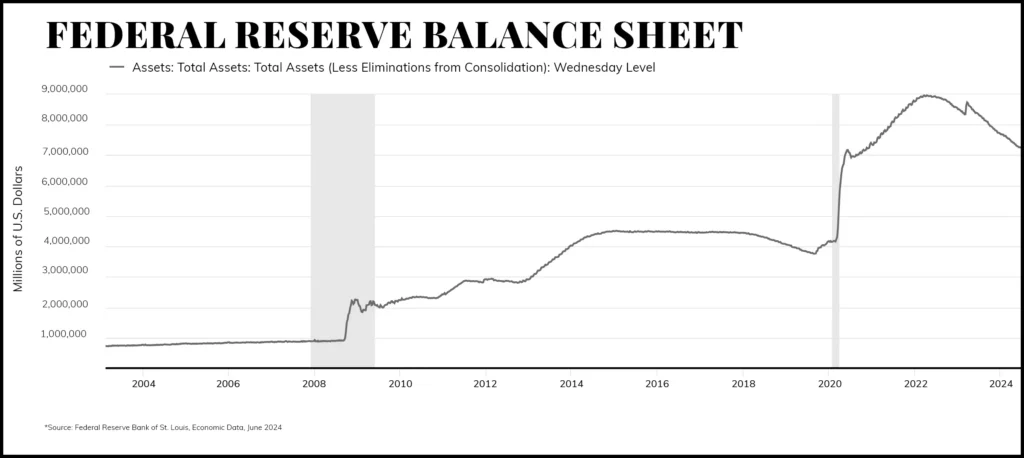

(3) “Quantitative tightening is the underrated story, one way or the other”

$2 trillion has come off of the Fed’s balance sheet since their tightening efforts began roughly two years ago. They announced a slowdown in the pace of tightening at the May 1 press conference, and lo and behold, an April sell-off turned into a May rally. And yes, it flew under the radar in financial media.

Look, the balance sheet is still (a) Way bigger than it was pre-COVID, and (b) Lower now than its high point. Do I think they can do a lot more tightening before they break something? No, I don’t. This story remains a high priority.

(4) China to split the baby on Japanification

Fiscal stimulus and support via spending, subsidy, and policy incentives? Check

Avoidance of use of monetary policy to Japanify their economy? Check

(5) Broader market participation

Hopefully, I have said enough and written enough about how problematic I believe the market top-heaviness is. If today were December 31, let’s just say this theme would not have played out as expected. But it is not December 31, and that’s all I can say for now.

(6) 2025 Earnings will dictate 2024 performance

The year started out with earnings expected to come in around $270/share in the S&P 500 next year, and the number is now $279 (an implied growth rate in 2025 of +14% versus 2024). So yes, a move from +11% assumed growth to +14% has pushed markets higher. And yes, any downward revisions to those expectations would hurt markets in 2024 a great deal.

(7) The election will not be as big of a market story as it is a news story

This was hardly a prediction as much as a repeating of historical fact, and I will make the case more in the September special edition.

(8) Prepare for much more volatility

So far, not true at all. It has been much more true in bond markets, but really not true in stock markets, yet, at all.

Path Forward

I am supposed to tell you that the average Q3 return in markets going back a hundred years is only +1.3%, whereas the average Q4 return is +2.9%. It is an insanely unhelpful data point in a given year since averages are created by the numbers over time that go way above or way below the median point.

But what we do have for the remainder of the year is:

- Clarity around 2025 earnings expectations (this will be big)

- Fed actions to begin cutting rates

- An opportunity for the valuation dam to crack (or not)

and - An election

I would say that this represents the major categories of things that will matter for the second half of the year, with the possibility of earnings revisions being most impactful. The Fed doing what is expected (small, late-year rate cuts) would be least impactful, but in the off chance that they telegraph something far different than expected (very unlikely), that could change things. The valuation wall holding is impactful in the same way that whether or not we have a tidal wave has a lot to do with ocean safety. It won’t matter if it doesn’t matter, but it does matter if it ends up mattering. You’re welcome. And just remember what you pay for this subscription!

The valuation story is, though, asymmetrical even if unpredictable. I have a very hard time saying with a straight face “the 22x forward multiple of the S&P may go to 25x.” I do not have a hard time saying, “The 22x forward multiple of the S&P may go to 18x.” I don’t know that the latter will happen, but I do think it fair to say that the odds of the latter are, shall we say, higher than the former.

The election will be a big story in the second half of the year, and right now as I type this I get a new text, popup, call, zoom, bulletin, report, rumor, etc. every eighteen seconds about whether or not we even know who one of the candidates is going to be. But despite the vast significance of the election in terms of the news cycle, the strong emotions it unleashes from various factions of the country, and the real relevance it has to American life, I do not believe it will be or can be the dominant market story of the second half of the year. I will have much more to say about this in a future Dividend Cafe white paper on all things election.

Chart of the Week

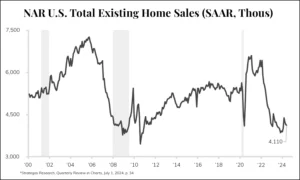

I didn’t spend a lot of time on housing in this edition because I believe the real narrative has been thoroughly discussed in these pages all year. But to graphically demonstrate the severity of the affordability challenge, supply-demand imbalance, and frozen market is, I think, important. To see existing home sales now, with less than 4% unemployment, with year-over-year wage growth at 4%, with corporate profits at record levels (and growing y/y at double digits), at the same level as the worst financial recession we have seen since the Great Depression, is just surreal.

Quote of the Week

“Essentially, all models are wrong, but some are useful.”

—George Box

* * *

I do wish everyone a very Happy Fourth of July weekend, and by that I mean, a celebration of this country and the experiment that has made it the greatest nation on God’s green earth. We have so much work to do. And we have such a beautiful set of ideas and principles to serve as a launching pad for this work, embedded in our founding documents. Endowed by our Creator with certain unalienable rights, indeed.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet