Dear Valued Clients and Friends,

It really was a historical event that took place last Saturday night. The U.S. operation, “Midnight Hammer,” was executed last weekend, and once all partisanship is removed from the assessment, the scope and success of the operation are pretty remarkable. I understand there is still some ambiguity as to the exact calculations around setback to Iranian nuclear progress and so forth, but there is just a lot to the operation that, if nothing else, logistically, is pretty amazing to behold for a mere finance guy like me.

My priority in the Dividend Cafe today is not political (for which I will put my bona fides to be objective and either critical or complimentary as situations warrant up against anyone), and nor is it militarily strategic (where like 99.9999% of all other people, I am unqualified to speak). Rather, I believe this warrants a really serious look at markets, at what has transpired in recent weeks, and where we find ourselves now with one of the most important considerations of risk premium on planet earth: Middle East uncertainty.

This is a topic we ignore to our own peril, and I believe today’s Dividend Cafe will, all at once, provide a little history, a little context, and more than a little shock and awe. It just won’t be the type of shock and awe that you might expect, or that a B-2 bomber delivers.

Let’s jump into the Dividend Cafe!

|

Subscribe on |

When knowing the future doesn’t help

I want you to pretend for a moment that you can pretend we are sitting somewhere in the past, say, two weeks ago, and I said to you, “I have a crystal ball, and tomorrow Israel is going to attack Iran.”

You say to me, “Your crystal ball is wrong; President Trump is close to a deal with Iran, and he has made clear he doesn’t want an attack now, and Bibi would not do this without American support.”

And then I say, “well, my crystal ball is not wrong, and the attack is coming, tomorrow, and it is going to kill the top generals in Iran, and their top nuclear scientists, and represent hundreds upon hundreds of missile and rocket attacks into Iran, all the while Iran is going to swear up and down they will annihilate Israel in response.”

And you say, “Well, as long as the U.S. stays out of it, then maybe we can avoid a big market disruption out of it.”

And I say, “Well, you won’t believe what else the crystal ball tells me, but actually, the U.S. is going to jump in, in a big way, dropping 14 bunker-buster bombs on Iran’s nuclear facilities from B-2 stealth bombers that would fly all the way from the United States.”

And then you say, “Well, that sounds like it could escalate into a major war. Surely oil will spike, and I can see Russia and/or China getting involved on Iran’s side, and this could spiral quickly.”

And then I say, “Funny you should say that – because a lot of the President’s own supporters will turn on him over this, and the rhetoric is going to turn up a lot, and my crystal ball says there will be retaliatory attacks, and then talk of a ceasefire, and then talk of a broken cease-fire, and talk of regime change, and all sorts of heightened uncertainty. And this is all going down in just days.”

Now, you may think I am crazy to be talking to you this way, about a crystal ball and such, even apart from what it is I am saying that the crystal ball is suggesting. But what if we add on this for good measure:

“As I am talking to you, the Dow is at 42,198. Israel has not yet attacked. Iran has not yet retaliated. The U.S. has not yet conducted its historical strike. None of these things has yet escalated. And two weeks from today, the Dow is going to be …”

You interrupt me to say, “below 40,000 – maybe worse?”

And I say, “Oh no, actually, 43,386, up +3% in these two weeks.”

And you say, “Yes, you are crazy.”

Then I say, “Oh, oil is $68 right now, right?”

And you say, “Yes, it is. And if Israel attacks Iran, and Iran launches counterattacks, re-groups, the U.S. attacks as you say, and Iran plots its next move, oil will be at $80 – if we are lucky, maybe $90 if they cut off the Strait of Hormuz.”

And I then say, “Well, my crystal ball is sort of laughing right now, because oil did get off of $68 after Israel attacks Iran, and hit $75 for one day, but in two weeks after all these attacks, it will be at $65.”

And you say, “Israel will attack Iran more comprehensively than anything since the shah was overthrown nearly fifty years ago, launching a U.S. attack in support, with talk of a war breaking out, and you think oil is going down?? You are not just crazy, you are certifiable.”

And I say, “uh-huh.”

Unpack this

By now, you get what I am doing. There was no crystal ball, and this conversation never happened, and yet every single thing described absolutely did happen, exactly in the sequence, timeline, and magnitude laid out. Two weeks ago – two weeks – Israel attacked Iran, and one week ago the U.S. got involved bigly, and as I type this morning with just nine market days having transpired (because of one market holiday in between), the Dow is UP +3%, and oil is DOWN over 3%.

I am sure plenty could be said about why this is – Iran’s retaliations were, to say the least, underwhelming. The U.S. action has not yet elicited a response from Iran directed at us. There is global relief that the Iranian capacity for nuclear attack on Israel is diminished to a large degree. Other factors are driving markets, too (i.e., AI capex, confidence in Q2 earnings whose results will begin coming in a couple of weeks, progress in U.S.-China trade talks, increasing optimism about Fed rate cuts, etc.). In other words, markets are, and always have been, and always will be, multi-faceted.

But the multi-causal reality of markets is not the only story here. It isn’t like the story here is, “well, yes, the Israel/Iran issue should have pulled markets down, but then Nvidia pulled it up, so in that tug of war we were up 3%” … The story is that:

- What happened with Israel/U.S/Iran was not remotely predictable

- The aftermath was not remotely predictable

- The market response to the actions themselves was contrary to consensus expectations

- The market response to the aftermath was contrary to consensus expectations

- And oh yes, there are multi-causal drivers of market activity, always

You can take out Iran, Israel, geopolitics, oil, war, and any of the proper nouns and particular adjectives you want. Change the cute little story above with me and my imaginary friend and an even more imaginary crystal ball, and fill in whatever you want, mad lib style. Make it monetary policy. Make it a bad jobs report. Make it a trade war. Make it a trade war reversal. Make it an election. Plug in the wackiest combination of headline trauma you can think of. The assurance of unpredictability out of whatever the hypothetical will not change.

What is sure to be true in any such scenario is that: (a) No one will get the predicted fact patterns right, (b) No one will get the market response to the facts right, and (c) No one will get the timing of it right.

The only other assurance is that (a) A whole bunch of people will try. My condolences to them and theirs.

Who could have seen it coming that we couldn’t see it coming?

I got an email in early April that “it was obvious” the markets were going to crash after President Trump was elected (they went up thousands of points), and that “it was obvious he was going to launch a trade war” (he reversed course four days after announcing it in response to market action) and that “it was obvious markets would go a lot lower with the path he was taking us on and that stocks were going to crash much more” (they are up 20% since I got that email).

Truth be told, my biggest fear is that the guy who sent that email is now buying stocks! But I digress.

No one should ever feel bad about being wrong. They should only feel bad for ever saying the words “it is obvious” when it comes to financial markets. It does not take a long time doing this professionally to find out that nothing is ever obvious. Humility is necessary for success in this business, but it is also guaranteed to come for those with enough staying power, regardless.

My point is not that markets may not go down (or up) with this President, or any other President. My point is not that a trade war will come back to the surface (or that it won’t). My point is not that markets will drop in response to the next tweet of this unconventional President (or that they will). My point is that I do not know, and I assure you that you do not either. And if you did, you would not be emailing me (or at least you shouldn’t be).

In one calendar quarter (less, actually), we have seen the most insane public policy announcement I have seen in years (“Liberation Day”), a massive market collapse from such, a complete policy reversal, a massive market reversal, an Israel-Iran flare-up that appears to have lasted twelve days (for now), an oil spike, an oil drop, and a graveyard of failed predictions along the way.

I guess 85 days is pretty short for this many opportunities at humility. But other than that, it is all par for the course, as they say.

Is peace breaking out in the Middle East?

One of the more important Dividend Cafes I feel that I have written in the last several years was the initial Dividend Cafe after the Hamas atrocity of October 7, 2023. I used that commentary to highlight the history of geopolitical tensions in the Middle East and their impact (or non-impact) on markets over time.

I am reasonably optimistic about what we seem to have accomplished with the strikes last weekend, at least to the degree that I can form any opinion. But what you are not going to hear from me, and ought not listen to from anyone else, is that “peace is now assured throughout all of the Middle East.” If Iran’s nuclear threat is significantly diminished, then yes, that is one threat that has been marginalized. But to assert that the entire Middle East region is now somehow a pasture of peace and tranquility is, well, the dumbest thing I have ever heard in my life.

I encourage you to re-read the aforementioned Dividend Cafe. If anyone believes that the religious, geopolitical, ethnic, and historical conflicts of that entire region are all in the rearview mirror, then be my guest. I have a bridge to sell you in Syria. But as you may want to consider from that piece, as an investor, does the persistence of a risk premium in the Middle East matter to you? They attacked our own country, and markets are up 500% since then. I am in the same boat as everyone else when it comes to the year-by-year reality of that region, in that I do not know what attacks are forthcoming, what response to those attacks will be, or what market impact will result. There is a long-standing precedent of enhanced market volatility in the immediate aftermath of severe Middle East drama, and there is a long precedent of markets recovering after such drama (sometimes in months, other times in days). If you want to study the last two weeks, or two years, or two decades, or two centuries, and come up with any other conclusions than these about how Middle East disruptions should impact a U.S. investor’s plan, please advise:

- The Middle East has a high probability of remaining a hotbed of geopolitical tension, uncertainty, and risk, AND

- U.S. investors in anticipation of and response to such ought to do … nothing

What are we doing in Iran?

So with that said, allow me to share the three strategic objectives of the U.S. action in Iran as expressed by the brilliant René Aninao of Corbu:

- To re-establish credible military deterrence and the perception of U.S. escalation dominance

- To introduce a newly expanded US commitment to the enforcement of the global non-proliferation regime

- To demonstrate [on the eve of the NATO Summit and conflict resolution negotiations with Putin] the operational superiority — and precision global reach — of the U.S. military in coordination with its non-treaty allies to achieve desired effects

The geopolitics of what we just did in Iran transcends what we just did in Iran.

Some of you may remember the “Bush doctrine,” whereby it was determined after 9/11 that “any country that hosts, facilitates, and supports rogue actors who plan or enact harm on the United States will be treated as a country that enacts harm on the United States.” Regardless of the way in which things ended up being done in Afghanistan and later Iraq, the purpose of this so-called doctrine was to deal with the new reality Al-Qaida made clear on 9/11 – that foreign threats were no longer only relevant if they came from another nation-state … Terror cells being coddled inside a country were a potent threat in modern times, and therefore their host countries needed to stop being host countries.

I would suggest that the so-called “Trump doctrine” is also relevant in the ongoing evolution of modern foreign policy. “If you do not currently have a nuclear weapon, and we do not believe you should have a nuclear weapon, you are not going to have a nuclear weapon.” This “doctrine” may fall short of comprehensive foreign policy, and it may be inadequately hawkish for some, and may be excessively hawkish for others, but it does seem to be a new doctrine for markets to appropriately discount: Non-proliferation is a major priority, and it will be pursued without American troops on the ground.

Next Steps

My expectation for what comes next in the Middle East is that I have no idea whatsoever. I expect some who hate the President and lack the capacity for objectivity to claim the mission was a failure. I expect some who are guilty of the exact same delusions in the exact inverse to claim that the mission accomplished permanent peace on earth. And I pay no attention to either of these extremes, just as markets pay no attention to them. The current lay of the land may prove to be the best case – a quiet Iran that licks its wounds and fails to respond witch much force (either out of capacity restraints or strategic patience), a severely damaged nuclear capability for Iran, a ceasefire between Iran and Israel, and a successful messaging to other rogue actors of U.S. seriousness in this regard. But of course, some of these things may take a step backward in hours, or days, or months. It is not known to anyone who will dare to be talking about it, and is likely not known to anyone who is not talking about it, either.

What I do know is that the administration’s tolerance for a prolonged and expensive war involving U.S. ground troops is about the same as the public’s appetite for such: Zilch. Is that left tail risk out there? I mean, I suppose it is, way, way out there. But is it something that looms as a serious market discussion point right now? No, it does not.

How to “play it”?

Media outlets reach out to me a lot, asking how “I am playing” such-and-such an event. My answer to them is always the same, and I think you will find it pretty consistent in what I say to clients (and readers):

I am not “playing” anything. There is no “play” around Israel-Iran. There is no “play” around macroeconomic event A or geopolitical event B. Some companies may get cheaper or more expensive in response to certain events, but seeking a “play” in the way big events effect the dollar, or stocks, or this, or that, is just the kind of thing someone ought to do if they want to get to get run over by a truck.

And my “play” on getting run over by a truck is to avoid standing in front of trucks.

Dividend growth is not a play. The companies we own as dividend growth investors are not plays. Dividend growth is an investment philosophy that we believe has offensive and defensive characteristics that make it a vastly superior way to own public equities than any other strategy of equity investing. Some events happen that make the dividend reinvestment of a certain company better than others. Other events happen that make investors glad they own a company. Diversification underlies dividend growth to mitigate the risk of being wrong and to spread out the probabilities of what happens within a portfolio of companies. But in any period you can ever talk to me about, past, present, and future, we are not “playing” with client money. We are doing what we believe in philosophically to achieve the right outcomes. To that end, we work.

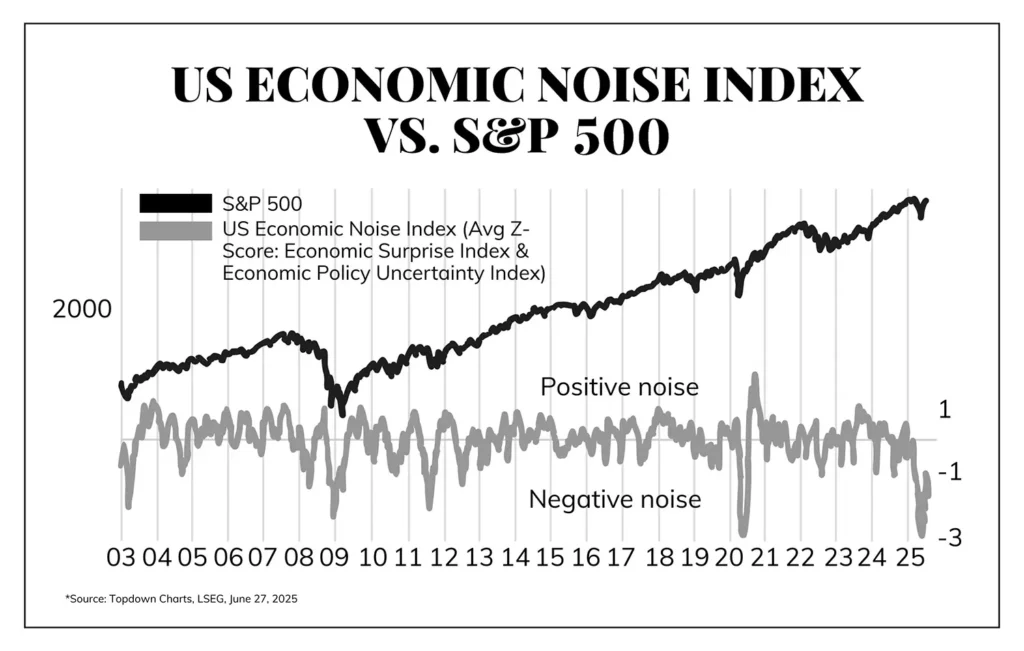

Chart of the Week

So much “noise,” so little reason to care.

Quote of the Week

“Anything that happens, happens. Anything that, in happening, causes something else to happen causes something else to happen. Anything that, in happening, causes itself to happen happens again. It doesn’t necessarily have to happen in that order, though.”

~Douglas Adams

* * *

It was a scorcher in much of the country earlier this week, and we now get ready for hot June to move into July. Whether we are talking about markets or weather, the beat goes on, and next week we will welcome in the second half of 2025. Enjoy your weekends, stay cool, and while you are at it, stay free. And reach out any time. Our advisors live, sleep, and breathe what is best for our clients. And that is how it should be.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet