Dear Valued Clients and Friends,

I hear often from investors who are focused on the “fun” parts of risk-asset investing that they “don’t care” about the bond market. Truth be told, it doesn’t do a lot to excite me, either. Most professional bond managers I know seem to be borderline Communists (just kidding), and the bond market itself lacks the human action that I believe is embedded in things like operating enterprises.

But the bond market cares about us whether or not we care about it, and that is the subject of today’s Dividend Cafe. It is a message I like a lot, and I believe if you jump into today’s Dividend Cafe, you will come out more enlightened about economic growth, stock market pricing, interest rates, and the decisions we face as investors.

So let’s do just that.

Podcast Transcription Download

|

Subscribe on |

The Mother’s Milk of Stocks gets Complicated

“As earnings go, so goes the market.” This is both true theoretically – stock prices are an encapsulation of expectations of future earnings streams discounted to a present value – and also true directionally – the general direction of earnings (up or down) speaks to the direction of market prices (up or down).

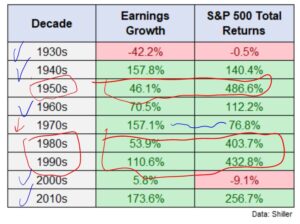

As you can see in this chart, the 1930’s and 2000’s saw lousy earnings growth and lousy stock returns. The 1940’s, ’60’s, and 2010’s saw good or great earnings growth with pretty proportionate good or great stock returns.

But I want to talk about the 50’s, 80’s, and 90’s, and then the 1970’s as well. In all four decades, the same principle is at play, but in the case of the 70’s, the principle is working the other way vs. the other three decades. What I am referring to? Earnings growth and Stock Returns are directionally the same, but mathematically far, far apart. What is going on here?

First, the good decades – the ones everyone likes (and pretty much what too many have come to believe is the norm). In the 50’s, 80’s, and 90’s you had good earnings growth, I would argue good in the former two and great in the latter, but you had insanely good stock returns. This is classic multiple expansion. Stock investors got earnings (sine qua non for good returns), but they good a growing P/E ratio to go with it, disproportionately boosting stock market returns relative to underlying earnings. Good times.

Note the same was actually true in the last decade, too, but (a) We are talking about 1.5x the market returns relative to earnings growth, not 5-10x seen in other decades; and (b) The earnings growth is really over-stated because the 2010’s saw earnings coming out of the trough of the Great Financial Crisis, so, you know, it is easier to gain weight after a two-week stomach flu (if you catch my drift).

But here’s the point. For the last forty years, we had three great decades for stock returns where earnings growth was good or great, and valuations were explosive. In the midst of that, we had one decade where earnings were terrible, and returns were terrible. Multiple expansion has become a core part of investor expectations.

What about the 1970’s? Here you have pretty spectacular earnings growth, but with really muted stock returns (the only decade in the last hundred years to pair these two phenomena). Why? Well, it is simply a reversal of the math in the 80’s and 90’s – that is, multiples contracted. So earnings were what they were, and they kind of kept equities from collapsing, yet returns were lower than the math of the profits themselves as rising interest rates put downward pressure on stock prices.

But the dividend can save us, right?

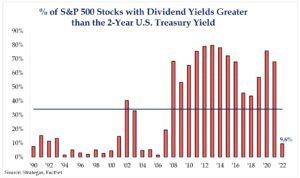

I like the way the guy who writes these sub-titles is thinking! Certainly, one other element that factors into stock returns beyond the earnings and the earnings multiple is the dividend (though it must be pointed out that really the dividend at some point has to be understood as a component of the earnings, but yes, the differential in the dividend is how management is treating the shareholder). So some may believe that one way to juice stock returns in a period where returns are muted by declining valuations is to grab the big dividend names.

But what does one do when those stocks are not there? A “big” dividend name is a relative term – 4% is a lot when bonds pay 1%; it is less when bonds pay 4%. The amount of companies in the S&P 500 currently paying more than the bond market has dropped from 75% or so most of the time since the financial crisis to less than 10%.

*Strategas Research, Daily Macro Brief, Oct. 14, 2022

What is one to do?

Hint: Focus hard on those names that do offer superior yields, with the sustainability of growth in those dividend cash flows, with management aligned and inclined to do so, and a business model that supports it all.

Understanding comes before action

Pointing out the math that $10 of earnings times a 15x multiple equals $150, whereas $12 of earnings times a 12x multiple equals $144, is not very helpful. I presume either that readers of Dividend Cafe can do that kind of multiplication or that they have access to a calculator. When two numbers are multiplied together, one going down (or up) – the multiple – can have an impact that is either positive or negative regardless of what another number is doing (the earnings). This is the easy part.

The question is answering why it happens, and I have gone to great lengths to try and explain the intersection of earnings and valuations. But even pointing out how P/E ratios work is inadequate; quantifying multiples to stock prices is one thing; qualifying why and for what reason a valuation may change and why and what for why reason a bond yield may change is entirely different.

The Purity Test

We use treasury bond yields to measure the state of interest rates because they are the purest, most reducible vehicle for such. Corporate bonds reflect the up-and-down reality of interest rates but also credit risk, where Treasuries allow investors to only think about the yield – not the likelihood of getting paid back vs. default. Whether a corporate bond is risky (high yield, junk) or relatively safe (think Apple or Johnson & Johnson), there is some factor in pricing unrelated to the interest rate – some thought around credit. And the same can be said about most other governmental bonds – we don’t think that Italy will default on a bond payment, but it’s sort of possible. We don’t want Peru to default, but we know many emerging countries do. We don’t expect Chicago to default on a muni bond (okay, bad example), but we know it’s possible (i.e. Detroit).

But Treasury Bonds allow for purity in yield free of credit and default considerations.

Lending the government money

And so why does one lend money to the U.S. Treasury?

Well, if it is you or me, it is for a safe return of our capital at maturity with a guaranteed interest payment along the way (one that is state-tax-free but not federal-tax-free). There is no currency risk like there would be if we bought the bonds of another country (we buy in dollars and sell in dollars if we are U.S.-based investors). And the interest we get reflects a number of things that we are about to discuss.

What if it is China or another country? China sells a million things to the United States, and they get paid in dollars. But their country has its own currency, so when they get all these dollars as payment for the things they sell us, they can’t just circulate them into their banking system. So they hold the dollars as “foreign exchange reserves,” and the safest and most liquid way to do that is to buy U.S. treasuries.

What if you are the Fed or a central bank? Well, in this case, the Fed is generally buying a Treasury bond from a bank that owns one to increase cash in that bank’s reserves and then to put that bond on its own balance sheet. Why? To put downward pressure on interest rates (as a policy tool) and to add liquidity to the banking system (as a policy tool).

And in all cases, the buyer (you, me, China, the Fed) gets an interest payment that reflects a number of realities.

Bond yields say what?

As a general rule, I have always liked this formula:

A bond yield (the price the market is putting on the time value of that bond – the money one wants to be paid to be separated from their money for a given amount of time) equals: The Fed Funds rate (overnight bank lending rate) PLUS expectations for Real Economic Growth PLUS expectations for Inflation (in other words, nominal growth). So if the bond is a 10-year maturity and the Fed funds rate is 2%, and one expects nominal growth of 3% for ten years, a 5% payment per year is a logical expectation for the yield. If the Fed Funds rate is 1% and one expects growth of 2%, then 3% is more logical, etc.

It doesn’t work like this day by day, and there are shocks to the system, surges of demand, excess supply, shortfall of supply, volatility in inflation expectations, recessions that hit growth, booms that push growth higher, and all sorts of other factors, but played out over time, I stand by this formula:

Fed funds rate + nominal growth expectations

And again, nominal growth itself has two components: Inflation, and then economic growth.

The 80’s and 90’s

Let’s make this as simple as can be:

Economic growth expectations were good in this period of a golden bull market in stocks and bonds (so that would theoretically push bond yields up a bit, BUT inflation expectations came way down, especially from the high level of the 1970’s), so bond yields came down pushing bond prices higher. This elevated stock returns (see above), and was a dynamic period for borrowing money, for housing, for anything utilizing leverage, etc.

2008-2020

Let’s make this as simple as can be:

Economic growth expectations were muted. Inflation expectations were close to zero. Bond yields came way, way down. The Fed Fund rate was zero. This allowed great returns for bonds (yields down, prices up), and for stocks (higher valuations), even in the midst of low growth.

Why did growth and inflation expectations come down? Well, if there is anything I can be accused of over-discussing, it is this, but the answer is: Excessive indebtedness led to an increase of fiscal and monetary interventions that led to declining growth and less confidence in the growth outlook for the future.

2021-2022

Let’s make this as simple as can be:

The world was shut down in 2020, and growth expectations went negative. It re-opened in 2021 with no production from 2020, and a diminished capacity for production in 2021, yet with normalized demand coming out of the shutdown. In fact, demand had been “pent-up,” so there was an “extra” low supply combined with “extra” high demand. It was all about the COVID policies on the front end and on the back end, and why no one talks about this is the great frustration of my life as an economic analyst.

You furthermore had significant transfer payments that added a sugar-high to spending, you had 0% interest rates facilitating leverage, you had a labor shortage, you had a cessation of semiconductors getting into the country, you had global trade pressures as other countries stayed locked down (maybe they hadn’t seen The Last Dance when we all did?), and you had no ability for the supply of commodities or finished goods to catch up to the moment.

That is called inflation.

Bond yields went up. BUT, the 10-year bond yield and the Fed Funds rate are not that far apart. So let’s go back to my formula:

A 10-year bond yield equals: the Fed Funds rate plus NOMINAL growth expectations.

A 10-year is about 4%, and the Fed Funds is about 3%. This implies a 1% nominal growth rate. Either inflation will be 1% and growth 0% or inflation will be 2% and growth -1% or something thereabouts (if you ask the bond market). Now, of course, the 10-year is pricing in that the Fed funds rate may (and will) come down, too, but soaking wet you are not seeing much more than 2-3% of NOMINAL GDP growth priced in the bond market, which means 0-2% of real economic growth, SOAKING WET.

2023-____

I understand we are all obsessed with what the Fed will do tomorrow and next month, and that won’t change until CPI comes down, the Fed stops hiking rates, and things feel more normal on this front. We don’t even know yet what the hangover will be, let alone the rehydration.

Yet I believe the message of the bond market, and the message it is most likely to impose upon markets in the years to come (not months) is that excessive indebtedness is still the elephant in the room for growth and inflation expectations. The Fed can control the overnight rate, but they cannot control the long end of the curve – the big bad bond market. And unless you believe nominal GDP growth is going to be double what it has been despite all the headwinds to growth we face (it will depress me to no end to make a list for you right now of what those headwinds are, so I won’t), you might consider the possibility that bond yields top out and head lower in the remainder of the decade.

Not for a good reason, but a bad one.

Conclusion

But I am going to propose that bond yields starting the next period of time at 4% is a very good thing for investors who have had no benefit of diversification from stocks and bonds for some time. There is less distortion of asset prices at a higher yield. There is less mal-investment. There is a hedging benefit in incorporating both asset classes into your portfolio (stocks and bonds).

Alternatives are needed to round this out. Either when bond yields are too low to do anything for risk mitigation or return supplement in your portfolio OR when bond yields are going higher (2022), hurting your portfolio, alternatives matter.

But we may have three arrows in our quiver going into 2023, not two, and that is a good thing for those who read the tea leaves correctly.

2022 has been a correction of excess, a reversal of COVID insanity, and a pendulum shift from one extreme to another from central banking deities.

The go-forward period doesn’t offer what I most want for my kids, future grandkids, and overall society – robust real economic growth (see: 1980s and 90s). But maybe, just maybe, we can use a 4% bond yield to our advantage.

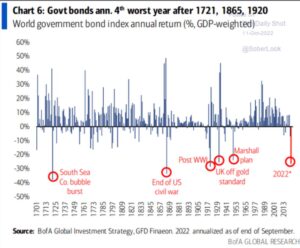

Chart of the Week

I am not sure what to think about the measurement of bond returns in 1721 when churning butter was the most profound technological advancement of the decade, but I do know this: 2022 is going in the history books for global sovereign bond returns.

Quote of the Week

“It is ordained in the eternal constitution of things, that men of intemperate minds cannot be free. Their passions forge their fetters.”

~ Edmund Burke

* * *

Well, there were some weird days in the market this week, but the weirdness may be around for a while. I am off to New York City with Brian and Kenny to sit down with some of the smartest people on the planet (plus some bond managers – just kidding) to talk markets, economics, and strategy. I will have a lot more to say after 20+ more meetings.

In the meantime, may your weekend be delightful, may the Cowboys beat the Eagles, may USC do what they need to do in Utah, and may no one ever believe that people having jobs is inflationary. MORE goods and services = less inflation.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet