Dear Valued Clients and Friends,

This week’s Dividend Cafe almost seems to delve into what my philosophical approach to solving the drug epidemic may be, but it really isn’t about that. First principles ought to cover one’s approach to a wide array of subjects, but here in the Dividend Cafe, we limit our subjects to areas involving the markets and the economy (no matter how tempted I may be to get distracted at times). This week’s Dividend Cafe keeps its eye on the ball of a truly important fact of human nature, a whole bunch of current circumstances impacting investors, and a few things around government debt and long-term economic growth.

It’s a worthwhile read in this week’s Dividend Cafe. Let’s jump in!

|

Subscribe on |

Supply finds demand

When there is demand for reckless and idiotic products, one never needs to worry about whether or not there will be supply. And the product we are talking about now is the so-called “single stock ETFs.”… Now, you may be as confused as I was (and I have worked in the business 18 hours a day for 25 years and counting) as the general understanding of an ETF is that it is a DIVERSIFIED basket of stocks, either replicating an index of sorts or representing an actively managed portfolio. Isn’t “single stock” and “ETF” an oxymoron, like “jumbo shrimp” or “UCLA football”? (come on now, I am just having fun). And since an ETF is a stock, why would anyone buy an ETF of a single stock when they could just buy the single stock itself? Why, indeed! Because, LEVERAGE, of course. But why not just buy on margin? OH, because in this case, the ETFs exist to speculate (with leverage) FOR A SINGLE DAY. Yep.

Matt Levine of Bloomberg highlighted a case where one of these is down 82% on the year, despite the fact that the stock itself is up over 100%. And the ETF offers 3x the upside!! So what gives? How does something that should be up 3x 100% (if you dropped your calculator, that equals +300%) actually go down -82%? Because the leverage works DAILY and resets each day. Yep, an entire product has been created to give super leverage to what a stock might do on a GIVEN DAY. Yet, that intrinsic leverage falls apart (because of the complexity of re-buying the options that fuel the ETF) beyond a single day.

If I were given a magic wand and told I could fix the drug addiction problem in our culture, I would use my wand to address the DEMAND problem – the fact that people want destructive and often fatal things due to various challenges and holes in their lives. If I used my wand to address the SUPPLY issue and yet the DEMAND was still there, I have no doubt that addicts would move from one unhealthy thing to another – one whose supply was not taken offline by my magic wand. In other words, in real life, there is no magic wand (you may have heard it is hard to eliminate the supply of narcotics), and as long as the demand that comes from loneliness, spiritual isolation, social dysfunction, etc., exists, there will be addiction. We need demand-side cures to drug addiction – those on the spiritual, personal, social, emotional, psychological, medical, and existential side of things.

What does this have to do with single-stock ETFs, and am I not being a little melodramatic? Yes, I am, but it seemed to me a good analogy to make the point. It would be very easy for me to say, “The SEC should ban these products.” They are, after all, an atrocity to all that is good and decent. However, investors have every right to take whatever risks they want in pursuit of whatever rewards they may be after. I believe their ADVISORS have a very serious MORAL and FIDUCIARY duty to only serve their interests and give prudent advice to their clients. But let’s just go out on a limb here and assume that these products are, ummmmm, not being used by fiduciary advisors! Some do-it-yourself investors have a heavy desire to speculate, and what could be more speculative than what a single stock might do on a single day? These products (offering either leverage to the upside OR downside for a single day) may be the dumbest thing I have seen in a long time (or as the brilliant Cliff Asness calls them, a “fresh hell”), but people have a right to “fresh hell.”

I don’t control the supply side of our industry – I can’t eliminate products, and I wouldn’t even if I could. All I can do is focus on the demand side and, even then, only on those who want my advice and counsel. Rank, reckless, absurd speculation is in high demand because human nature is a failed investor. Our value proposition is to contort the demand of investors into the needs of investors – into solutions that satisfy objectives. To that end, we work.

Yield curve history

By now, everyone knows that the U.S. bond market yield curve SEVERELY inverted in early/mid-2022, and here we are in late 2024, and no recession ever came. Now, maybe a recession comes in a year or two, and people will then start saying that the May 2022 yield curve inversion predicted the April 2026 recession, but at that point, you will just have more emails to unsubscribe from.

So I say this with a ton of caveats because what has happened (often, but not always) with the yield curve is clearly NOT predictive, as many learned the hard way the last couple of years. That said, as we prepare for the yield curve’s “un-inversion” (the spread between the 2-year and 10-year treasury yield is now flat after having been as much as 100 basis points wide last year), I thought I would look up how certain areas of the market have historically done during periods of “un-inversion” …

Consumer Staples has been the best-performing sector historically a year after the yield curve “un-inverts” (+15% better than the S&P 500). Health Care is second place at +10%, and Energy is third place at +8.75%.

Historically, other things have often (but not always) happened in the economy (and market) during periods of yield curve inversion that happened this time. It is entirely possible the “un-inversion” will not play out as it often (but not always) has historically, as well. Market action in the last 4-6 weeks looks to be moving according to this historical precedent (at least with staples and health care), but I would never dare call it predictive.

Speaking of the last month

I wrote last week how the market rally in August that followed the market sell-off in late July/early August was led more by defensives than technology. What I did not address was the state of Industrials, Materials, and even Energy (though midstream has been spectacular). The so-called cyclicals have been bruised, and with the decline in the U.S. dollar, this may seem counter-intuitive. I would suggest this is more macroeconomic-oriented, with Chinese growth continuing to lag significantly, U.S. manufacturing continuing to contract, and the capex story not accelerating as many hoped. They represent sectors that are out of favor (we like that) and attractively valued (we like that), but economic fundamentals and expectations also matter.

What keeps John Mauldin up at night

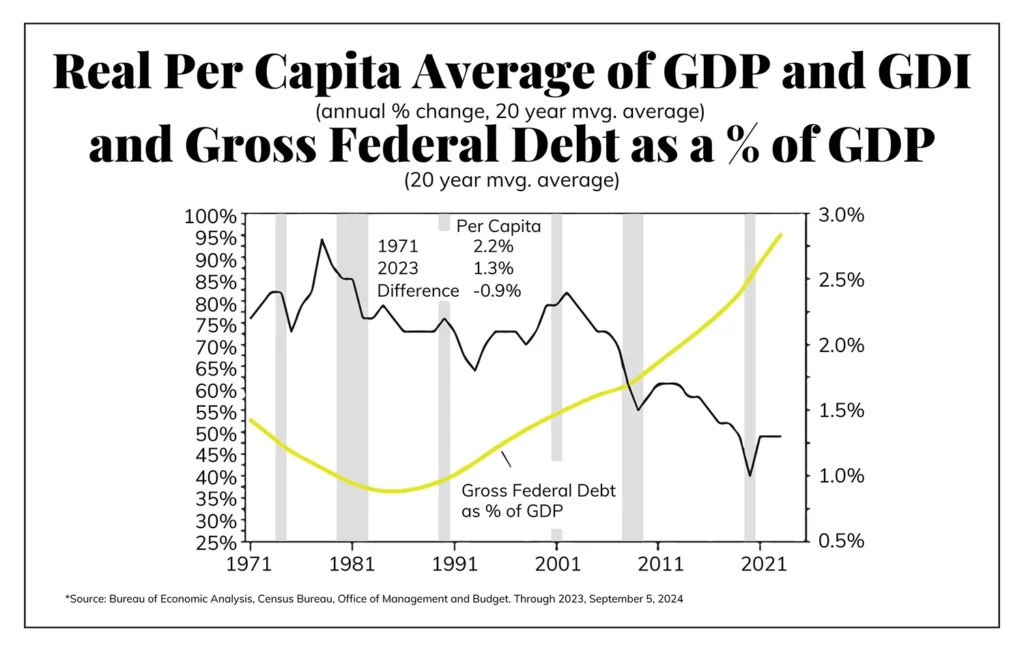

Government debt has grown trillions of dollars MORE than the economy itself has over the last decade. This is called a negative multiplier effect. Keynes talked about a positive multiplier whereby for every $1 of government spending, there was some increase in GDP of greater than $1. What we have done since debt-to-GDP passed reasonable thresholds is see a negative multiplier kick in whereby GDP IS growing but at a slower pace than that of government debt. Reinhardt and Rogoff found that economies lose one-third of their trend real GDP per capita growth when the government debt ratio rises above 90% for more than five years. This took place eleven years ago (h/t Lacy Hunt).

There is no question that real GDP growth has grown since 2014 much less than government debt has and that this reflects a textbook negative multiplier effect, whereby the diminishing return of excessive (non-productive) government debt erodes economic conditions.

Yen Carry Trade Extended

I have read more in the last six weeks than any healthy human being should read in a lifetime about the “yen carry trade.” One thing I am convinced of is that many people do not know what a carry trade is (i.e., buying an asset in one currency with money you borrowed from another is a carry trade; merely hedging a currency exposure is not). The idea that the unwind has much further to go because there are still lots of investors who have used the Yen for funding really misses the point. There may still be more speculators who need to be taken out behind the woodshed, but we know a lot of these actors already have their faces ripped off. Many others who used interest rate differentials and a currency outlook (which is always and forever RELATIVE) may or may not change their views in the years to come. But that is not the same thing as a carry trade, and the unwinding would not look the same if it did go that direction. The important thing for investors to remember is that the macroeconomics behind currency outlook are always moving targets and that many investors are always looking for SOME crowded place to build unhelpful leverage. Our job is not to know who is doing that or what they are doing; it is just to NOT do it ourselves.

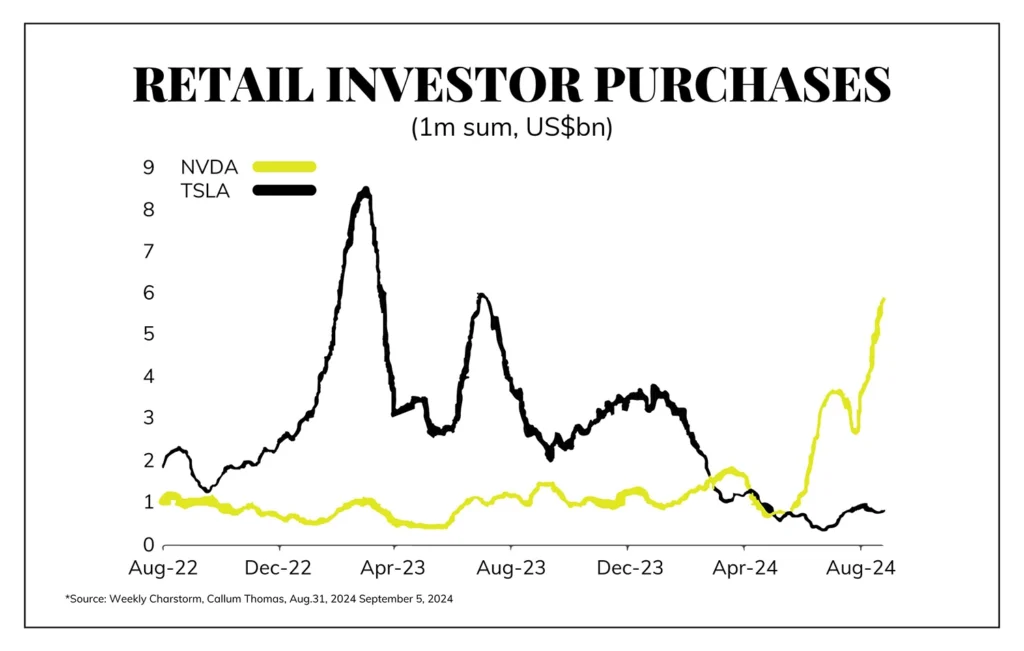

Chart of the Week

Tesla is down -35% since peak flows from retail investors came in. Peak flows from retail investors came into Nvidia right after it passed a +400% gain over a two-year period.

Quote of the Week

“Human reason can neither predict nor deliberately shape its own future. Its advances consist in finding out where it has been wrong.”

—F. A. Hayek

* * *

Next week, Brian will bring you the “Monday edition” Dividend Cafe, and I will be back in full saddle for Tuesday and beyond. I am leaning towards the following week for my “election edition” white paper Dividend Cafe but I need to nail down a hard date, still. If it is not out Friday the 20th, it will be Friday the 27th, but I will know more in the days ahead.

Have a wonderful weekend!

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet