Dear Valued Clients and Friends,

I am typing this week’s Dividend Cafe from 30,000 feet very late at night on Thursday night/Friday morning, after spending four and a half hours on the plane, on the runway, alongside 100+ other planes that were unable to take off as airspace was closed for Kamala Harris’ visit to the LA area (campaigning with Gavin Newsom against the recall). My wife and I will land in Nashville in the middle of the night, and we will forget this experience soon (I hope). Anyone who travels a lot has had bad experiences. I travel 50x a year and have been through everything, but as a percentage of the times I fly, I have had it easy over the last 25 years. It’s never fun, but it happens.

But twenty years ago Joleen and I were also flying together, this time departing LAX for a Tahitian honeymoon. As I mentioned the other day Joleen and I celebrated twenty years of marriage this week. On September 10, 2001, we left LAX on a redeye with a planned landing in Tahiti in the early morning. One hour before we landed the most horrific act in American history took place. It is that event that is the subject of today’s Dividend Cafe.

Sure, there are some personal reflections and musings. But there really is a market lesson in all of this, and I hope you will find this to be meaty enough for your normal Dividend Cafe longings. Truth be told, the rather basic message I have to share for investors on this 20th anniversary of 9/11 is more significant in practical terms than any commentary I have ever written about monetary policy or capital allocation.

I will forget the wait of today, but I will never forget 9/11. Let’s jump in.

The landing in Pape’ete seemed to be without incident on the morning of 9/11, but the panicking commotion from other people in line caused me to run to a payphone. My brother-in-law informed me that it looked like a bomb had gone off in NYC, and my grandmother was just plain thrilled to know her favorite grandson and her new granddaughter-in-law were okay. It took at least another hour until clarity on what had happened was available, and by the time we arrived at our resort destination, there was no TV for me to glue myself in front of. There were CNN printouts from the web that they posted at our Moorea paradise, but there was no real access to information, and obviously not a thing in the world anyone could have done if there had been.

Joleen and I had a very memorable honeymoon. We sat down and chatted at some point after a day of pretty severe distress, and made the decision that we were going to enjoy our time no matter what. And we did. But it was a day that neither of us will ever forget, and ironically, the last time we spent four hours stranded on a plane together was the day we were leaving Tahiti at the end of our honeymoon, which ironically was the first day LAX was re-opened for incoming global travel post-9/11. We got home from our honeymoon in the middle of the night, too.

But I digress.

That experience was awful for reasons that really have nothing to do with me or Joleen. We got by. We were safe. We made the decision to enjoy our honeymoon, and we did so. But here’s the thing. Joleen and I love our country very much, and though New York did not mean to us then what it does now, we certainly were well aware of what symbolic message the terrorists were trying to deliver with this attack in the heart of our country’s financial system. Like I assume the vast majority of you, we were angry, scared, and of course, heartbroken for the loss of life.

Joleen worked in marketing at the time for the ad agency that ran all of the marketing for the Hilton Hotel Corporation. I, of course, worked in finance. I would be lying if I said that the thought never crossed my mind that both of these mid-20’s newlyweds were about to be unemployed. The market re-opened a week later and fell thousands of points. I may not need to remind you that it wasn’t like risk assets had been thriving before 9/11. We were 18 months into the 30-month bear market that broke out post-dotcom. People swore no one would ever travel again. Both Warren Buffett and Vice President Cheney said it was inevitable that a nuclear attack would one day happen on U.S. shores. There was pretty indiscriminate panic in markets, a severe slowdown in economic activity, and of course, a gnawing feeling that nothing would ever be the same.

On that last count, before I dive deeper into some market lessons, it does grieve me that so much of that has proven to be wrong. What I mean by that is not that Americans did, in fact, start flying again (in record numbers). That was and is a good thing (just as it is now post-COVID, as doomsdayers and drama queens once again eat their words). I mean that the “return to normalcy” post-9/11 has gone beyond the admirable reclaiming of our lives and freedom, and apparently from where I sit, also invited a sort of amnesia about the nature of those who hate us. I fear our breakdown in vigilance. I regret the willful decision to feign ignorance about the threats we face. And I pray it will never happen again. Like so many other things in a country that has fallen in love with tokenism, “Never Forget” seems to have become a one-day-per-year bumper sticker, at best.

But this is where the market lesson comes from post-9/11, post-GFC (great financial crisis), and post-COVID. Not one of those three events that have so far marked this new and rather unsettling century were foreseeable. And not one was able to disrupt the properly allocated investment plan of a disciplined investor. Not one was hedge-able. Not one was time-able. Not one was avoidable. And yet, not one was fatal (for investors who behaved).

Is that all there is to it? Investor behavior is the primary determinant of investor outcomes.

Yes, pretty much. But I will elaborate a bit more. Like almost every other “this time it’s different moment” in history, 9/11 was traumatic, with significant justification for a re-pricing of risk assets. Would we face a generational war with a non-nation state actor? Would domestic attacks in the U.S. become a normal event? What would it mean to the insurance industry – travel – finance – technology – etc.? What would the economic cost be to New York City itself? The fears, worries, and just plain questions that were on the table post-9/11 would seem unfathomable now, but they were abundantly rational and common then.

The Dow was at 8,000 then. It is at 35,000 now.

The 338% increase notwithstanding, with, you know, that little 50% drop along the way in the Great Financial Crisis, market resilience is more than a statement about corporate profits. It is a statement on the human spirit, and corporate profits are merely the consequence of the human spirit. The indomitable quest for human flourishing, achievement, self-advancement, and betterment has been met with incredible capacity, productivity, technology, and reason. The basis for free enterprise is the miracle of human action and the results it has produced in history. That same miracle creates corporate profits and therefore creates investment opportunity. And that same miracle – that capacity for resilience and achievement – is why we are able to overcome events like 9/11, the financial crisis, and yes, COVID.

That resilience cannot come without setbacks, failures, loss of confidence, periods of panic, and all the rest. The strategy of a long-term investor cannot be dependent on short-term happenstance. The long-term goals of an investor can be aligned with the long-term realities of the human spirit. They cannot be perfectly aligned with the short-term gyrations of markets. Not predictably. Not successfully.

Investors have had ample opportunity to invest out of fear rather than the principles I have described herein since 9/11. It has not done well for them. There are going to be more “investor moments” like the ones I describe above that have taken place in the last twenty years. Before this new century began, before Jo and I were married, before 9/11, there were moments like this, too. Opportunities to abandon a thoughtful, carefully constructed investment plan have always been there.

The investment lesson of 9/11 will last forever, and through many more situations – both good and bad. That lesson is that if one is invested in risk assets, they had better believe in the dynamism of the human spirit that justifies that risk premium. And if they believe in that dynamism, they better not forget it when bad things happen.

This time is never different.

Never forget. And in this context, I do mean two different things.

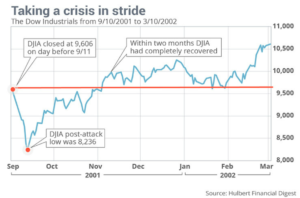

Chart of the Week

Quote of the Week

“America was not built on fear. America was built on courage, on imagination and an unbeatable determination to do the job at hand.”

~ Harry S. Truman

* * *

I don’t have anything else to say this week. I am now safely at my destination and ready to hit “submit.” The hassles of this trip pale in comparison to what real travel issues were twenty years ago, so I don’t have it in me to complain about a little delay. I hope today’s Dividend Cafe serves as an investment reminder about that which really matters,

And I hope this 9/11 weekend serves as a reminder of that moment when so many things changed. And so many things didn’t.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet