Dear Valued Clients and Friends,

There is a mixed bag of topics in the Dividend Cafe, but the concluding topic is worth the [very brief] wait.

I know a lot of you are asking me to write about the drama in the Presidential election and its impact on markets, but I really can’t do that yet. It is too early. The Republican candidate (Donald Trump) has not picked his VP (and I think that could move the needle up or down in polling, a lot, depending on what he does). And the Democrat candidate (Joe Biden) is having to convince his own party that he will stay as the nominee. I am doing Zoom events every single day with some of the most inside people on the Beltway, and I promise you that none of them know exactly what is going to happen, either. I am very excited for my “election edition” Dividend Cafe in a couple months, but it has to come after both party conventions. In the meantime, buy popcorn.

I will tease up today’s Dividend Cafe by saying this … It has been a very interesting year so far in markets, for all the reasons I have been writing about. This week had a very interesting event (see below). And long term, there is a wish list of things I want to see (make that, we all want to see!). This week’s Dividend Cafe goes into all of the above. Jump on in, to the Dividend Cafe!

|

Subscribe on |

History as your guide

The top heaviness of markets has been discussed ad nauseum this year, but here is a stat that ought to give pause to those doing the cap-weighted index thing … Q2 of 2024 saw the biggest outperformance of the cap-weighted S&P 500 vs. the even-weighted S&P 500 since … Q1 of 2000. You know, the quarter that gave way to March 2000.

The gap between the two indexes that literally hold the exact same stocks is 11% year-to-date—owning the S&P 500 weighted to each company’s market capitalization is up 11% more than owning the same S&P 500 evenly weighted to each company. That 11% delta is in just six months, and it is stunning.

But Thursday?

I do not do the do the thing of answering whether or not one day means this or means that, because, of course, no one has any idea. Reversals sometimes come with a bang, sometimes with a whimper, and sometimes a bang that bangs right back the other way. So all I can tell you about what happened Thursday is, well, what happened Thursday. But it was wild …

Take most of the “losers” of 2024 so far (or at least relative laggards), and look at what they did: Regional Banks +4.2%, Small Caps +3.6%, REIT’s +2.9%, the Yen +1.8%, long duration bonds +1.4%. And then look at the “winners” of 2024 – semiconductors down -3.3% in a day, Tesla down over -8%, Nvidia down nearly -6%, Big tech down -3%, Nasdaq down -2.2%, large cap growth down -2.1%, etc.

Small cap outperforming the Nasdaq by 5% on a single day has never happened in history.

I reiterate – it means nothing predictive. To try and do so would be silly, as I have read somewhere before. Some may believe the market trend of nothing really going that much higher, but semiconductors and AI-adjacent companies continue. Some may believe that big cap growth “stuff” rolls over but a rotation into other elements of the market takes place with a new leadership mantle. And others may believe it will all roll over. All I can do is look at valuations and history. A leadership transition is far more common than options 1 or 3.

Be careful what you wish for

One of the strangest theories out there is that, with rate cuts coming, the market is about to take off … Look, maybe it is. Maybe the Fed will cut rates from 5.5% to 5%, and some huge hedge funds will say, “Whoa – we didn’t see that one coming! Let’s check out the Nvidia thing” … Stranger things have happened.

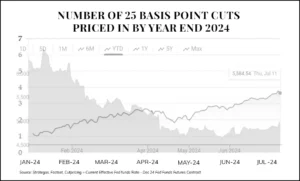

But here is what the market was expecting in rate cuts at the beginning of the year up through where we are now – from six cuts totaling 150-175 basis points, down to two cuts totaling 50 basis points. And here, on top of that in the dark-gray line, is how the market has done through that reduced expectation of rate cuts.

I mean, if I had just come down from Mars and looked at this chart, I might even be tempted to think the markets don’t want rate cuts.

That said, Fed

Of course, fed rate policies matter even outside of what the impact may be to the stock market. A case in point would be, wait for it, those who borrow money on a short-term, floating-rate basis. And they may be happy to know that the futures market is now pricing in about a 94% chance of an initial cut in the September meeting. If that isn’t high enough, the odds are 99% by November, and 100% by December.

Have you heard this song before?

So, China has been suffering through an economic adjustment. As is always the case in a downturn, the money supply comes down as loan demand drops (in this case, loan demand has dropped due to decreased confidence from would-be borrowers and tighter lending in these constrained conditions). Less business activity puts more downward pressure on corporate profits, and fewer profits beget worse economic conditions.

Profits and money supply are lower in China because economic conditions have worsened. China’s option is to “Japanify” out of the situation by manipulating money supply and the cost of credit and economic activity via fiscal policy OR to stop digging in the ditch, take the hangover that is a business cycle profession, and live to fight another day, stronger than they were before.

Other growth woes

The public stock market of Germany, all 57 companies in the MSCI German Index, is equal to half of Apple’s value. They collectively generate 110% of Apple’s free cash flow—110% of the free cash flow, 50% of the value. How does this happen?

Over the mountains a bit, Switzerland’s MSCI Swiss Index – 45 companies – is worth 60% of that of Apple – yet generates 10% LESS free cash flow than Apple does. 60% of the value, 90% of the free cash flow. How is Switzerland trading at over 17x earnings (roughly in line with averages) while Germany trades at less than 12x earnings?

Here is a theory … Switzerland has the sixth highest GDP per capita in the world, while Germany barely makes the top 30 (27th place, to be precise). And how has this come to be? Could it be that Switzerland has 38% governmental debt-to-GDP, while Germany has 64% debt-to-GDP? Valuation comes from growth expectations. Growth comes from economic activity. Debt represents a drain on future economic activity. And these various anecdotes in the preceding paragraphs all weave together some crucial stories.

h/t Alexander Ineichen

Above average forever?

Can a return stay above average forever? I wish I didn’t have to ask this question.

Only by holding in place what is considered “average.” Over time, if a return is “above average” long enough, the “average” has to change, and then it is, well, not “above average.” But how do we get the math of an “average”? We get it with certain periods being above average and other periods being below average.

So two things must be understood here, and they are not that complicated when you think about it, but rarely do investors think about it: (1) The average is always changing; (2) Returns always, always, always revert to their average, eventually.

Now you know.

Got me thinking

I read Louie Gave at the institutional research firm Gavekal diligently. I very often agree or am persuaded by his point of view, and even when I am not, I am always challenged. He wrote a piece a few weeks ago about innovation that I thought was stellar. Essentially, he rooted it in a couple of tautologies that can never be repeated enough: (1) A higher standard of living comes from economic growth, and (2) Economic growth comes from population growth, productivity growth, or both. Simple enough. He pointed out that with population growth at zero (or negative) in almost the entire developed world, the burden on innovation has gotten higher (and as I point out all the time in the Dividend Cafe, the burden is greater by the cost of government indebtedness).

But aside from avoiding the great impediments to economic growth (i.e. excessive indebtedness, high marginal tax rates, burdensome regulation, etc.), what are the things that help facilitate innovation? Louie suggested the list must include:

- Education (though a caveat is important – all innovative societies have a top-tier university system, but not all societies with a top-tier university system are innovative)

- Rule of law (again, necessary but not sufficient, and often graded on a curve)

- A strong military capacity (you can say correlation and causation are not one and the same, and that is true, but the U.S., Israel, South Korea, and Taiwan sure have a lot of correlation to throw around)

- Entrepreneurialism (Louie called this “acceptance of failure,” but I think the two are one and the same)

- Ecosystems – in short, network effects

One item Louie did not mention but I imagine he would agree as a sine qua non of innovation – capital formation. Societies that trash capital markets end up with trash economies. The innovation of capital markets is a surefire foreshadowing of innovation in the production of goods and services.

At the end of the day, the sequence of thought here is not too complicated – a higher standard of living is borne of economic growth, and economic growth is borne from population and productivity increase. Population growth comes from fertility and immigration, and the West is down on both these days. Productivity is hurt by impediments, the most violent of which is excessive government indebtedness that misallocates resources in society. Productivity is aided by the six factors above.

Do with that what you wish.

Chart of the Week

Did someone say top-heavy? 78% of the stocks in the S&P 500 are performing less than that of the S&P 500, an all-time high.

Quote of the Week

“All of us would be better investors if we just made fewer decisions.”

~ Daniel Kahneman

* * *

I think I will have another Dividend Cafe of the “multi-topic” variety next week as I see my research and inspiration pile is still about twenty pieces deep right now. I do have a slew of “single topic” Dividend Cafes coming, including one on all things crypto (this one will not be popular with some), a new perspective on the systemic risk of private credit, a refresher on public debt, a synopsis of MMT (modern monetary theory), and even one on the real lesson of Blockbuster Video. All that to say, some fun ones are coming.

Have a splendid summer weekend, use your A/C, and reach out any time with any questions you may have. The Palm Beach office is being installed next week! We cannot wait to be coming to Florida …

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet