Dear Valued Clients and Friends,

I got a lot of feedback on the special “China edition” Dividend Cafe two weeks ago, but I promised a lot more to come on the subject, and that is what we have today. I don’t only want to walk through various perspectives on Chinese investment, but really want to make sense of what much of this means for hemispheric changes taking place in global monetary realities. There is a tremendous investment relevance to all of this, and that will be just as true for anyone who never buys a dollar of Chinese stocks, bonds, or currency. We ignore this topic to our own peril.

It has been a historical week in a lot of ways, and I have written about Afghanistan and its potential impact on American domestic policy throughout the week at The DC Today. We will know more next week about the sausage-making on capitol hill. Market volatility this week was largely Fed-driven and seasonal. I don’t believe the events in Afghanistan this week will be remembered by markets for minutes, but I believe they will be remembered globally for decades.

And globally, we have much to consider if we are to be smart investors. So to that end, we work …

Join me in the Dividend Cafe (where, as a special bonus today, some pretty hardcore facts about dividend growth benefits will be presented).

China continued

As I wrote about two weeks ago, a paradigm shift appears to be playing out in terms of how many U.S. investors feel about investing in Chinese equities. But that is really more the effect of the paradigm shift, not the cause of it. The underlying paradigmatic transformation I believe we are living through is China’s determination to downtick its connectivity to western capital, technology, and social structures. An overwhelming hostility to its own local capitalists is merely a tactic in accomplishing this.

But there is much more playing out than China picking on its billionaire class and whopping stock prices for U.S. investors in Chinese growth companies. The world’s relationship to China is in the midst of a transformation as well. There was tough talk on the trade relationship with China in the Trump administration, and many assumed that the new administration would mean a return to the pre-Trump status quo as it pertains to the nature of the U.S. dynamic with China. But the fact of the matter is that American foreign policy with China has not altered at all the last eight months, trade and tax deals have not changed at all, and there is sort of a political handcuffing that seems likely to keep that policy similarity in place.

Put differently, the politics of a distrusting towards China posture were not good six years ago; the politics of a trusting posture towards China are not good now.

COVID has a lot to do with that. I began writing about this over a year ago when I was fascinated by the shift in polling around public sentiment. I believed then it had to have a political ramification (I was right), but I think I underestimated what it will mean as an economic ramification.

The issue to me is not whether or not there is an investment opportunity in Chinese equities. The issue is that the risk curve in doing so has skewed up. Even as valuations and prices have come down, the risk is enhanced – not the opposite as it should be after a price decline – because their clear and present policy objective is to control their internal affairs at the expense of external stakeholders. So be it, but that can’t happen without impact the risk profile of such investments.

The question that weighs over investors is whether or not the very things that are paradigmatically shifting in the global economy’s relationship to China as it pertains to trade, risk, control, and their stock market, are also things that enhance the opportunity in sovereign debt and currency.

Two to Tango

I know what many Americans believe about China. I know post-COVID what much of the world thinks about China. The distrust more and more of the world has regarding China around COVID, around human rights, around the theft of intellectual property, around Marxian command-control intentions, have expanded not just in the states but in much of the world. I share almost all of it (where I have some disagreement with many on the populist American right is the belief that the entire deindustrialization of much of the rust belt over the last couple of decades is the fault of Chinese exports; but I will save that for another day, or maybe I should say, a previous book).

But when we assess what the economic ramifications from this entire paradigm are, we will arm ourselves better pragmatically if we also consider what their impressions are of us. The Chinese perception of American political and economic intentions and practices may be dead wrong – and in most cases, I think they are – but if I am to correctly assess their next move, I would be wise to firmly grasp what their perceptions are. Again, the accuracy of China’s beliefs about America is somewhat irrelevant here – only that they really believe it and will act on it in their next batch of hegemonic positioning.

And so what is the relevant part of China’s assumptions about American policy? That we cheat because the U.S. dollar is the world’s reserve currency, period. What do I mean by cheat? As economist, Charles Gave puts it (not articulating his view, but articulating his summary of their view):

The implication is that the US benefits from the privilege of settling its current account deficits in its own currency.

This privilege allows the US to live above its means, enjoying the possession of both guns and butter; guns to keep other countries in fear of being bombed should they misbehave, and butter to keep the US population in a comfort that is no longer earned, but acquired by issuing debt which is purchased by client states to pay for their ‘protection’.

We import more than we export, which means, in the most simplistic verbiage possible, that we have to pay the difference. We can buy $20 of widgets from one country, ship them $10 worth, but then have to pay $10 to make up the difference. We can do that with debt. But no matter what, we get to do it with our own currency.

China believes THIS is the great unfairness of the 21st century. Now, they are not stupid. They want to export their stuff to us. And they have been happy to fund our deficits to some degree to do so. They needed dollars. We needed to borrow money. We needed to buy their goods. They needed to sell us their goods. Everyone was happy (well, not everyone, but let me keep this simple).

China is going to protect the flow of capital vigilantly. They cannot change the structural advantage the U.S. has as the world’s reserve currency, but they can avoid a balance of payments crisis where they are at the mercy of another country. This means practically speaking:

- They have to keep a massive surplus of foreign exchange reserves

- They have to keep their currency structurally sound

- They have to find more ways for their flow of capital to be denominated in renminbi, not dollars

And it is that LAST point that I believe is one of the most potentially paradigmatic changes of the next 10-20 years – trade between Asian countries becoming denominated in Asian currencies, less so in dollars, create a decrease in demand for U.S. dollars, ergo, a decline in value.

And with that, an increase in the value of Chinese currency/debt.

More to come

I will be interviewing Louis Gave of Gavekal Research for public consumption on this very topic in the coming days and we will circulate it next week. There are significant implications in everything I am talking about. What if commodity imports are no longer purchased in American dollars (by China)? How did China ever pay for their massive commodity imports with dollars – meaning, where did they get the dollars? Well, they bought our debt and accumulated massive dollar reserves, of course. Their ability (or inability) to decouple commodity purchases from dollar dependency will matter a great deal to commodities and energy as well.

This is not imminent, but I am convinced it is their policy goal.

The renminbi as a stable store of value benefits every single Chinese strategic imperative one can think of.

And all one wants with their “boring bonds” these days is a “store of value” (discussed last week).

The interests of the U.S. investor and the Chinese government are counter-aligned when it comes to their equity growth markets in so many ways and completely aligned when it comes to their bond markets in so many ways.

Looking forward to bringing you next week’s discussion.

A couple other things

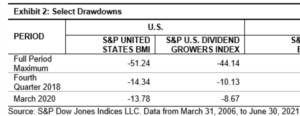

The S&P 500 is the major U.S. equity index that contains a lot of companies across a lot of sectors in the American economy. The good folks at Standard & Poors have been kind enough to create a sub-index of just those companies within the S&P 500 universe who consistently grow their dividend. The defensive characteristics of the dividend growers is readily apparent when measured by drawdowns (peak-to-trough declines).

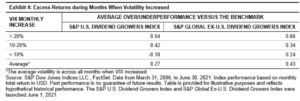

But even apart from this drawdown factor, which I have practically found to be the most significant, the “risk-adjusted returns” (that is, returns adjusted for the volatility taken to get them) have been better for the dividend growers for 3 years, 5 years, 10 years, and 15 years. The upside capture of dividend growers is higher than its downside capture (whereas by definition the total index has an equal upside and downside capture).

And in periods of heightened volatility, the average monthly outperformance elevates. In other words, if you think we are in for a really calm, easy go of it with equities for years to come with substantially decreased levels of volatility vs. historical normalcy, dividend growth may not produce the same enhanced performance benefit. =) But if you believe there will be any normalcy in volatility, let alone enhanced volatility, the defensive benefits are rather astounding to consider.

Chart of the Week

The “oh no, the market is at an all-time high!” concern is perhaps the saddest thing I regularly hear from investors. It is not sad for clients of The Bahnsen Group, because we can immediately explain that every price the market has ever been at prior to today was, once, its “all-time high.” We can explain that valuations should be our focus, not prices. And we can walk through the futility of believing an all-time high is anything predictive whatsoever. The reason this silliness is sad is not for our clients, but for those who hold to the intuitive concern, and don’t have anyone to correct the math and logic of their thinking.

It is the point about all-time highs and their failed predictive prowess that I want to focus on in the Chart of the Week. The S&P 500 was at 1,480 on January 1, 2013. The market made 45 all-time highs that year – in one year – 45 days were the new “all-time high.” We actually have 320 “all-time highs” since then. 320 different days over eight years that the market closed at an all-time high. And the S&P is now at 4,400, not 1,480. Basically, the market has tripled since the faulty logic of all-time highs began being used. Sad indeed.

*A Wealth of Common Sense, All or Nothing Markets, Ben Carlson, August 15, 2021

Quote of the Week

“If you want to be successful, you need to study success, not hate it or be envious of it. If you are envious, then you will distance yourself from success and make it that much harder to get there. Never be jealous. Never think someone is ‘lucky.’ Luck is created by the prepared. Never think that someone is undeserving of the money they have. That only puts you one more step removed from the freedom you aspire to. When someone is envious and jealous, they will never get the freedom they want, but they will spend the rest of their life trying.”

– James Altucher

* * *

May your weekends be filled with back-to-school preparation and air-conditioning, and may your inbox reach out to me if you have any questions at all. The navigation continues.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet