Dear Valued Clients and Friends,

I understand it may seem odd to devote a Dividend Cafe to the particular subject of the Energy sector in a week of surreal market volatility and media obsession over the Fed. But in fairness, I write about the Fed almost every week, plus four days a week in The DC Today, and the entire subject of monetary theory underlies all that we do in capital allocation at The Bahnsen Group. Our nuanced views on the role the Fed currently has in financial markets are known, and to co-opt my planned Dividend Cafe subject yet again to cover the thrilling story of the Fed moving interest rates exactly how we knew they would, is not going to happen.

But the Fed was not the only story (non-story) this week. Markets are in a pattern of daily incoherence as traders, algorithms, novice investors, speculators, and other such inconveniences work through the challenges of a paradigm shift. What the futures say at night has nothing to do with what they will say in the morning which has nothing to do with what they will say at the open which is fully disconnected from intra-day activity which then leads to a totally unpredictable market close. Then, rinse and repeat.

My only exhortation is – thank God none of this means a thing. Not a thing. Totally irrelevant. If the intra-day gyration of the market on a random Wednesday has ANYTHING to do with the life goals of a human person, that human person deserves a new advisor and investment strategy. Actually, they may not deserve it. But they certainly need it.

So I’ve written about our low opinion of “shiny object” investing, and the avoidance of such has a lot to do with the way our January has (thus far!!??) gone. But the energy sector is up +18% this month as of press time in a YTD market that has a Nasdaq down -15% and S&P 500 down -10%. We need to look at that. Is Energy becoming a new “shiny object”? Is the sector a trade or a long-term opportunity? What aspects of energy investing appeal to us right now? Where do environmental, political, and macroeconomic concerns fit in? These subjects all deserve their own Dividend Cafe, and that day is today.

So jump on into the Dividend Cafe …

Where do things stand?

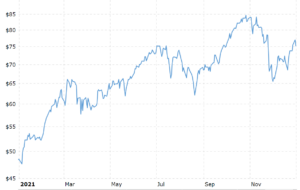

As I wrote about in our annual white paper reviewing 2021, Energy was the top-performing sector in the stock market last year, increasing between +45% and +55% depending on which index is being used. A significant component in this recovery is, of course, the increase in the price of crude oil. Following the efforts to limit new supply in the COVID moment of 2020 and the resurgence of demand in 2021, crude prices moved from $48 to $76 last year, bringing back needed profit margins to the upstream sector along with significant production incentives.

*MacroTrends, WTI Crude Oil, 2021

The rally has continued in the new year, with energy far and away at the top of the pack, and creating a stunning +33% delta at press time between energy (+18%) and the Nasdaq (-15%) – all in 18 trading days.

This Time is Different

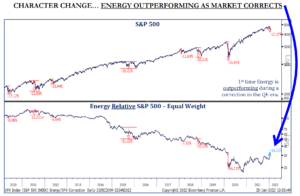

We are in the eighth period of the post-crisis era (since 2010) where the S&P 500 has declined greater than -10%. In each period we have seen to date – seven out of seven times – Energy performed worse than the market itself during a market correction. This correction the market is in right now is the first time that Energy has outperformed the market during a market correction (and done so by bucking the entire directional trend).

*Strategas Research, Technical Strategy Report, Jan. 26, 2022, p. 3

The technical strength is hard to overstate in the midst of this correction. A stunning 80% of energy sector stocks have made a new relative high vs. the market since the correction began.

Some Background

But there is more going on than just the higher price of oil (and natural gas, for that matter). The profits of the energy sector do not just rely on the price of the oil and gas being sold, but of course, the amount being sold – and the forward anticipation of what will be sold. The profits of the upstream sector where exploration and production take place are heavily dependent on both price and supply. The profits of the midstream sector where we have a special interest are dependent on volume, both in terms of the amount of oil and gas going through current pipelines, but also anticipation of future projects that represent entirely new revenue streams. In other words, there are two levers – more oil and gas in current projects, and more new projects.

The upstream and midstream sector have one particular thing very much in common: a heavy reliance on capital markets to fund Capex. Years ago I boldly preached the economic reality that commodity prices were a heavy input in the profit levels of producers, but that only volumes mattered to the midstream companies. I used the toll road analogy to say that the price of the cars on the road was immaterial; only the quantity of cars using the toll road mattered to their revenue model. And I think all of that was accurate as far as the point I was basically making, but in investment reality, there was another factor where upstream and midstream sectors were heavily correlated – access to capital markets.

If providers of debt and/or equity were going to sour on both sectors, I would cause a great deal of price correlation between the two – and that is essentially exactly what happened. The midstream sector required a lot of capital to fund Capex, and it had gotten used to selling new equity to make that happen.

No Soup for You – Part 1

In 2015, there is no question that capital markets turned on the energy sector. Very simply put, much of the Capex-dependent sector (upstream and midstream) ran into the ultimate negative feedback loop. They needed new capital to fund growth, but they needed new growth to rationalize new capital. As equity values declined, the self-reinforcing cycle kicked in whereby capital was harder to access. As capital became either more inexpensive or less accessible or both, equity values declined further. Rinse and repeat.

This was a period of self-awareness. Capex-sensitive industries have always had a sort of paradox here (REITs are not immune from this). New projects can command new capital as long as they suggest economic growth and value creation pro forma, but growth and value creation are in a pair trade with capital whereby the loss of one assures the loss of the other, then accelerates value destruction. Capital allocation became more responsible. Non-bank lenders became integral (private credit and private equity exponentially increased their exposures to the space). Free Cash Flow regained its status as a priority. Debt-to-Assets and Debt-to-Income ratios mattered again, with those ratios that impressed investors commanding a premium.

Tax structures changed. Shareholder-friendliness was back en vogue (for many operators – not all). Many GPs stopped charging their LPs for something called IDRs (Incentive Distribution Rights), one of the most abused mechanisms in the history of corporate finance. Essentially, the general partner had incentive to grow the distribution to the limited partners because of the premium cash payment the GP was assured to receive. However, over time these IDR’s added heavily to the cost of capital for the LPs and became a true failure of governance. Most companies in this 2016-2019 timeframe eliminated their IDR’s and the general partner and limited partners now find themselves on totally equal footing as it pertains to distributions.

So from 2015-to 2017, distress and excess in the sector deteriorated credit quality, skyrocketed the cost of capital, and forced truly constructive changes in the fiscal habits and capital governance of most energy sector constituents.

No Soup for You – Part 2

But the industry’s access to capital was not fully restored after the adjustments of the aforementioned era. While debt ratios came in and policies changed for the better, a simultaneous change in the culture was adding an entirely different impediment to capital access: the new trend in so-called ESG investing, and the political winds that blew hard against the fossil fuel industry.

Some more rational actors worked hard to educate the public on the realities on the ground. Global demand for energy was going up at an accelerating rate, non-carbon solutions were not even remotely close to being able to meet the need and demand, and far dirtier solutions (coal, China, Russia, etc.) were the only other way those energy needs would be met if we turned our nose at American oil and natural gas. Some modest attempts were made by those with concerns over carbon emissions to make the case for natural gas, which emitted the least carbon of the fossil fuels by a wide margin, and which offered the U.S. the best opportunity to meet global energy needs without relying on dirtier global producers.

The environmental case for continued improvements in the U.S.’s own production capability was ignored by the new crusaders, and a strange but powerful consortium of actors (politicians, think tanks, celebrities, pension funds, Wall Street marketers, and other unmentionables) took control of society’s narrative on energy production and consumption in the U.S. Well, the “narrative” is not really the point – they took over the capital allocation.

And with capital now cut off in a “round two” of what had plagued the second half of this decade for the energy sector, only a freak event could make things even worse.

Did someone say “pandemic”?

We enter 2020 with a reasonably self-repaired U.S. energy sector in a healthy position for production, the most substantial improvements in environmental metrics ever, and capital ratios that were vastly improved from five years prior. But the industry entered 2020 in a worse PR situation than it seems even Harvey Weinstein was in and with very limited access to capital at the traditional and advantaged costs that public markets provided. Non-bank investors and lenders were at the table (thank God for private equity!), but this cost of capital did not and could not come without a premium (market efficiency is what it is).

And then, COVID.

And then, the governmental response to COVID.

Supply was running too high. Capital costs were running too high. And now demand would be running too low, which may be the biggest understatement of all time. As cosmopolitan metropolitans ordered up their favorite DoorDash meal and bore down for a long Zoom and Wine night with their gal pals (or guy pals), demand for energy collapsed around the globe.

Surely, this was the death knell for the oil and gas industry.

Oh, and then …

I mentioned a lot of the governance improvements and additional projects that came to market in 2017-2019. Despite two phases of capital constraints that weighed heavily on the industry during the years of the Trump administration, one offsetting source of optimism was a favorable administration that sought deregulation, American energy independence, and a policy bias towards increased production and market share.

Yet after the famine years of capital and then the COVID storm, even that would be taken away as the election results delivered the White House and even slight Congressional majorities to those who advocated for less friendly energy policies. The pessimism was in fifth gear, the pedal was to the metal in doom and gloom, and the sector was leaking badly (I love doing this).

So how has this happened?

With economic, cultural, medical, political, and social headwinds too vast to unpack any more than I have, somehow the U.S. energy industry has proven to be an incredibly investible place. And one of the foremost reasons is, well, that it had become so uninvestable.

What many of the activists will never realize is that the censorship of capital being advocated on the fossil industry drives up the expected rate of return (the hurdle rate some require to enter the fray). And capital is not always as irrational as the shiny object era may lead some to believe. At some point, the opportunity cost of NOT investing in energy becomes too much to bear.

And what happened at the end of 2020 is that the entry-level was too low and the upside too high to stay away. Those brave warriors who dared to buy an integrated oil and gas company instead of a company that “makes an app where a teddy bear wrestles with a cat while you take a video of yourself dancing and can chat with your friends by typing” were handsomely rewarded.

2022 and Beyond

The story is not over. Some of us who care about carbon emissions recognize that other nations do not have the improving environmental metrics we do. Natural gas is expensive in Europe and Asia but vitally needed to provide heat around the world. Advancements towards non-fossil energy sources are not in the stratosphere of meeting demand and suffer from seemingly unsolvable problems of intermittency. American consumers have become exasperated by skyrocketing gas costs and utility bills, and the anti-production crowd has recently become very pro-production – as long as the production is in Saudi Arabia, and not west Texas.

ESG or MIA

My prediction is that the extraordinary alpha generated in a portfolio by NOT owning energy from 2015-2020 is covered by an immutable law of human nature: it is very easy to oppose something you don’t really want anyways. As long as energy investments were under-performing, there was no reason not to create a cottage industry around boycotting their great evil.

But much like the self-fulfilling prophecy of capital access funding growth five years ago, so does the anti-energy ESG world now face a self-fulfilling prophecy reversal. My friends at Strategas Research taught me the mantra – “virtue follows performance.”

I am not suggesting that AOC is about to buy an Oil ETF in her stock portfolio, or that CalPers is going to fund the next great rig procurement in Oklahoma. But I am suggesting that the last six years in the energy space saw it take the most vicious right hooks one can imagine.

And that which doesn’t kill you makes you stronger.

Conclusion

I believe that hedge funds and private equity actors willing to do the scientific, environmental, and economic research have circumvented the cultural and political pressures of the day to the betterment of their investors. But I also believe more mainstream capital will have no choice but to rationally, responsibly, and modestly serve as a capital provider to the energy industry.

I believe demand is robust, and likely to grow, not shrink, for years or decades o come.

I believe the leading operators upstream and downstream are in better fiscal positions than they have ever been.

And I believe some companies have stock prices that warrant a little trimming now. Not elimination. Just a little trim and balance, is all.

The global opportunity in the energy sector is caused by the global need in the energy sector. There is room for reasonable people to disagree about some of the policy solutions. I have a more moderate view than many of my friends on both sides of the aisle do.

But I also believe that the underlying thesis for energy is coherent and sensible and that the largest and most resourced companies in the sector can and will play a vital role in the decades ahead. We would never dare apply any investment standard to energy than we would any other sector. If repeatable cash flows and growing dividend payments and shareholder-friendly stewardship of the balance sheet are not maintained, we are not interested.

That is all we recommend for everyone – the same standard they would apply anywhere. The results of that mentality just might make for a far more rational capital allocation, and keep energy from ever being the worst, or best, performing sector again.

Chart of the Week

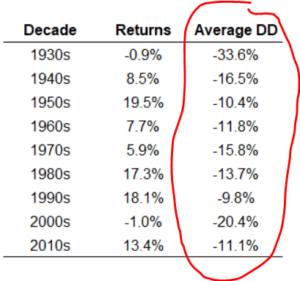

Is the 10% drop in the S&P something to fret about, or is the LOW END of the cost of market returns for a hundred years?

*Wealth of Common Sense, Jan. 25, 2022

Quote of the Week

“There are only two ways to live life. One is as though nothing is a miracle. The other is as though everything is a miracle.”

– Albert Einstein

* * *

I do not see any imminent reason to believe erratic market action goes away, but it certainly could go away at any time. We intend to stay rigorous in our communications with clients and vigorous in our execution of time-tested principles we believe in. Those things give us energy. And to those ends, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet