Dear Valued Clients and Friends,

We are going to do something unique this week – a deep dive into the massive country that is China. From stocks to bonds to history to currency to geopolitics, this is a big topic, and we do it this week with the sole aim of determining where there may be investment opportunity for our clients, and where there may not be.

It is a topic that reveals deep passions and emotions in many people. Our goal is to remove passion and emotion and be fiduciary investment managers with a burden for optimizing solutions on behalf of our clients. This has serious implications when you look at Chinese stocks or U.S. bonds.

I could make this introduction a full article if I wanted to, but let me resist the temptation to keep bloviating and ask you to dive right in. I believe it is a thought-provoking and useful summary of a few investment considerations in the fastest growing economic region in human history. And we want to get this right.

Some Call it Equity

The vast majority of China investment discussion these days, especially in the last couple of weeks, has to do with some form of Chinese equity markets. For a long time this has been the focus of much discussion because China’s equity market was on fire, primarily through a handful of technology names (much like the FAANG dynamic here in the United States). From a massive e-commerce company (sound familiar?) to a massive search engine company (sound familiar?) to a couple of major gaming companies and platforms (sound familiar?) to a couple of mobile and software companies (sound familiar?), China has seen great success come from a small number of “big tech” firms, and this has attracted great interest from U.S. investors.

And that attention has gotten more specific in the last couple of weeks with many names selling off as much as 25%, with much of the downward pressure essentially China-driven (more on that in a moment). Some niche sectors have done far worse (“education technology”) – with losses indicating potential insolvency. Total loss of market value has exceeded $1 trillion.

So whether it is more of an ad hoc tactical question about potential bargain-shopping in Chinese tech stocks, or the longer-term question about the growth opportunity of this space (past and future), there are legitimate reasons that U.S. investors have perked up as it pertains to the Chinese stock market.

Well, that is NOT the subject of this week’s Dividend Cafe. We will address this to some degree, but at the Bahnsen Group, we are not feeling some pull to adding a China-speculative sleeve in our portfolio management. We do invest in the Emerging Markets via a dedicated money manager – completely aligned philosophically to bottom-up characteristics and company fundamentals. And that manager may buy a few companies from China in their portfolio, but those decisions are company-driven, not country-driven. They are not “playing” China, and they are not speculating anywhere. And indeed, much of their philosophy around the risk of China equity investment has revealed itself in recent weeks.

Is China its own market’s worst enemy?

In the last few weeks, China has flat out nationalized some companies, nationalized (or threatened to) some sectors, and used a heavy hand to tell some companies how to allocate their profits. They have surprised some newly listed companies with onerous regulatory requirements. To be very blunt, they have acted out of control, unhinged, and reckless.

Except …

It hasn’t been remotely out of control or reckless for their purposes. In fact, it is quite purposeful.

Private equity companies would be utterly foolish to not re-think (or at least re-price) their intentions with Chinese market businesses. Listing on U.S. exchanges has become categorically more unlikely (if not impossible). Western appetite for Chinese equities has been dealt a huge blow. Why would this be good for China?

I am sympathetic to the argument that President Xi and the CCP want to leave a persistent reminder for the big-time executive class of China who is in charge, and I do think China is categorically against the celebrification of their business leaders (whereas in the United States, it is a way of life … See: Steve Jobs, Bill Gates, Elon Musk).

All of life is high school

I do believe there is a “you can’t break up with me because I already broke up with you” thing going on here. The pressure from U.S. regulators to clamp down on Chinese listings on U.S. exchanges has intensified substantially in the last year. I had to pull from my research archives a handful of pieces that I read just a year ago essentially arguing for the same risk in Chinese equity investment we are talking about now, but based on U.S. regulator action, not Chinese authorities.

An overkill on anti-dependency

But I believe more important than sending a signal to their business class, and even more important than fortifying intellectual and capital resources for more pressing national needs (an additional factor that should not be ignored), China does not want to become reliant on foreign capital.

Increased foreign capital not only pushes up the value of their currency, likely to levels that damage the competitiveness of their export economy, but it becomes more addictive economically over time. China does not want to rely on the west for capital, having already spent 20+ years relying on the west to be the consumer of their export-driven economy.

Could I think of a better way to diminish reliance on foreign capital than playing existential games with their great entrepreneurs and creative minds? Yes, but I am not a Communist or a totalitarian. There are entire philosophical, geopolitical, and even psychological factors at play that significantly impact the thought process here.

It really transcends reliance on foreign capital. It has everything to do with a broad reliance on the west – capital, customers, technology, etc. – China is very aware strategically of the advantages they have enjoyed by nature of the west’s reliance on them; the last thing they want is to have the shoe on the other foot.

Just so we are clear …

Not all of the policy decisions Chinese regulators or politburo members have made in recent weeks are necessarily bad decisions. Many of their decisions may well be for the wrong reasons, but still have some merit to them. Cracking down on securities margin lending could be useful in avoiding excess speculation and dampening the risk of an asset bubble.

But basically, the facts are as follows: When it comes to Chinese equities, there is little the CCP appears unwilling to do to force their private sector to align with the CCP’s social, economic, and national priorities.

A different way of thinking about risk and reward?

There is a bullish argument for increasing exposure to Chinese growth stocks (though it is not one I accept). Essentially, China equity bulls could easily assert that the risks of Chinese governmental behavior have always been known, are well baked in the cake, and that the fact that China can take down one of its own at will is just something to live with. High volatility and touchiness around bad news is to be expected, but ultimately their e-commerce and fintech industries are sure to create some serious global winners and one just has to grin and bear it.

It is not the way I think, and I am not comfortable with some of what is unsaid in this thinking. But it’s not the craziest thing I have ever heard – and I would give it 50/50 odds of working out for the risktaker who “grins and bears it.”

But no, we are not going there.

An interesting silver lining

For all of the unfathomable losses in value out of the Chinese growth sector in recent weeks, and what appears to be a genuine paradigm shift out of one of the hottest growth regions on the planet, it is fascinating that there has been no contagion risk through this escapade – like, none!

Suppliers and importers have not felt any pain. Banks and financial intermediaries have not really been involved here – it has not been relevant to credit markets. Global equities have not really suffered at all other than the emerging markets funds that have exposure to China or had to grapple with forced selling across their strategies (which has happened but has been contained).

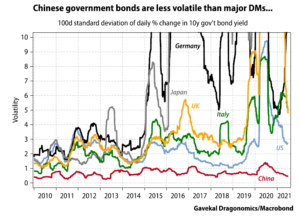

Now, what about bonds?

There are a lot of angles to address in this subject. Currency exchange rates. Capital flows. Population growth. Demographics. GDP growth differentials. Trade and budget deficits. So I suppose it ought not be made this simple, but sometimes bond yields really do cut through a lot of the noise. And why are we considering the sovereign debt of China/Asia for our client’s “boring bonds”?

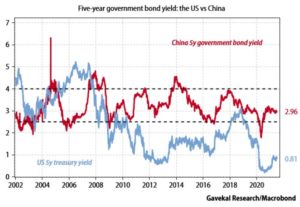

Because of this:

Essentially, a government-guaranteed bond with a five-year maturity pays well less than 1% in the states, and right around 3% in China (note: the chart above showed 0.81% for our 5-year Treasury; since this chart came out last week the yield has fallen to 0.73%).

Essentially, the delta between comparable spots on the yield curve between the two largest economic countries on earth is triple – that is, 3x the yield in China vs. the U.S. (apples to apples in maturity).

So are bonds different?

Something interesting happened through the commotion of Chinese equities these last few weeks:

Their currency and their bond market RALLIED. Investors did not take the instability of Chinese intrusions in the corporate equity sector as a reason to wholesale flee the region. And there is a reason that may get to the heart of the matter here …

If one accepts that the great risk in Chinese equity ownership is not merely the willingness of Chinese authorities to do things that could hurt U.S. investors, but also the motivation for them to do so, it is entirely reasonable to consider that bonds may not only be different but in fact, the opposite.

What is the greatest dependency China has in the world on the west? Why, the U.S. dollar’s reserve currency status, of course. Diminishing dollar-denominated trade in favor of yuan-denominated trade is perhaps the greatest Chinese objective of this century. What could possibly benefit that objective more than a structurally solid bond market – high liquidity – attractive yield premium – and all the things foreign investors would want from a bond portfolio?

Is that it? The yield premium?

Here’s the thing – no. Now, it might be news to experienced bond investors that there is something else besides the dependable income stream of a bond that they are supposed to care about, and I am not opposed to saying that all things being equal, generally yield differentials are good enough. But the problem with “all else being equal” with bonds is, all else is never equal.

Liquidity, currency, monetary policy, debt service, and GDP growth all impact investor decisions and outcomes in sovereign bond investing. Yes, we can start with the Chinese bond thesis by seeing that we get actual yields in their term structure vs. negative real yields in the United States. But our work cannot end there.

Some notables on the Chinese bond market

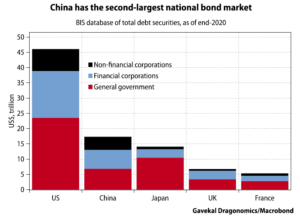

This is not a small market. We cannot look to a small or inefficient sovereign debt market for “boring bonds.” Yes, size matters.

This is the second-largest bond market in the world. Now, the sovereign bond size is larger in Japan than China (have you SEEN Japan’s national debt?), but the Chinese sovereign bond market is #3 in the world and the total bond market is #2.

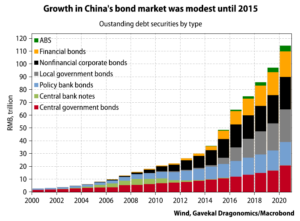

Historically, their sovereign bond market basically didn’t start until 1981 (the year Reagan took office, and also the year The Fall Guy debuted on American television). They issued bonds that year after decades of no debt issuance (throughout the Maoist Cultural Revolution). But truth be told, their bond market really just went next level (in terms of issuance) in the last five years.

The newfound diversification of the Chinese bond market (covering all asset classes of debt with size and scale) makes it much more like the U.S. bond market than Japan or most emerging countries. And yet, unlike the U.S., the “local government” bonds of China, not to mention their bank bonds, are essentially “quasi-national” bonds (think of it like Fannie and Freddie here in the U.S – they could be called whatever people want, but they were government bonds in the end).

This gives a unique and large blend of asset classes for bond investors to fish in, with deep and wide levels of options that do not forfeit Chinese sovereign backing. This feeds liquidity, optionality, yield differentials, duration optionality, and all sorts of things that fixed-income investors value.

The nuances of policy bank bonds and local government bonds in China would leave you in the Dividend Cafe for far too long, but the point I will make is that there are broad categories that enjoy sovereign guarantees and risk treatment and add to the fluidity and depth of the overall bond market.

There are also state-owned enterprises as well (corporate debt from companies the state has nationalized), but that is not at the heart of our inquiry. In other words, we believe they should be treated differently because they are different.

A Good Summary

Try to remember this line: “China’s bond market is large, domestic, and stable like a domestic market; but high-yielding like an emerging market.”

This is sort of the essence of the inquiry. Is there an arbitrage being made available to fixed income investors over the sort of “dual classification” of China as a developed economy and an emerging economy? That is our hypothesis, but we have more testing, challenging, and prying to do.

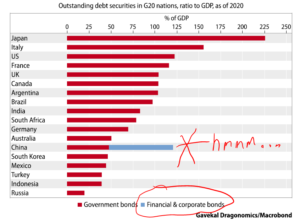

This “straddle” contains some indisputable facts. Capital flight is not a huge risk. Capital inflows are, in fact, the predominant theme right now. And while the size of the bond market (as mentioned above) is large, deep, and liquid, the pure sovereign bond market is under 50% of their GDP, whereas the bond market is over 100% of GDP of many developed nations like America, Japan, and Eurozone countries.

But, but, but. If you added some of the SOE bonds and bank bonds that have implicit guarantees in China that number more than doubles (again, think Fannie and Freddie). Now, of course, the problem with that pedestrian statement is that if you add the debt of the implicit or peripheral guarantees to your numerator you really need to look to the assets and the cash flows of the additional issuers in your denominator as well. But my point is, this point seems to be the reason for the yield premium.

Did someone say risk?

In other words, you have a country that should be AAA in terms of most bond characteristics, but it gets treated more like an A1 than a AAA (in layman’s terms, it gets treated as a good quality bond instead of a perfect quality bond).

Does China deserve a discount to its credit rating? It borrows entirely in its own currency (98%), versus emerging countries that have to denominate 10-40% of their debt in foreign currency. This is inherently stabilizing for China and inherently destabilizing for emerging countries that have an added large variable to the risk profile of their debt (currency exchange).

So I understand full well that for a bond investor, real risk is DEFAULT risk, but if one wants to use VOLATILITY as a measure of risk in sovereign debt, I guess Chinese bonds are LESS risky than U.S. bonds??

You have lower levels of foreign ownership in the Chinese bond market and much less central bank rate intervention, meaning a more conservative monetary policy that adds to the attractiveness of their bond market.

Some other tidbits

I have to wrap this up so let me just throw out a few other nuggets that add to the case here. Banks are large holders of Chinese bonds, and 64% of them (per a bank accounting study by my friends at Gavekal Research) have to be held to maturity. There is a very low turnover reality in the ownership realities of Chinese debt (more stability). And at the same time, there is ample liquidity as banks utilize repurchase transactions to serve as liquidity providers.

The liquidity profile is nowhere near that of U.S. treasuries, mind you, but increasing foreign ownership is bringing more and more liquidity, and different categories of bonds in their debt universe offer varying liquidity options. This exercise is literally a whopping five years old (technically it was opened a decade ago but there was basically no participation from foreign investors until 2016). We are in the infancy phases here.

Foreign governments and foreign central banks have become larger and larger participants in the Chinese bond market. And certainly, yield-hungry private investors have intensified their interest since 2019 (hence our inquiry).

A Fair Question

So for those following along, a reasonable summary of our position thus far may be this:

- Direct investment into Chinese equities is, for us, too riddled with uncertainty given the willingness and incentive of the CCP to intervene in a way that damages the value of that investment

- Direct investment into Chinese sovereign debt is perhaps in a different category, as the very thing driving CCP intervention into equity markets incentivizes a healthy and benign bond market environment

But a fair question to that second point may very well be …

Is it worth it?

Is the opportunity set to be found in that sovereign debt worthwhile relative to other possibilities for that capital?

Is the risk/reward ratio favorable?

An Entirely Different Angle

And then there is the question of the U.S.-China relationship itself … Apart from the straight analysis of U.S. investment in Chinese equities or U.S. investment in Chinese debt, what about the economic implications of the overarching geopolitical tensions between the two countries?

The first thing I should say is that this is not a discussion limited to the impact of investment in China; it impacts all investment, everywhere. There is no global investing (in the U.S. or out of the U.S.) that is not impacted by the U.S-China dynamic.

But I will comment more in a future Dividend Cafe on the overall U.S.-China relationship, and how it is being dramatically underestimated for its profound relevance to all risk asset investors.

The Moral Conundrum

Not only do we have appropriate risk/reward and economic considerations to sort through, as a vehement anti-Communist, I also have to ask myself:

Does investment in Chinese sovereign debt further the cause of the Chinese Communist Party?

Now, I do know the answer is most practically “no” – but there are differences of degree vs. kind that are important.

Conclusions

(1) We have a bias against direct Chinese equity ownership due to unpredictability and risk from the Chinese government, which has strategic objectives that currently desire less reliance on western capital, technology, and social structures.

(2) The same incentives that work to cause Chinese authorities to damage their own equity markets also work to cause them to support and stabilize their bond markets.

(3) Their bond market is a new phenomenon in modern global capital markets. It is large, liquid, and robust. And it offers a sizable premium to U.S. bond markets in yield/income.

(4) That premium in #3 is a by-product of China straddling the line between a developed and emerging economy.

(5) We are thoroughly vetting the economic assumptions, the risk/reward trade-offs, and the moral/political aspects to decide if sovereign exposure in “boring bonds” would be in the best interest of our clients.

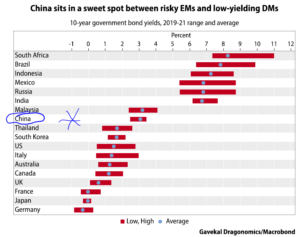

Chart of the Week

Is this the sweet spot? Nice yields that are well above the U.S. and Europe, but nowhere near the risk/volatility level of more unstable regimes?

Quote of the Week

“The best time to plant a tree was 20 years ago. The second best time is now.”

~ Chinese Proverb

* * *

I know this week was a lot, but this is a heady topic with a lot of hair on it. I hope you feel more informed on this than you did before you read it, and I hope you appreciate the opportunity and responsibility in front of us as we vet our decision and options.

Reach out with questions, and please know that if we are in the business of rushing decisions and chasing hot themes or marketable products, we would have pounced by now. But we believe in diligent, prudent, fiduciary decision-making because we love our clients. We really do.

To that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet