Buzzwords.

They can be really annoying, right?

At their inception, they are the perfect descriptor, and that’s why they are so catchy. Then they flood the conversation and quickly lose their potency. Eventually maturing into plain old industry jargon.

Here’s one for you: Holistic Financial Planning.

Again, at its infancy, I can understand why the term stuck – the world was changing, and people needed advice, not stock tips; they needed advisors, not brokers. Over time though, the term holistic financial planning became meaningless, and I am not even sure if those promoting it, actually knew what they meant by it. This buzzword was destined for the financial jargon graveyard.

A Stroll Down Memory Lane…

In May of 1792, 227 years ago this month, stockbrokers began brokering trades on the streets of New York. Over time these stock exchanges would continue to grow in size and complexity, offering a platform for buyers and sellers from all around the world to transact. For much of those 227 years, a broker stood in the middle of each of these transactions acting as an intermediary and charging a commission for each trade.

A couple of hundred years later and retail brokers like Fidelity and Charles Schwab hit the scene. The price wars amongst these institutions would help to shrink transaction costs and cause our friend the stockbroker to become nearly extinct.

Fast forward to today, and you’ll find a world in which pensions are rare, and investors are now responsible for managing their own financial futures. You’ll see a new trend in motion, a generation of consumers seeking out guidance and advice. And a growing population of professionals looking to help these investors navigate their personal finances and provide holistic financial planning.

Thus, the buzzword was born.

Quilts vs. Puzzles

Regardless of my annoyance with the term or its overuse within industry marketing, investors should expect holistic advice. Meaning there is a need out there for advice that accounts for all the unique facets of someone’s particular situation (think: goals, time horizon, tax bracket, risk tolerance, etc.) Juxtapose this against our history lesson of the stockbroker, and you’ll easily recognize the difference – it’s the constant need for advice/guidance versus brokering a one-time transaction.

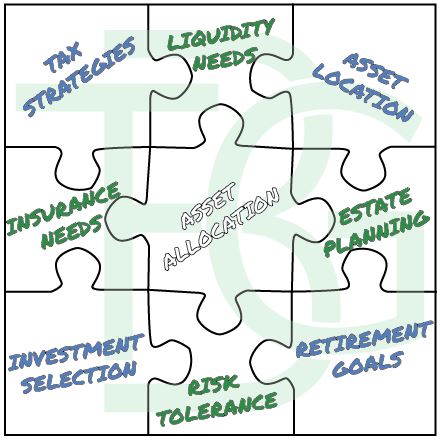

So, what does “holistic” look like in practice? It looks like a puzzle, not a quilt.

Most investors have a quilt. They have a collection of tips and tidbits that turned into transactions, which they’ve accumulated over time. An old 401(k) from a former employer here, an insurance policy bought from an old college buddy there, an IRA inherited from an aunt, and so on and so forth. Then you stitch these all together, making a hodge-podge financial quilt.

Here’s the problem. Each of these quilt squares was designed in isolation, created without the acknowledgment that anything else existed. All the pieces are not accounting for potential redundancies that might elevate the risk exposure of the whole, the squares do not know whether or not the correct legacy planning is weaved throughout the entire quilt, there was no attempt to leverage cost efficiencies, and most definitely tax-efficiency was not accounted for. No, this is a quilt, just a collection of old things gathered along the journey. The quilt tells a story indeed, but it does not make for the ideal financial plan.

A puzzle, on the other hand, is much different. When you build a puzzle, you start by laying out all the pieces on the table. Then you build the puzzle, one piece at a time, making sure that each addition fits in with the existing structure. During the whole construction process, you have the end result in mind – the photo on the cover of the box.

Good financial planning work is much the same. The cover on the box for a financial plan are the goals and aspirations of the investor. The pieces in the box are all the moving parts – the insurance, the retirement plans, the college expenses, etc. The financial advisor is collaborating with the investor to make sure that all details are accounted for. The objective is to see all the pieces as part of the whole; this is holistic financial planning.

The Construction Process

Let’s zoom in a bit more to see what this looks like in practice. When working with a new client, my first step is always to build out an accurate net worth statement. This puts all the puzzle pieces on the table to see what we are working with. Once we agree that we have captured an accurate snapshot of the client’s current resources and liabilities, we transition to discussing goals.

As part of this fact-finding process, it’s important to find out all the details: dates for retirement, current expenses, future one-time expenses, current income, tax bracket, risk tolerance, etc. These details will lead to crafting an appropriate asset allocation across the client’s balance sheet. Once those allocation targets are set, then I’d move onto implementation. It’s best to implement these allocations with a client’s tax situation and liquidity needs in mind. This is to say that the asset location will matter. A client typically has a collection of tax-deferred and taxable accounts, so there should be a rhyme and reason for how the strategy is being implemented across the portfolio.

If you are thinking that this is a lot of steps and a lot of details, you are right, it is. This is what holistic financial planning looks like. We all have different levels of complexity when it comes to our own financial lives and that complexity warrants intelligible planning and design work. This is the beauty of building puzzles vs. quilts.

So… Do you have a financial quilt or did you build yourself a financial puzzle?