Dear Valued Clients and Friends,

Markets staged a massive rally up Monday, a big sell-off Tuesday, and as of press time Wednesday morning, are poised for a huge rally up Wednesday. There is much that has to be said, and in this special mid-week Dividend Cafe we will look at the political impact on markets of the last week or so, the central bank action that has clearly entered the mix, and other portfolio considerations relevant to all going on in these new bouts of market activity.

Jump on in to this special mid-week Dividend Cafe …

Market roller-coaster

The market followed its worst week in years with its biggest point increase in history Monday, rising 1,300 points (+5%). Markets also recovered about 600 points late-day Friday (after being down 950 points late in the trading session Friday, we closed down 350).

As of press time Wednesday, and this is key because, by the time you are reading this, who knows where markets will be, futures are pointing to an open 600 points higher on the Dow.

So from the low point, Friday to where we are now markets have rebounded 2,000 points. And yet, they have not done so with a clear conviction that risk is back on. In fact, as we will talk about shortly, the ten-year Treasury bond yield went below 1% for the first time in history. And the market rally has come with significant zigs and zags – particularly in Tuesday’s trading session which saw markets down 300 then up 200 (500 point swing) then down 1,000 (1,200 point swing) then down 700 (300 point swing).

This high volatility is likely to continue before more real stabilizing takes place. A significant amount of weak hands were shaken out last week, but there are still computer and algorithmic factors behind whipsaws, and asset allocation issues as balanced portfolios deal with the action in Treasury bonds. The so-called “market timers” will soon throw in the towel if they have not already, and that will help reduce the see-saw effect.

All things being equal, “up and down” volatility (this week) is much preferable to “one-directional down” volatility (last week). But in neither case can we consider this environment normalized or healthy until the roller coaster ends.

Fed to the “Rescue” ?

The Fed announced on Tuesday that they were cutting interest rates 50 basis points immediately. The next FOMC meeting was not until March 17, so this mid-cycle intervention to cut rates represents their first “emergency cut” since 2008 (financial crisis). Prior to that, intervening rate cuts were more common (January 2008 stock market crash, August 2007 subprime meltdown, post-9/11 in September 2001, various market disruptions in 1998, etc.).

One could argue the subprime 2007 and 9/11 cuts were more focused on general economic conditions and financial system liquidity, but the other interventions listed above, and certainly the one announced this week, were clearly directed at the stock market. No one really believes that liquidity had yet been challenged or dried up in our credit markets.

So why did stocks sell off so much on a day the Fed came in to “rescue” the stock market? It really is quite simple, and reinforces the lesson about stock prices I am constantly repeating … Markets are discounting mechanisms, with prices responding to relative expectations, not merely absolute news. Markets had priced in, and this is not a typo, a 100% chance of 50 basis points of rate cuts, the day before. Tuesday’s announcement was just the Fed doing what the market was demanding of them days previously. For markets to have increased the Fed would have to have surprised markets, and this was not a surprise.

Futures markets are now implying a 54% chance of another quarter-point rate cut by April and a 40% chance of still another rate cut behind that by December. The Fed will do what it does and say what it says to manage expectations in the weeks ahead, but the rate market is assuming various levels of significant Fed easing.

It is noteworthy that the Fed action yesterday was unanimous, meaning even the more hawkish members went along with this.

QE ?

They did not announce any repo market extension beyond the plans already on the table through April, but depending on conditions, it is possible an update on their bond-buying will be a part of the regular March 17 meeting.

Central banks of the world unite

The Bank of Japan announced they will buy 500 billion Yen of government bonds via repos to boost liquidity in the Japanese economy. Imminent cuts are implied in Canadian futures pricing and European Central Bank pricing. Goldman Sachs has published a paper expecting far more rate cut activity in the U.S. than even futures are expecting.

October 2008, of course, represented one of the most significant central bank coordinations in history as the world burned in the depths of the financial crisis.

In March of 2011, I was reminded this morning that the G-7 intervened in unison to stop the surge in the Japanese Yen.

And most recently, in February of 2016, the world’s central banks profoundly intervened as China was unwinding from significant capital outflows.

* Jones Trading Institutional Services, Bank Policy Institute, Strategas Research, Corbu, March 2020

What this means and doesn’t mean

It may sort of “freeze” markets right now (afraid to go up too much, afraid to go down much further), pending more understanding of what is coming next. It does reinforce what I find it hard to believe anyone ever doubted – that the Fed sees themselves as an enabler of risk assets. But I do not see the Fed rate cuts as materially significant to economic and credit market activity.

My belief is that we will end up at a 0-.5% Fed Funds rate by the end of the year. I do not see it as relevant to suppressed economic activity or transitory impact from coronavirus in any way other than purely psychological. It primes credit pumps, and liquidity is important, but it has a very limited impact on economic activity at this level.

And, it has to be unwound, someday, somehow unless we want to admit to Japanification.

It really doesn’t matter what I think longer term. The market wants this as short term support, and the Fed has been offering short term support to markets for 22+ years (if not 33 years, depending on how you view these things).

Back to the VIX

August 24, 2015, the VIX hit 53. I remember that day well because it was the opening dedication day of Pacifica Christian High School in Orange County, a school I co-founded and had poured massive work and treasure into the prior two years. Markets dropped a thousand points, and the VIX went past 50, as markets feared huge economic distress out of China. The S&P 500, that day, was at 1,850.

Today, AFTER last week’s bloodbath, it sits above 3,000.

2020 now

So my hope for a 2020 largely driven by basic earnings fundamentals and devoid of Fed relevance is dead and gone. Eyes are all over central banks in the midst of a health panic. And earnings are obviously subject to significant Q1 distortions, transitory as they may be, from coronavirus. Best laid plans …

Why are markets responding this way?

A market down 13% in a week and a 10-year bond yield at an absurd 1% is indicative of full-blown global panic. Covid-19 seems likely to continue spreading in isolated pockets (the numbers are exponentially lower than one would perceive from media and market response). And yet mortality is quite low, and seems to indicate it will stay that way apart from older, more vulnerable people. The concerns (for markets) are not as health-driven or mortality-driven as they are supply chain and consumer activity driven.

Any improvement around serious government response, or any indication that Covid-19 proves less lethal and widespread than feared, sets up the catalyst for a rebound.

Ongoing issues and knock-on effects are likely, and global questioning of dependence on China’s role in the supply chain is at an all-time high. Capex is not likely to get the boost we wanted in 2020. There are questions ahead. But both things can be (and we believe, are) true at once:

(1) This reaction has been way overdone

(2) 2020’s fundamental picture has taken on deterioration

Maintaining Energy Exposure

The energy sector had been struggling before the recent market downturn, and the market swoon the final week of February only accelerated the selling. Some high profile energy companies now trade at levels never seen before, suggesting extreme under-valuation. But with that said, there is a reason that timing the value realization of this thesis may prove challenging. Energy capex generally slows down when oil stays meaningfully and persistently below $50/barrel. This, and then some, seems well-priced into the lead integrated energy companies, but many upstream producers with less quality balance sheets are vulnerable.

All of the energy sector has been under extreme duress lately, but only the midstream sector and high quality integrated names suggest extreme under-valuation, at the risk profile we seek.

This challenge exists in both directions – companies offering plenty of known good news often have prices that already reflect such; and companies with known challenges also often have prices that reflect such. That is our thesis on MLP midstream names and integrated leadership names. The issue of timing is a fool’s errand here. And yet as we will say as long as we have to – the challenge of timing the realization of true value, especially in the face of headwinds such as capex deterioration, is made much easier by very large dividend yields.

History

Average one-year return over the last sixty years when the “equity risk premium” (the earnings yield of the market less the ten-year treasury yield) has reached this level … +12.9%

Source: Strategas Research, Investment Strategy Report, March 1, 2020, p. 2

Anyone remember China?

All focus has understandably been on U.S. markets for U.S. investors in the last week or so. But with ground zero of the impact of the virus being in China, it bears watching the impact to their economy that the virus and its handling represents. The Manufacturing PMI number showed severe contraction from January to February (as expected). GDP growth for Q1 will surely be abysmal in China. This is much more related to the “cure” for the virus (i.e. shutdown) than the virus itself. The pace of economic growth recovery in China is what is hard to predict at this time.

Behavioral finance & human nature

One of the things that I hate about my market communications every time we have a market distress event of sorts is that I constantly feel that my attempts to provide historical context or data-evidence for what we are doing (are not doing) risks appearing to be inadequately sympathetic to the realities of human emotion. I may feel strongly that it is our duty to keep clients away from the behavioral mistakes that can be so tempting in market turmoil, but I have never felt that it was wrong for investors to have the emotional temptations and feelings they have. My focus on prudence, reality, evidence, history, and data is not meant to belittle emotion and human nature – it is rather to acknowledge it, and yet, through all of my sympathy and empathy, plead that those for whom we have a fiduciary duty not give in to their [understandable] feelings.

History of market turmoil

The bull market of 1982-2000 is widely considered one of the most amazing market feats in human history, with the S&P 500 growing from just over 100, to over 1,400, in 18 years (not counting dividends, not counting dividends, not counting dividends – it is not adequate to only point out once that this is not counting dividends). It would be news to investors of that era that there was no bear market in that great bull run – as 1987 saw one happen in a day, let alone a year, and 1990 and 1998 also generated 20%+ drawdowns!

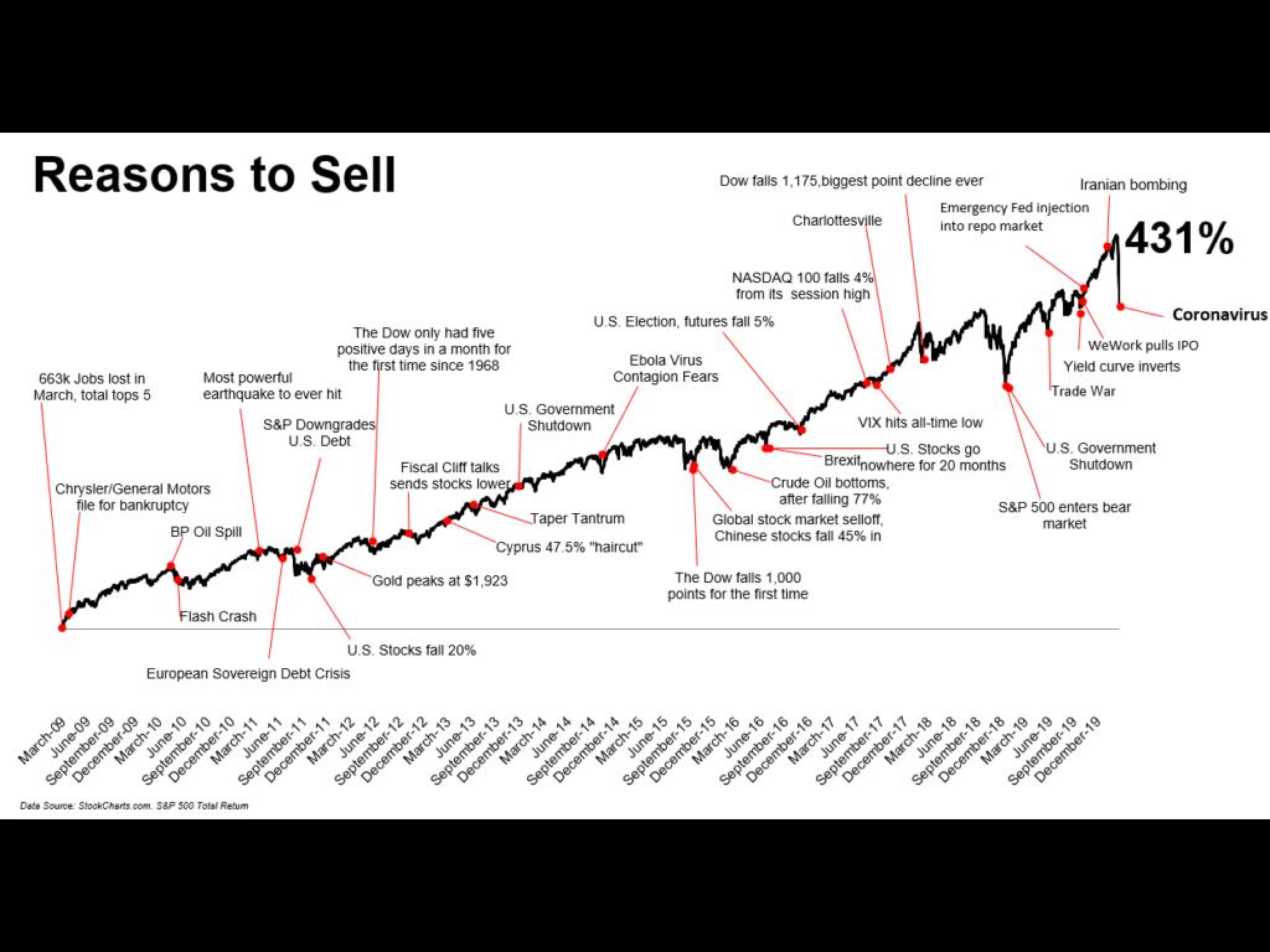

And the recovery bull market since the financial crisis has not been without turmoil itself (see the chart of the week), drawing down 20% in 2011 and 2018, with 5% and 10% drops happening dozens of times along the way.

These drawdowns, corrections, and bear markets had different reasons and provocations, but are part of the admission ticket to being a long-term equity investor. I do not like it, but I do not have a way to change it. The good news is that those who accept it and realize they have had no complaints whatsoever about their long-term results. In other words, it is not a bad trade off …

Politics & Money: Beltway Bulls and Bears

- The market action on Wednesday morning (again, as of press time, the Dow is pointing to a 600-point rally), and one could argue the even bigger move Monday (up 1,300 points) had some “Bernie Sanders weakening” effect behind them. Joe Biden’s crushing victory in South Carolina Saturday and his significant out-performance relative to expectations on Super Tuesday (last night) did precede these market moves higher. There is a huge danger of the “post hoc” fallacy in evaluating these things (i.e. “after this therefore because of this). And the risk of that fallacy is higher during periods of market insanity, where markets truly need no excuse to do anything whatsoever. And yet, the somewhat diminished “tail risk” of a Bernie Sanders Presidency intuitively seems to be part of the market action in these violent up days. Now, I want to be clear – I cannot prove it, and I cannot directly connect these dots. It is rare that cause and effect can be brought together in stock market action. But the fact of the matter is that betting odds had a Bernie Sanders nomination at 80% just one week ago, and the same electoral odds show a Joe Biden nomination at 65% now. That is a massive reversal, and while correlation is not causation, there is a significant correlation with market action throughout.

- Does this mean that the market loves the idea of a Joe Biden Presidency? No. In fact, Joe Biden has a better chance of beating Donald Trump, as far as market actors are concerned, and markets (all else being equal) would clearly prefer a Donald Trump re-election. However, there is something in finance called “tail risk” (low probability, high impact events). No matter what anyone thinks about the prospects of a Bernie Sanders Presidency (and he is absolutely still very potent and present in this Democratic primary – there is a long way to go!) – his “odds” have taken a huge hit in the last week. There were four candidates just days ago jockeying for the so-called “not Sanders” position (Biden, Bloomberg, Buttigieg, and Klobuchar). Today there is just Biden and Bloomberg, and Bloomberg is either headed out of the race, or headed to irrelevance in the race (having bet it all on Super Tuesday and having come up empty).

- The nomination process is not over, and there is a chance (a good one, actually) that the war between so-called establishment forces in Camp Biden and revolutionary forces in Camp Sanders will escalate, adding division in the Democratic side. The market will likely not mind that. I offer no political predictions here at all, for as we have just seen, four days can drastically alter expectations for a race. But I will say this: A coronavirus-driven collapse of stocks and the potential threat to the U.S. economy weakened Donald Trump one week ago, and the only viable candidate standing against him at that time was a socialist. Today, there exists a very formidable candidate for the right to run against President Trump in Joe Biden who, while still quite leftist in economic ideology, is not perceived by markets as the same threat Bernie Sanders is. Beyond those rather benign and factual statements, there is not much more that can be said.

Get used to hearing this

Declining share prices allow accumulators to pick up more shares when dividends are being reinvested.

Declining share prices do not effect withdrawers at all when the dividend stream they withdraw from is steady and even growing, not impacted by the natural movement of the stock market.

Every client is one of those two buckets. Every client should feel great encouragement from it.

Chart of the Week

This one sort of speaks for itself.

Quote of the Week

“The intelligent investor is a realist who sells to optimists and buys from pessimists.”

~ Benjamin Graham

* * *

It has been a busy week at The Bahnsen Group, and that is what it should be in times like this. We have gone to our lowest cash position since the year after the financial crisis, and we have had the chance to buy from our wish list positions we thought would never be “cheap enough” again. We also, of course, have used this experience to try and reiterate for our clients the timeless truths that drive our beliefs and commitments at The Bahnsen Group. During periods of elevated market distress, it can either be the best time, or the worst time, to pursue such an ambitious agenda. But on balance, it is the right thing to do – to tell clients the truth, always, to stand behind our convictions, and to posture the realism and humility that comes with having no idea when market conditions may normalize. I am proud of my team, my investment committee, and our advisors.

And most of all, I am blessed, immeasurably blessed, to have the clients we have at The Bahnsen Group. For them, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet