Dear Valued Clients and Friends,

As we go into this Easter weekend, markets closed on this Good Friday, I debated whether I wanted to talk about tariffs yet again. I don’t really see a way to avoid the topic right now, though I did use today’s Dividend Cafe to go around the horn with a variety of topics relevant to the current kerfuffle in markets – bonds, the dollar, exceptions, valuations, China, and more. I kept it shorter than the last couple have been, but there is a lot of information today intended to bring clarity to some subjects where clarity is needed.

I want you to have a Good Friday, and a blessed Easter weekend, so let’s jump into the Dividend Cafe, and get you on your way …

|

Subscribe on |

Entitled to Our Own Facts

Last week, the buzz was buzzing that China (or other foreign countries) were selling off U.S. treasuries to punish the United States for starting a trade war, essentially weaponizing their relatively modest holdings in our debt. There were (and are) a few problems with this thesis, mostly connected to how utterly absurd it is. But let’s dig deeper. What kind of weaponization brings the bond market all the way back to where it was, ummmm, five weeks ago, and does so for about five hours? I mean, come on.

The chart here shows the yield of the 10-year, so the price is inverted … Look at how we have basically been between 4% and 4.5% for about thirty months, with some periods of near 5%, and how the recent move didn’t get near those levels. It just defies math and the English language that some would call this “weaponization.”

But wait, there’s more … Isolating treasury market price action to U.S. market hours and to overnight hours tells an even clearer story. Treasury markets have a price increase of 3.9% in overnight hours but a price decline of 2.7% in U.S. market hours (h/t Strategas Research, Daily Macro Brief, 4/17/25). How can this be any clearer?

Human Nature

This week, there has been a lot of noise around waivers and exceptions granted for big tech companies via the administration’s announcement of a carve-out on tariffs for imported products from China related to smartphones, semiconductors, and computers. For some, the impression is that special favors were done for the big and powerful. For others, it looked like an admission from the administration that there is a huge cost to these tariffs, and they didn’t wish that cost to be evident with the most popular consumer product in history. For others, it was evidence of confusion in the messaging and the ultimate plan as to where these things were going.

I happen to believe there is truth in all of the aforementioned takeaways, but that the biggest takeaway is this: Huge efforts to receive waivers, carveouts, exemptions, and exceptions happen because of human nature. In a scenario like the one we now have: Tax policy (tariffs) that are at the executive branch’s discretion, with little specificity or clarity or binding force, there is significant wiggle room to get exceptions. Therefore, there is ample incentive to try for exceptions.

The desire for exceptions is not limited to multi-trillion-dollar mega-cap big-tech companies; every small business I have spoken with that is getting hit by tariff impact is also naturally looking for some form of waiver. The difference, of course, is that bigger companies generally have more resources (lobbyists, attorneys, government connections). In comparison, smaller companies often don’t know what to do (or it falls on deaf ears). We can’t change human nature, and we can’t change the law of big vs. small resources, so what can we do?

Well, we could always try policies that don’t play into this insidious reality of human nature, right?

Unpacking Negative Return Attribution

On a surface level, it looks like the largest stocks by market cap have come down in valuation from 31x forward earnings to 26x (with the impact on the broad market here being a decline of total S&P multiple from 22x to still pricey 19.5x). But those multiples are all based on FORWARD earnings, and there is simply no way to know if those earnings expectations are still valid. A stock price can drop because earnings drop, and it can drop because the valuation on those earnings drops, but it also can drop because of … both. That multiples have, so far, dropped most in the largest and most pricey part of the market is no surprise. But the next phase of dissection will be with earnings themselves, not merely valuations.

Still about China

As of press time, no phone calls have taken place between President Trump and President Xi, and no real signs exist for how the current tariff rates may come down. China has vast amounts of export products that can be, and are, routed through Vietnam (and other countries) to avoid the tariffs, and it does not appear the U.S. has the resources for enforcement (yet) to deter this.

It remains unclear what will happen to the current exempted products, what (if any) deal will come regarding current tariff rates, how currency exchange rates will be addressed, and what the real policy objectives are. I have to believe that as long as all of these things remain uncertain, markets will remain volatile.

Now, some have asked if I at least see the tariffs with China as a good thing to protect American interests against a foreign adversary. This is where the conversation generally changes to either “we must protect American workers” to “we must defend our national security” to “we must fight back against their unfair trade practices” to “we must stand up for human rights” – all of which are categorically different arguments with different applications that get lumped together to the aim of making so ambiguous the conversation, nothing gets accomplished. Let me just say that if the objective is an eventual decoupling from China, it will have to happen over a long period of time, and it will have to require U.S. alliances with other trading partners. Over the last two weeks, we tried to do whatever we tried to do in the exact opposite manner – a detonated bomb, not a sober and gradual decoupling – and alienating allies and global trading partners, not fortifying them in the objectives with China. But when it comes to human rights and national security, I confess to being confused by tariffs. Do human rights violations become less violative or morally offensive if we collect a tax? Are we looking to get paid for human rights violations, or to just shun human rights violations? Some clarity would be useful. As for critical infrastructure and national security, I support doing whatever has to be done to decouple those vital security interests from a global supply chain we cannot rely on or control, immediately. The problem is that I believe we can only do that if we actually define national security interests honestly, and you will forgive me for not believing Swiss chocolate, Colombian coffee, Vietnamese t-shirts, or Chinese plastics fit in those categories. By all means, become self-sufficient in the manufacturing of all that is vital to national security, tomorrow. Tariffs are not protecting national security – they are trying to get paid to keep our national security interests unprotected. This must be addressed coherently.

In the Meantime …

Longer-term realities aside, for what lies in store in our trade relationship with China, let alone what different (reasonable) people may believe about the complexities discussed above, what might we expect in the weeks or months ahead? It appears a lot is on the line as to who is more correct and who needs a deal more. President Trump and Secretary Bessent have correctly stated that China wants our business, and many others have pointed out that America wants (and in many cases, needs) their goods. It continues to seem to me that we are asking the wrong question to ask who needs whom more: When the answer is “both,” the question then becomes who has a higher tolerance for pain. I am afraid many Americans are in denial about the answer to that question.

We should note that about 14% of China’s exports come to the United States. I don’t want to minimize that: It is equivalent to around $500 billion of sales, and 14% is a big number. But it is not 30%, 50%, or something existential. And if China can pick up export sales by 1% here and 1% there with four or five other countries (Southeast Asia, western Europe, Russia, India, etc.), they could potentially see the net effect get down to 8% or 9% – still substantial, but not fatal.

Now, I am well aware of the President’s desire to see a deal reached. And I am aware of the vulnerabilities in China’s deflationary economy that promote them finding an off-ramp, too. I am not going to do what I criticize others for doing – predicting an outcome when I have no basis for such a prediction. I will just say that I think trade wars have the same winner as nuclear wars – no one involved in them.

Bowling for Dollars

I have put my cards on the table many times when it comes to a discussion of the U.S. dollar. I have passionately studied economics since I was in middle school, and I have professionally managed money for 25 years, and it has always rung true that very few things demonstrate more confusion and misunderstanding than when people speak about the U.S. dollar. Perhaps one of the only things more perplexing than listening to people, pundits, and others talk about the dollar is actually watching people try to trade currency … it is like watching a car accident when you know the accident is coming.

But over the last week, we have seen people claim “that the dollar was crashing.” The DXY, a measurement of the U.S. dollar against a trade-weighted basket of other currencies, was down about 3%, still about 10% higher than it spent most of the last decade, and much higher than it spent the decade before that. You would think these people alleging dollar crash conditions would look at a chart.

The dollar is not going to lose reserve status, and for now, I don’t have to defend that claim on an absolute basis (i.e. why there is no argument for such) – it is perfectly adequate to defend it on a relative basis (i.e. who exactly is supposed to replace it?). But that the administration wants a modest weakening of the dollar’s foreign exchange value is hardly a mystery. Some in the administration have even said they believe dollar strength has been the source of great pain for U.S. manufacturers.

But is it worthwhile to forecast what sectors and companies are most likely to benefit from relative dollar weakness? The challenge is that we can’t stop at first-order effects. On one hand, policymakers in the U.S. may want a weaker dollar. But on the other hand, other countries have ample incentive to weaken their own in response to tariffs. Can a currency deal be reached? Sure. If there is, would it likely result in a modest weakening of the dollar? Of course, no accord is coming that strengthens the dollar! But a “crash”? Trading a long and short (buy and sell) side of this? Predicting the loss of reserve status?

As crazy as it was in middle school. I remain passionate about the subject.

A Lot of Things I do not Know

I do not know what “trade deals” will get announced in the next 90 days with 70, or 100, or 130 countries that were in the tariff announcements of April 2 and are now in a 90-day “pause” with negotiations allegedly underway.

I do not know how much of what transpires with these countries will be substantive versus cosmetic. I do not know what will be needle-moving in facilitating more trade that drives U.S. economic growth, versus how much will “sound good” but be somewhat token.

I do not know if there is a possibility of these “negotiations” falling apart and some drastic “re-tariff” announcement coming, bringing us back to pre-April 9th market conditions. I am skeptical that the President will let that happen, but I can’t rule it out. He keeps Peter Navarro on his team, so I can’t rule anything out.

As discussed above, I do not know where things will go with China discussions – what may get better, get worse, or become baked into market and economic conditions.

I do not know if the U.S. economy has already tipped into recession, will tip into one in Q2 or Q3, or will somehow avert one altogether. My projections are that substantial deferral of capital goods investment has already taken place, with a threat of layoffs picking up in the near term.

I do not know what additional carve-outs, waivers, and exceptions will be granted in this ongoing saga, or what the fate of the current ones will be. I do know there will be millions of requests.

One Thing I Do Know

What I do know is that a tax bill is one of the lowest-hanging fruits for some form of benefit to the economy amid all this uncertainty. First, there is the urgency of avoiding $400 billion of tax increases in January if Congress does nothing. I am confident that, at a bare minimum, that will be addressed (I am less confident that markets will care if that is all that is done; I have to think it was baked into market expectations that this extension was a given). Nothing about extending the status quo is stimulative – that is why it is called “status quo.”

From there, the administration wants (in order of priority):

- No tax on tips

- Lifting of the SALT deduction cap

- Incentives for domestic production

- No tax on overtime

- No tax on social security

That last one is the most expensive, and candidly close to impossible mathematically (and politically).

Can Congress use tariff revenue estimates in how it constructs the budget reconciliation? That remains to be seen. Congress has not passed these tariffs; the executive branch itself puts them on again and off again every other day, and by definition, the stated intent of the tariffs is to not raise projected revenue (because activity shifts as a result). The whole thing is outrageous, and the CBO is not likely to score it, but how Congress treats this will be very interesting.

I believe bonus depreciation (100% expensing for capital equipment) will work its way into the final bill, and that this may be one of the most under-appreciated parts of all this for markets. It happens to be off the media radar and political radar, and that may prove a good thing.

There is, by the way, more talk (even with bipartisan support) of increasing the tax on stock buybacks. And yes, I imagine this is, net-net, beneficial for dividends. It is also outrageous, bad policy, and not part of my investment case for the superiority of dividends.

There is substantial committee work to be done, and the House has to take the lead there. From there, we go to the Budget Committee and then the full House and Senate. And from there, if still standing, it goes to the President’s desk.

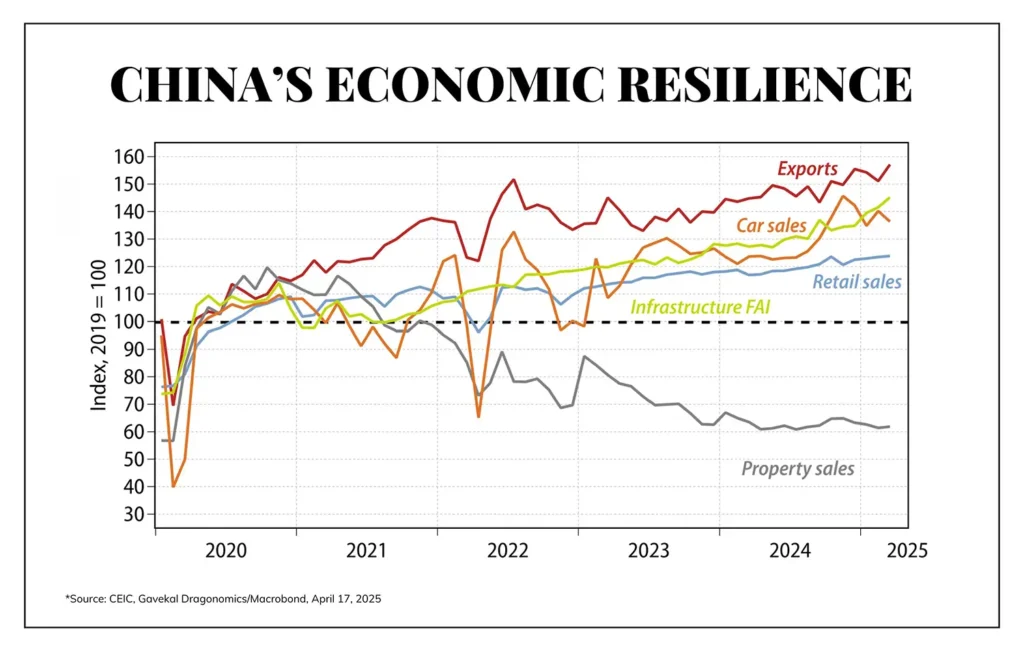

Chart of the Week

China’s property market is the problem. The rest of their economy paints a different picture. But deflationary busts of inflationary bubbles do a lot of collateral damage. We should know!

Quote of the Week

“All past declines look like an opportunity, all future declines look like a risk.”

~ Morgan Housel

* * *

I will be in Dallas, TX, at the beginning of next week and couldn’t be more excited for our expansion there. I will end the week in Newport Beach. It is a meeting-filled week, to say the least – just the way I like it.

I wish everyone a truly wonderful Easter weekend! History will never be the same.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet