Dear Valued Clients and Friends,

The market hit an expected roller-coaster this week as all the buzz is around the coronavirus in China. Each day this week but one had up or down movements in the triple digit range. So as predicted, volatility has elevated from near nothing to this present week’s level. Earnings season got much more real. The media launched a full campaign. And we have much to say about all of it.

So jump on in to this week’s Dividend Cafe, and you will get a full refresher around coronavirus, earnings season, China, emerging markets, venture capital, pharmaceuticals, and one other thing – the most important thing we care about right now. All that and more at the Dividend Cafe!

All things Coronavirus

The death toll in China can’t be minimized from a human standpoint, and obviously, this is a human tragedy and source of sadness and mourning for those afflicted.

As a market story, it remains one of elevated volatility over fundamental deterioration. The long reported incubation period of the disease before those infected show signs adds to the volatility, giving rise to the unknown (markets hate unknowns).

But in fairness to Mr. Market, the Dow was up a stunning 3,000 points in just over three months – it hardly needs an excuse to see volatility elevated. The thing for investors to really focus on who have longer than a two-week time horizon is earnings season. The coronavirus will not validate or invalidate the present market multiple; it will just elevate volatility due to the embedded uncertainty of things. But earnings season – both reported earnings and forward guidance – tells us volumes about market direction on a company by company basis.

We are in the heart of that earnings season now and will be for the next week and change.

Putting it into context

The ground zero of coronavirus being China adds significantly to market response around this. Investors are conditioned to believe either that China is about to take over the universe, or that its entire empire is a Lehman fraud about to fall down. The media, of course, has no interest at all in normalizing or moderating the story. A health scare is as good a story as the press can get for maximizing fear, clicks, and anxiety. This is not to say the story should not be covered, or does not contain legitimate fears within it … it is to say that the motivations and the methodologies of those doing the coverage matter.

China was accused in 2003 of trying to cover up SARS – of not doing enough. They now are trying to quarantine a community with the population of Italy. Their overall reaction here is the polar opposite to what transpired 16+ years ago.

I read over 500 pages of analysis on the exposure this week, with an even balance of medical coverage and economic coverage. It is a reasonable conclusion that economic impact is more about the temporal period of China travel reduction and perhaps trade reduction than the actual macro-health risk, which is reasonable to believe will prove contained. This will take a reasonably extended period of time before it cuts into industrial production or actually generates a business cycle impact.

So direct exposure to Chinese tourism may prove problematic (and I would argue that was true before this health issue), but the majority of economic impact has a transitory nature to it, and is less significant as one’s direct exposure to China is lessened.

Was the initial sell-off all about Coronavirus?

Of course it was, all the headlines say so, right? The clicks, the special bulletins, the special reports – everyone knows it.

But what if, just what if, it wasn’t? What if after a 3,000+ point market rally in a short period of time, the markets have hit a “wall of worry,” and reflationary trades are long in the tooth, and questions are starting to be asked about how long Fed liquidity programs will last, and the realities of the Democratic primary are being kicked around, and so forth and so on?

Let me ask it this way – what if there was no coronavirus scare, and the market had a couple down days in late January after a 3%+ month, after a Q4 of 2019 for the ages? Would not any one of the aforementioned issues be perfectly logical explanations for the exact same market behavior? Now, I am quite certain coronavirus is in the middle of the real-time market sentiment/volatility issues from earlier in the week. But my point is that we err when we assume markets act in isolation, or that the only thing moving markets (or capable of moving markets) is the most dramatic story available (the one the press runs with).

“Left tail” risk – the low probability/high magnitude events that can be quite disruptive to markets – have plenty of guests at their party, always. From Bernie Sanders to coronavirus to fear of Fed shock to global slowdown – never assume the “left tail” party only has one guest.

And just so we are clear …

A lot of information was flowing down the pike about coronavirus the last week or two. Some of it was accurate; some of it was not. I have written above about the historical non-wisdom in acting on reports of health scares, etc. But even apart from that lesson – and the precedent for market action throughout periods like this, is it okay if I use this opportunity to make another point?

What information does an investor believe they had that millions of other people did not have? What insight might have been unique to just you or a small group of enlightened investors? And if millions of other people knew the same information ahead of you or at the same time as you, what trading advantage might you have had in trying to sell out of the market at that time? Now, this is actually not about coronavirus, per se. It is about the reality of markets in 2020. Information edge is not available to you any longer, so to react to information without an edge, you become the crowd. Maybe that works out. Maybe not. But we need to acknowledge that joining the crowd has not historically ended well.

What we do

Our equity investment is constantly focused on the most important question an investor can ever ask about their ownership of a company:

Is this above-average dividend sustainable, and will it continue to grow?

The crowd is not asking this [compound] question. There is an edge in this approach. You do possess an advantage here as you replace the noise with fundamentals, and momentum with reality. The focus is on the very point of investing – the return of cash to you, the shareholder. And it is an answerable question that transcends the highly transitory events most investors waste their lives and money trying to answer, ones that don’t have answers no matter how much they pursue such.

And then there’s that other thing …

There is uncertainty around where things may go from here, and it certainly seems prudent to assume there will be an impact to at least Chinese economic strength in Q1. Yet it bears mentioning that these realities are exactly why we do asset allocation to begin with. The desire to “smooth the ride” a bit is the entire purpose of fixed income and alternatives inclusion in one’s portfolio. Bond yields did drop this week (adding to the price level of client bond portfolios), providing that zig/zag expectation with fixed income in your asset allocation.

So yes, our exclusive focus is on the strength and sustainability of dividend growth in our portfolio equities. But that takes place within the context of an asset allocation framework, and this is the reason why.

Well, what is earnings season telling us??

Really, it has been an extremely mixed bag so far, with some real bloodbaths and some real rallies out there. As I am reaching press time just as another 10% of S&P 500 companies are about to report, let’s elaborate on numbers Quarter-to-Date next week!

The crucial question – this week’s economic tutorial

I think the most important conundrum for investors to solve right now is not whether or not growth can be sustained by just increasing leverage … the answer is no, and everyone knows it. The question is how much of current growth is, in fact, the by-product of rising leverage, and how much is organic and healthy.

Perma-bears do something that really frustrates an honest advisor like me – and it frustrates me as much for the partially accurate implications in it as the blatantly dishonest ones … They make claims that no one would disagree with – the Fed has played a huge portion in reflating the economy; leverage has increased because the Fed has made it impossible for it not to; bad consequences await if they shut down the credit pumps they have made the economy dependent on … All of these facts are true, but then invite non-sequiturs for perma-bears – they do not know how much of current economic growth is dependent on Fed activity, they do not know when or how the Fed will alter the landscape, and they do not know what other facts will enter the fray that further color the future situation. In other words, they do not know what they do not know.

Their peculiar way of drawing conclusions out of certain premises and atrocious track record in all of the above do not change this fact: The Fed has taken on a hugely different role in the American economy than they have ever had before, and their interventions carry two attributes:

(1) People love it when they intervene to assist markets

(2) Unwinding interventions becomes difficult if not impossible, because that is the nature of monetary distortions

It is this second one that people must understand. We have a highly accommodative monetary policy right now because we used to have a highly accommodative monetary policy, and getting off of it creates pain that the powers that be would rather delay or defer. But delay and defer is not the same as avoid or avert.

Still here and not forgotten

We are accustomed to thinking of all market events as risk-on/risk-off – for example, the U.S./China trade issues of 2019 were always thought of in binary terms – either “something good” is happening, boosting market sentiment; or “something bad” is happening, diminishing market optimism. The completion of phase one stymies this binary thinking, because we are no longer “reacting” to a market story or news event or rumor or hope or forecast – we are now living in the aftermath of an actually complicated set of circumstances, but we are doing so free of the limitations of binary risk-on/risk-off assessment.

We are not de-coupling from China – they need us economically, and we need them. One country’s economic struggles will continue to mean exported struggle to the other country, and the rest of the world, for that matter. Greater access to Chinese financial markets by U.S. companies increases those shared exposures. National security interests are a bigger issue now in sensitive transactions, which advances American interests. And the trade restrictions of the new paradigm are being implemented in China without the blame being put on Xi Jinping.

All elements of life post-phase one must be monitored for their geopolitical significance and actual absorption into the global economy. The “risk-on/risk-off” reactions of last year are now in the past. It is time for more thoughtful analysis of the new guard.

Big Pharma – Keep the left close and the right closer

President Trump is highly likely to impose by executive order an International Pricing Index on drug prices – soon. This is a popular mechanism in Europe, and essentially brings price controls into the Medicare program. Such a move is probably positive for the President politically, but not positive for the drug sector itself. An announcement is more likely than actual implementation in 2020, hence the benign response in the drug sector’s stock prices. The market almost seems to feel the change is coming in Part B of Medicare, but not part D (the far larger exposure for drug sales).

If you are wondering why one would own drug companies with this uncertainty lingering, the market has fully known some sort of price distortive intervention was likely for 3-4 years now …

Venturing into reality

The world of private equity needs to be continually differentiated from private equity, as not all pre-public or non-public equity is equal. But there is another difference as well … While both categories involve illiquid exposure to equity risk (and reward), VC has traditionally aimed for massive gains in a small % of companies invested in to offset the complete loss of capital in a large number of companies invested in … But merely receiving funding in the Venture Capital world has traditionally been a perceived sign of value. Not any longer. Embryonic ideas still need (and have access to) strategic capital, but the maturation of the venture capital space has made it an easier place for managers to make money and a more difficult place for investors to make money.

Private equity, on the other hand, with its focus on a more mature stage of a company’s life cycle, scales better. The risk/reward dynamic is just different. The high asymmetrical risk/reward opportunity set of VC (by definition) cannot be scaled the same way …

We are living in a period of history where financial markets are changing in a number of ways. There are many reasons why public markets are less attractive to successful, talented entrepreneurs. What hasn’t changed is the need for capital to fund innovation and tomorrow’s great companies. What hasn’t changed is the benefits that talented moneyed outfits can bring to entrepreneurs in strategy and networking. But the capital structure and realities of opportunity in large pools of capital has changed. Investors must be focused on what is best for them, not what merely sounds most exciting.

Economic report card

Q4 GDP numbers were released this week, with many “whispers” circulating that the number would print as low as 1.5% real GDP growth in Q4 … Well, the number came in at 2.1%, just a tad below our 2.2% expectation and way higher than the doom & gloom projections from the recessionistas. The growth rate has been 2.4%, 2.9%, and 2.3% (net of inflation) in the last three calendar years (averaging 2.53% per year, a huge move higher vs. the prior trend). It is our estimate at TBG that the trade war took a half point off GDP growth in 2019.

Getting thirsty?

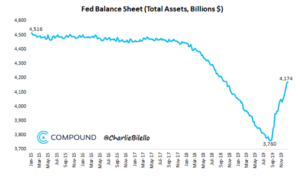

Is the Fed’s balance sheet again suggesting a tightening of liquidity in the economy? Not at all. There was a dip in the balance sheet this month, but the Fed’s intentions of being hyper-accommodative are going nowhere. Interest rates were expectedly held flat this week. The implied expectations for inflation have actually dropped this month.

I don’t want to get you too into the weeds, but the apparent reduction in the Fed balance sheet is because repo volume has fallen off substantially, even as the Fed replaces with t-bill purchases. Repos were and are always temporary liquidity – whereas t-bills are permanent liquidity. So there is a part of this that is in flux day by day and week by week, but what is clear is that the Fed is determined to boost liquidity in a sustainable way (the more permanent liquidity they put on their balance sheet via t-bill purchases, the more they erode demand for repos, which eventually weens that component of balance sheet volatility out of the picture).

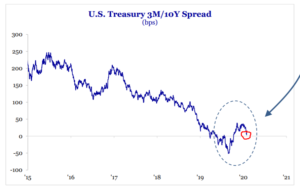

Inverting your prediction

I remain in the camp that the Fed will sit on its hands all year, and the risk to Fed tightening is very minimal … But the idea that the Fed will cut, while unexpected in many ways, is not out of the question. With the 3-month/10-year treasury yield curve falling back to near inversion, it is not out of the question that the Fed may choose to reduce the short end of the curve even further. Let the string-pushing continue …

* Strategas Research, Economics Report, Jan. 29, 2020, p. 2

Politics & Money: Beltway Bulls and Bears

- I think all anyone in the beltway is talking about this week is the impeachment trial, but we ought to mention that the USMCA deal (NAFTA 2.0) was signed, sealed, and delivered this week. It is a significant legislative feat, and frankly, these days any legislation getting signed is significant.

Chart of the Week

I cannot emphasize enough the profundity of what we know about the Fed (and all central banks) in this current time … Easy money is a default monetary policy – it is not reserved for crises or recessions. The deflationary realities that made this true are the subject of many a Dividend Cafe …

* Compound Advisors, Year in Charts, Charlie Bilello, Jan. 5, 2020

Quote of the Week

“Micromanaging is underrated.”

~ Michael Eisner

* * *

Please do check out the press release we sent yesterday regarding our new and improved New York office and not one, not two, but three new hires there. Very exciting times at our company!

As for the week ahead, earnings and virus talk will likely dominate market sentiment. I have no forecast of which way it goes. January is now behind us. Reach out with any questions any time. Iowa caucus, here we come …

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet