Dear Valued Clients and Friends,

I have been thinking a lot about the stock market lately, but not for the reasons most people think about it. The most common thing people wonder about the stock market is something like this: “Is the market about to go up, or down?” I think long-time readers of the Dividend Cafe know how I feel about that question (“long-time” could mean the last two weeks in this case).

I am always and forever agnostic about short-term moves in the broad stock market, not merely around anyone’s (including my own) ability to forecast such, but also around the relevance of it to one’s actual financial picture.

But I hear things said about the stock market sometimes that simply concern me. I am going to address a lot of those things this week and look at some basic historical facts of the market and the environment in which we find ourselves. My goal will be to look at what does not represent a “rough” or “troubling” market environment, and what does.

And in so doing, I hope we can find some takeaways about portfolio construction that speak to a present application that you will find useful.

What to do about this difficult market?

Roughly half of my investing life has been post-financial crisis and roughly half has been pre-financial crisis. I hear often people refer to this “rough market” or this “troubling market” and I wonder what they may mean, exactly. There are some legitimate things they could mean in saying such, but one thing they probably shouldn’t mean is that “rough” or “troubling” applies to the post-crisis returns.

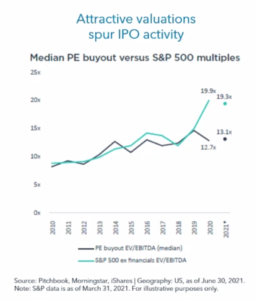

*YCharts, Ben Carlson, July 27, 2021

Indeed, in looking at the chart above one is struck by the fact that, with one year as an exception, the “bad years” were two years (2011 and 2015) in which the market was still up. Now, the market was down 4-5% in the Fed tightening/trade war year of 2018, but in 13 years you basically have had one barely down year, two barely up years, and then ten really up years.

If that is the “new normal,” I want more new and more normal, please.

So what is rough and troubling?

Perhaps what people mean is the volatility that has been endured to get to those returns in the market, but even there, some context is in order.

Yes, the COVID drawdown last March was nightmarish – 36% in 31 days. But the post-March market recovery began almost immediately, and that circumstance proved to be far, far less painful for equity investors than feared. Since the financial crisis, the annualized standard deviation of the S&P 500 has been 13.5%, versus an average over the last ninety years of 15.2%. In other words, the “volatility” of market returns has been about 11% lower than normal since the crisis. Hmmmmm …

An above-average return environment.

A below-average volatility environment.

And 12 of 13 years positive.

Valuations as rough and troubling?

So what could be “rough” or “troubling” about this kind of market environment? The part that I would dismiss is what I think most people mean – that it has been a rough return environment (it hasn’t) or that it has been a headache-inducing period of elevated volatility (it hasn’t).

Yet some may mean that it is difficult because valuations are high. And with high valuations, expected rates of return going forward are decreased. Okay, now we are getting somewhere.

But what does one do there? Do they wait to see valuations fall before they invest, or do they sell their current investments, pay taxes, and go to 0% return cash (negative real return) while they wait for valuations to drop beneath the historical mean in the broad market?

That may seem smart, other than the fact that it could take people out of a positive return environment for 3 years, 5 years, 10 years, or longer! What exactly is the re-entry strategy, and how effective has timing been around broad market valuations? I don’t want to belabor the points I recently made on this topic, but it ought to be readily apparent to everyone that playing the game this way does risk one of the outcomes we categorically refuse to engage – total destruction.

Concentration risk and leverage risk can blow someone up, and we believe one of the first aims of investing is survival. So we avoid those kinds of potential mistakes knowing that they could lead to really lovely returns when things go well because the asymmetry of the risk/reward bothers us (namely, having our faces ripped off).

But how does being on the sideline represent survival risk? Most investors cannot go 3, 5, 7, or 10 years with no compounding of their capital at all – and with negative compounding after accounting for even very modest price inflation. And for those withdrawing from their principal base in such a period, they literally and mathematically erode their capital – permanently. It is committing suicide to avoid being murdered. And it is painful to watch people do it.

Or is THIS the “rough and troubling” part?

I believe the most intelligent and nuanced way to speak to the “rough and troubling” part of current markets is in the context of central bank interventions. Returns have been high and volatility has been low, yet that has been in a period of unprecedented monetary policy accommodations. All of these facts are without dispute. The central bank interventions may mean nothing, they may mean a lot, but the facts of their existence are not controversial.

What I have long argued, and still argue now, is not that they are good or bad – but that they are unprecedented. I want to make two comments about this.

(1) The single most precedented thing in financial markets is the existence of the unprecedented. This is not an automatic disqualifier. Uncertainty and randomness and new historical realities are baked in the cake. They are part of the deal. Every war we have had since 1933 was unprecedented. Every recession had unprecedented components to it. Each bubble. Each burst. Each geopolitical foe. Each geopolitical alliance. Bad things are usually unprecedented in their specifics. Oh, and so are good things. We live in a world filled with apparent randomness on this side of glory, and the investment implications for that are profound.

(2) That said, the unprecedented nature of the current monetary environment cannot be dismissed as mere “par for the course.” There is ample work to be done (by us) in a period such as this. We may not know the answers, and in fact, we know that the people making the decisions do not really know the answers either, but what we can do is work from the position of humility that such a concession ought to create. And to that end, we do work.

Fed Reality

The nature of current monetary policy is not in the category of a “market headwind.” It is a societal, macroeconomic, prudential paradigm shift whereby our financial markets are more dependent than ever on a central body’s interventions. Would the removal of their interventions be problematic? Will there ever even be a removal of interventions? How problematic? In what way? I could list six more questions along these lines but the answer to all of them will remain the same – no one really knows. I consider this all de-stabilizing and problematic from a policy standpoint … all I want is to see investment assets grow from the discounted growth of their cash flows. Added complexity and instability from external interventions are difficult to price, difficult to assess, and certainly difficult to predict.

Investors today can act as if none of this is happening (the index approach), or they can act as if they know exactly how it will all play out (I don’t even know what to label this approach). Or, they can allocate a portfolio with a full recognition of these realities and uncertainties.

Here is rough and troubling

I am mystified why anyone would even think about the stock market as living in unprecedented times when the 10-year bond yield is 1.25%. The bond yield has been above 2% for 96% of the time the last one hundred years, and pretty much all of the time it has been below 2% has been, well, now.

Stock Market Summary

I have stated all this so much I genuinely fear being a broken record. But I also think this summary of our viewpoint is necessary to clip on your fridge (does anyone do that anymore?).

(1) I know broad market valuations are above average, yet also know that with bond yields (discount rates) so low, valuations are supposed to be higher than average.

(2) I know broad market valuations are above average, yet also know that valuation has never, ever, ever been a helpful timing mechanism.

(3) I know broad market valuations are above average, yet also know the bond market is in the most supremely above-average valuation of them all. Unless the average itself is changing? Heaven help us.

(4) I know broad market valuations are above average but do not buy the broad market indices for clients. Ours is an active, selective, process-driven approach – idiosyncratic and discriminatory each step of the way.

(5) I know broad market valuations are above average, and also know that the Fed now has its thumb on the scale of all parts of the economy and financial marketplace. This suggests the need to be humble, nimble, analytical, and hug strongly the principles of asset allocation, including the use of alternatives. It also suggests the benefit to “Fed-proofing” one’s portfolio as much as such a thing can even be done (it can’t) with dividend growth equities that transcend the broad marketplace (did you really think I was going to leave dividend growth out of all this?).

Alternatively speaking

We want to continue looking for alternative investments that can provide returns without necessarily adding to one’s equity market beta. Valuations in the private equity space, for example, sit well below the current public equity environment.

Illiquidity matters here. Income generation matters. It is a case-by-case decision based on each investor’s objectives and situation. But we can’t index our way to addressing all of these issues – an active, engaged, proactive, creative approach that seeks to optimize a risk/reward paradigm is needed and will be appreciated in the end. Private Equity is one area that I believe has been and will continue to be, a needed pursuit for the 2020’s investor.

In Conclusion

I could make you a list of all the “transitory” things that have impacted markets over the last 25 years, and I could further do so with the last 100 years. The “volatility” of being in the stock market is the reflection of those transitory realities – from currency debasements to hedge fund collapses to technology fears to tax increases to debt ceilings to accounting scandals to foreign entanglements to commodity shortages to beltway panic – there is no limit to things that can produce downside volatility.

But of course, there is no limit to what can produce upside volatility either. Solving for technology fears, actual innovation, improved accounting transparency, productive legislation, commodity normalization, enhanced peace in hot spot regions, superlative profit-making – it isn’t like markets have delivered the returns they have delivered for no reason.

At the end of the day, we have a market that scares some. That is a good sign. When NO ONE is scared, be scared. But we also have fear that is not entirely rooted in logic and facts, and we have an absence of fear that is not entirely rooted in clarity of the monetary moment.

Dividend growth equities.

Right-sized bond allocations.

Respect for the risk of credit (whether taking it or rejecting it).

Alternatives to adjust the risk/reward settings of the portfolio.

Realistic expectations.

Proper monitoring, diligence, and adjustment.

This formula is neither rough nor troubling. It is prudent and appropriate, and we are all in on it.

Chart of the Week

I had a different chart picked this week but replaced it this morning when my friend, Michael Poulos, of Marsh Advisory, sent me this gem. See, I can talk about Fed uncertainty all day long, but here is the 25-year reality we are living in: Velocity of money has declined at record speed as government spending and monetary coddling have increased at record speed.

This instability in velocity is not the cause of, but rather the reflection of, the key economic variable of our day: The expectation of declining future growth. We have to invest around it.

Quote of the Week

“The thing that most affects the stock market is everything.”

~ James Playsted Wood

* * *

I am working a great deal over the weekend and into next week on a special CHINA edition of the Dividend Cafe next week. I want to really assess for you what the risks are for U.S. investors in the current relationship with China, what the capital markets opportunities are, and try and drill down into the tensions we are wrestling with around Chinese equities being problematic, yet Chinese bonds being potentially appealing. This is a research project we are obsessed with, and even apart from its practical implications, carries a ton of peripheral lessons for us all.

I hate to leave you in such gripping suspense … =)

Enjoy your weekends, take in some outdoor sun, and reach out to any of us at The Bahnsen Group, any time.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet