Dear Valued Clients and Friends,

We are living in interesting times for equity investors, and I have no reason to believe those times will get any less interesting any time soon.

But one thing I would love for clients of The Bahnsen Group, and to a lesser extent, all readers of the Dividend Cafe is for there to be an understanding of what equity investors are really after. We all know “buy low, sell high” – and I even wrote a book once on how I think investors ultimately best monetize their participation in the stock market.

But I think a little more understanding of what one is paying for when one buys a stock may be useful (which of course, also implies a definition for what they are selling when they sell one). And if I do this right, maybe, just maybe, we will gain a better understanding of how to navigate the next phase of markets. To that end, we work.

Jump on into the Dividend Cafe.

What are equities?

At the most remedial level, we know that equities are fractional ownership interests in publicly traded companies. And we know that the essence of that ownership (economically) is a claim on future earnings and assets of the company.

But the mechanics of that claim can mean a few different things depending on the situation. It could mean that the assets of the company grow over time and that growth of value gets monetized by the shareholder selling their shares at a higher price (higher because the value of the assets the company owns is higher than it was when they bought their ownership interest. That is pretty rare – for one’s “claim on assets” to be the underlying objective or mechanic. But it could happen, more so with “asset-rich companies” that acquire plants, real estate, factories, land, machinery, etc.

But the aforementioned assets in the public equity space usually receive their value as a by-product of their cash flow generation. A piece of real estate becomes more valuable as it generates more income; a factory or plant has it improves productivity; etc. There is something inherently “operational” about company ownership because that is what companies are there to do. The “book value” of non-productive assets is a silly reason to buy equities. And “productive” assets are only productive to the extent they are cash-generating (or will be so).

So when one gets through the remedial definition and then works through the “claim on assets” component, what one really ends up with is a claim on future earnings. And this part is very important. Stock prices are: Your claim on future earnings aggregated together, discounted to some discount rate, with a risk premium attached.

Nothing feels like a “discount” here

So what one pays for a stock, all else being equal, is the sum of those future earnings of the company (pro-rata to their ownership), discounted by the appropriate rate one wants for their opportunity cost – their forfeiture of what they could have done with that money elsewhere. A “discount rate” is financial jargon for the cost of separating yourself from the money. Yes, you made $100 per year from your lemonade stand for ten years but had you had that money you could have made $2 at your bank, so as we “add up” those years of $100 profits from the lemonade stand, we “discount” them by the 2% you could have made not being invested in the lemonade stand. Does that make sense?

Therefore, because of math, the higher the “discount rate” one uses, the less valuable the future stream of earnings is now, and the lower the discount rate, the more valuable it is.

This is why we talk about the “risk-free rate” being so important in how we value equities (and all risk assets). Because it is economically fundamental to value assets by their future earnings. How much will I pay for a lemonade stand? I will pay what I believe I will make from that lemonade stand in the future, obviously, reduced by what I would have made had I not bought the stinkin’ lemonade stand.

Well, the same is true of a software company, an energy pipeline, an apartment building, a retail outlet, or a solar panel manufacturer. Lemonade stands just generate more sympathetic customers to the plight of adorable children.

And then that other piece

Then, beyond the (a) Stream of future earnings, and (b) Discount rate applied to those earnings, we also have the (c) Risk Premium. This is where financial vocabulary is a little confusing because a risk premium is actually a discount for a buyer – and a cost for a seller. The investor in a lemonade stand has some “premium” they want relative to the risk they are taking – above and beyond the “opportunity cost” of the risk-free rate. Yes, they could have gotten $2 in their bank, and yes they expect to get $100 in annual cash flows, BUT they also know they COULD face weather concerns that wipe out a Saturday afternoon of street-corner sales. They COULD face health food crazies demanding that the lemonade not have sugar and all lemonade stands selling sugared lemonade face fines and government regulation. They COULD see Johnny down the street steal the cash register money one day to buy some ice cream and eat away at a weekend of profits. So besides the “risk-free rate,” they want some other return. That return they want to compensate themselves for the extra risk they took of Johnny the ice-cream eating clepto, health food zealots, and unreliable weather is called the “risk premium.” It gets factored into what they will pay for the company. It is the “expected return less the risk-free rate.”

So when you see a stock price, it can be deconstructed as:

(1) The sum of future earnings,

(2) Discounted by the aforementioned discount rate,

(3) Further “discounted” by the “risk premium” (confusing, right)

The vocabulary seems backward because the “premium” in return IS in fact reflected as a DISCOUNT in the price. Consider this.

I believe I will make $100 from a lemonade stand over the next year.

I believe I will make $2 if I don’t buy the lemonade stand.

But I want at least $8 for the risk of Johnny, the weather, and all that stuff.

Therefore, I believe a lemonade stand that will generate $100 in the future is worth $90 now – $2 as a discount rate and $8 as a risk premium.

Make sense?

Not so fast

The problem with my example is I used ONE YEAR of discounting the earnings of this lemonade stand to establish a present value. In real life, we are generally thinking about many years, which complicates the consideration of the “discount rate” being applied to the future earnings, not to mention the “risk premium.” The more time that goes by, the more potential for risk, uncertainty, etc. So our “valuation” of these things not only combines:

(a) Calculation of cash flows (which are fallible),

(b) The application of a discount rate (which can and will change),

(c) A computation of a risk premium to account for all of the risks involved,

but also (d) The aforementioned three components applied to a certain time horizon.

What does your stupid lemonade stand have to do with today’s stock market?

The valuation of one’s fractional ownership in claims on a company’s assets and cash flows is done very differently for different types of companies. The highest performing stocks of the last five years or so had all these things going for them:

(1) Calculation of future cash flows was highly optimistic, or even unnecessary because the assumption was simply for massive growth (fair enough, by the way)

(2) The discount rate being applied to these considerations was the lowest in history

(3) The “risk premium” being demanded for these assets has been extremely low as investor confidence in the success of the “new economy” has been, shall we say, high

(4) The “duration” of these equities – the “time” being factored into their valuations has been almost infinite (“I feel good that this new app that gets me a ride to work and offers yoga in the backseat while it delivers me an organic smoothie and is fully solar-powered will start to make money by the year 2065”).

In all four variables, they have lent themselves to a growing price in present value (i.e. buyers willing to pay more now).

What does this have to do with today?

It is fair to ask ourselves a few questions around each category of stocks out there:

(1) What is the reliability of our calculation of future earnings? Is there even a path to future earnings at all? Are the earnings we anticipate real? Will they grow? Do earnings matter? Does quality of earnings matter?

(2) Is the discount rate going to go higher or lower? If it goes higher (the opportunity cost of investing), what does that do to high P/E stocks vs. low P/E stocks?

(3) Do we expect investors will want a higher risk premium in the future or a lower one? If risk premiums are at historical lows (or were a month ago), and if various geopolitical, monetary, and economic conditions are becoming more complicated, with more uncertainty, what will that do to risk premiums, and in what areas of the market will it be most enhanced?

(4) What does a higher discount rate mean to “long duration” stocks vs. “short duration” ones (meaning, ones whose profits are expected way out in the future vs. those already generating mature profits now)?

What I recommend

In the environment, we are in, and coming off the environment we have been in, I would suggest that buying companies of good earnings, now, that are understandable and coherent, now, makes the most sense. I would suggest that companies of an uncertain earnings outlook not only suffer from what will need to be a higher risk premium, but also from a long duration risk that, when discounted to a rising discount rate, provides double the risk and double the trouble.

I would favor simplicity, clarity, and good math. Where there is no attempt at math, no ability to do math, and no belief that math matters in how your investments are valued, I would steer clear. Those moments have not generally ended well.

And ultimately, I would not buy a stock because you want the stock price to go up. I would buy a company, because you want to own the company.

I agree with that last line today as much as I did in 1969 when Warren Buffett first said it.

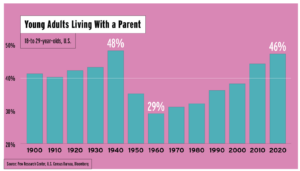

Chart of the Week

Interesting sociological dynamic, and perhaps an interesting economic one.

Quote of the Week

“The a priori assumptions of rational markets and consequently the impossibility of destabilizing speculation are difficult to sustain with any extensive reading of economic history. The pages of history are strewn with language, admittedly imprecise and possibly hyperbolic, that allows no other interpretation than occasional irrational markets and destabilizing speculation.”

~ Charles Kindleberger

* * *

More fun things are planned for next week – particularly on the monetary and Fed front. I have a lot of writing to do this weekend, but I am hopeful for good things with some pending DC Todays and next week’s Dividend Cafe. In the meantime, of course, reach out with questions and comments. And have a great weekend!

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet