We are fearful of all sorts of market monsters that may be creeping around the corner – recessions, volatility, rising interest rates, etc. – but there is another monster that we just don’t pay enough attention to even though it’s constantly lurking in the shadows. I am just going to come right out and say it; we don’t take inflation seriously enough.

BREXIT and trade talks with China might steal the headline news today and tomorrow it will be something else or more of the same. These current events are fleeting and rarely damaging to our long-term financial success. But always be lurking in the background – unseen and often forgotten – inflation remains a real and potential culprit of long-term financial destruction.

Why?

Because it is the stealthiest of all the risks out there, inflation is an absolute ninja. It lulls you to sleep with its 2 or 3 percent erosion per year and then BOOM! all of a sudden you look back over 20 years and realize that everything around you is a lot more expensive. Your money is literally worth-less and you never even saw it coming.

FACT: Inflation from 1914-2018 has averaged 3.23%. At this rate, your buying power gets cut in half every 20 years.

Source: minneapolisfed.org

Why should you care?

Because what you might think is safe, really isn’t. It’s natural for us to want to squirrel away cash under the mattress and call it a “rainy day fund” or an “emergency fund.” The problem becomes when this allocation begins to grow and dominate our balance sheet.

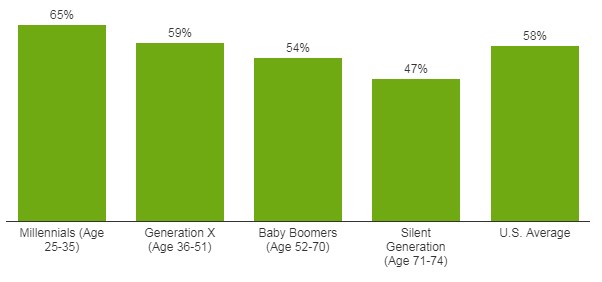

According to BlackRock’s Global Investor Pulse Survey 2017, these are the cash allocations across generations:

Source: Blackrock

Yikes! The Millennials, with the longest investing time horizon, have the highest allocation to cash. According to the FDIC the average savings account in the US is currently yielding 0.10% and according to the Bureau of Labor Statistics inflation over the last 12 months was about 2%. This is the illusion of safety that I am referring to. You earn a tenth of one percent on your cash savings, and the things that you want to buy are increasing by two percent. It doesn’t take a math wiz to realize that equation is not in your favor.

So, what’s the solution?

Uncertainty.

I know, it sounds crazy, but stick with me.

In finance, we call it volatility or risk, but it’s really just uncertainty. If you are willing to accept some level of “price uncertainty,” not knowing exactly what your investment will be priced at tomorrow, you will be rewarded for this. We call this reward a risk premium.

Most people love certainty and despise uncertainty. This is what attracts them to a cash savings account. The problem, as we learned above, is that the return on these accounts is typically less than inflation. This is fine for the money we plan to spend today or tomorrow but poses a real problem for our long-term investments. Remember, if your investments operate at an “inflation deficit” for too long, the negative effects will compound in a BIG way.

Again, the solution to outpacing inflation is to accept some level of uncertainty in your portfolio.

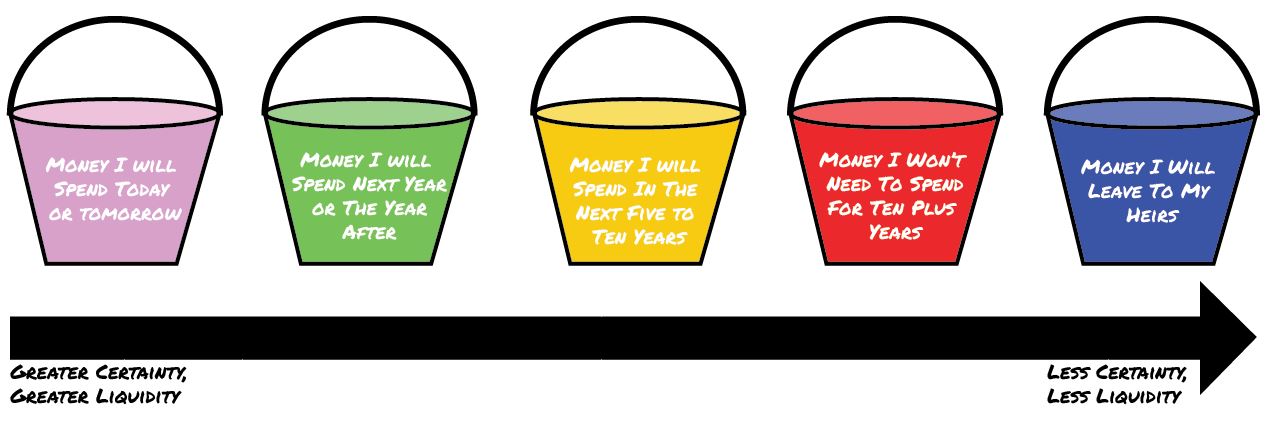

Buckets, Not Pies

The level of exposure to uncertainty (think stocks, bonds, etc.) will depend on a lot of factors: your risk tolerance, liquidity needs, time horizon, etc. To avoid over-allocating to certainty (cash), try imagining your portfolio as multiple buckets rather than a single pie.

This is what I mean. Here is the traditional way one might view their investment portfolio:

From the illustration above, let’s imagine that the gold color represents cash, the green represents stocks, and so on the other pieces of the pie representing other allocations. This type of portfolio is often constructed based on the answer to one simple question, “Are you conservative, moderate, or aggressive?” Let me fill you in on a secret… everyone answers “moderate.” It’s a misleading question, and the result doesn’t help you customize your portfolio to your particular financial plan.

Try shifting your thinking from pies to buckets. I am assuming that you have saved some amount of money that is greater than what you plan to spend this year. With that assumption in mind, you can just take what your annual expenses are (planned spending) and place them into the bucket that’s most appropriate, like so:

As you can see in the descriptors beneath the timeline arrow, for money that is earmarked to be spent in the short term, you should find investments with greater certainty and greater liquidity, i.e., cash or government treasuries. For the money that is earmarked for the long-term, you can venture into investments with greater volatility (uncertainty), and liquidity (quick access to the money) becomes less important, i.e., stocks or private investments.

After completing this type of exercise, ultimately, you will end up with a classic “allocation pie.” The difference is that you will get to this final allocation through a process that helps you frame these decisions better and results in a customized allocation tailored to your current and future needs. Most important to remember, the primary objective is to strategically and effectively build an allocation that meets your short-term needs and assures that your long-term investments outpace inflation.

Signing Off…

Ok, TOM readers, that’s all we’ve got for you this week. I hope you enjoyed this lesson on inflation and picked up a few tidbits on how to improve your financial plan. I’d encourage you to listen to David Bahnsen’s Advice & Insights: Special Edition – A China Trade War Update where David provides some excellent insight and commentary on the current trade deal looming over the White House. As always, feel free to contact us with your questions, and this is TOM signing off…