My 16th birthday is one I’ll never forget.

My grandmother sent me a letter explaining that she was gifting me $1,000, with two stipulations: it had to be invested in the stock market, and it couldn’t be touched until after college. To paraphrase her message:

“This is to jump-start your future. I hope it inspires a love and passion for investing.”

Jump-start my future? Check. I still remember cashing in those funds to help pay my final college tuition bill.

Inspire a love and passion for investing? Also check. Ever since walking into my parents’ advisor’s office shortly after my 16th birthday to choose my first investments, I’ve been captivated by the opportunity to steward wealth through the market.

The $1,000 check was meaningful – but the principles and inspiration my grandmother passed along have paid the greatest dividends.

That early lesson – that investing isn’t just about dollars, but behavior – frames how I think about different investment options.

The Jump-Start

The message my grandmother gave me on my 16th birthday closely mirrors what Trump Accounts aim to communicate:

We want to jump-start your future and inspire an interest in investing.

Although the accounts may not be a game-changer as a tax shelter (read on to find out more), I believe they’ll become an important behavioral tool for American families, inspiring millions of Americans to start investing.

The Introduction of Trump Accounts

In 2025, the One Big Beautiful Bill Act included a provision to allow for a new type of investment account, dubbed the “Trump Account.”

With IRAs, 401(k)s, 457 plans, JTWROS accounts, and UTMAs (you get the picture), why add yet another account type to the confusing world of personal finance?

As President Donald Trump states, “This is a pro-family initiative that will help millions of Americans harness the strength of our economy to lift up the next generation. And they’ll really be getting a big jump on life.”

Regardless of one’s politics, the relevant planning question is not the account’s name, but rather how it compares with the alternatives.

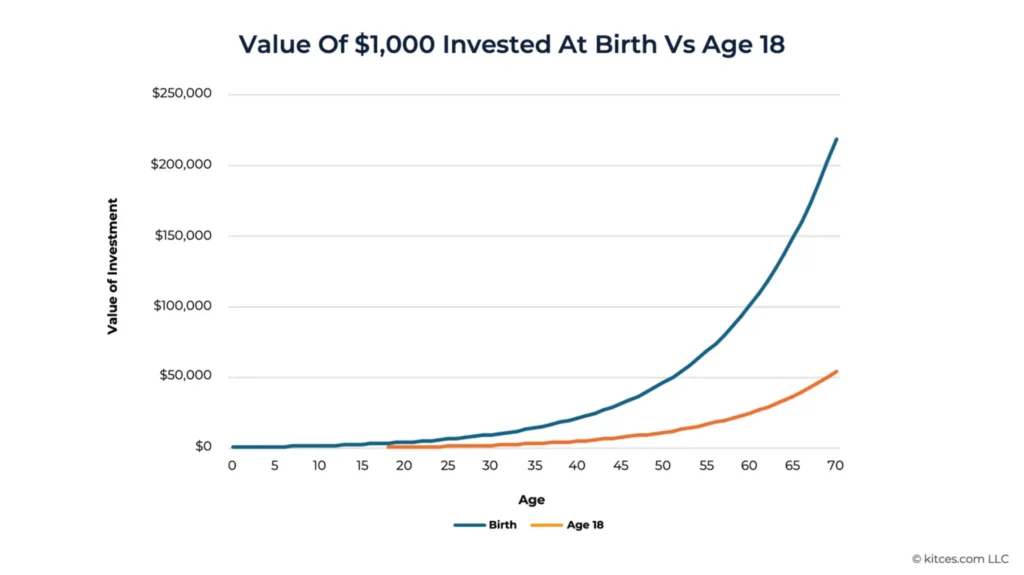

The Eighth Wonder of the World

It’s no secret that America is a consumption-driven society, often procrastinating on saving. It’s also well known (at least, intellectually) that investing money early in life can lead to an incredible compounding effect. Albert Einstein described compounding as the eighth wonder of the world.

The impact is striking – especially when comparing investing at birth versus starting at age 18 (as shown below, using 8% compound annual growth rate).

*Source: Kitces.com LLC, June 25, 2026

What is a Trump Account?

While Trump accounts can officially be funded on July 4th, the structural rules and mechanics are largely in place, and the US Department of the Treasury has reported that more than 6 million children have been signed up (https://www.cnbc.com/2026/06/23/trump-account-signups-hit-6-million-millions-more-children-eligible.html).

A Trump Account is a government-initiated investment account for children, designed to encourage long-term savings from an early age. As described, “Trump Accounts are traditional individual retirement accounts with special rules established under section 530A of the Internal Revenue Code.” (https://trumpaccounts.gov/).

Core characteristics include:

- Accounts can be established for any U.S. child under 18 with a valid SSN.

- An automatic $1,000 from the U.S. Treasury will be given to every American child born between 2025 and 2028.

- Contributions of up to $5,000 per year (no earned income required), which are not tax-deductible. However, these contributions count as “basis”, which can be withdrawn tax-free (assuming basis is properly tracked)

- During the “growth period” (from establishment of the account until age 18)…

- Investments are restricted to broad US-based equity index funds

- Withdrawals are completely restricted

- Growth is tax-deferred

- Upon reaching age 18, the account effectively converts to a Traditional IRA, at which point standard IRA withdrawal rules apply.

The summary: This program is designed less as a deduction-driven tax shelter and more as a behavioral tool to get capital working and compounding from an early age. The investment restrictions (limited to U.S.-based stock index funds) may ultimately prove to be more of a feature than a bug, helping to reduce common behavioral mistakes such as parking long-term capital in cash for extended periods of time.

Get a Free Lunch

If your child was born between January 1, 2025 and December 31, 2028, take advantage of the free money! David Bahnsen tells us “There’s No Free Lunch”, but in this case, it really is a $1,000 head start. In my experience, establishing the account for a child has been seamless. The official website (https://trumpaccounts.gov/) is easy to navigate and provides additional educational materials.

A $1,000 deposit seeded at birth can turn into over $5,500 by age 18 (assuming a 10% annual growth rate). Not bad, especially for nothing out-of-pocket.

In addition to the U.S. government “seed” money, other prominent donors have pledged to jump-start the program. In fact, Michael & Susan Dell committed $6.25 billion to fund Trump Accounts for around 25 million American children, intended to provide seed money for children too old to qualify for the initial $1,000 deposit from the federal government. (https://www.cnbc.com/2025/12/02/trump-accounts-claim-money.html)

If other contributions are being made on your behalf (such as the potential gift from the Dell Foundation), once again – take the free money!

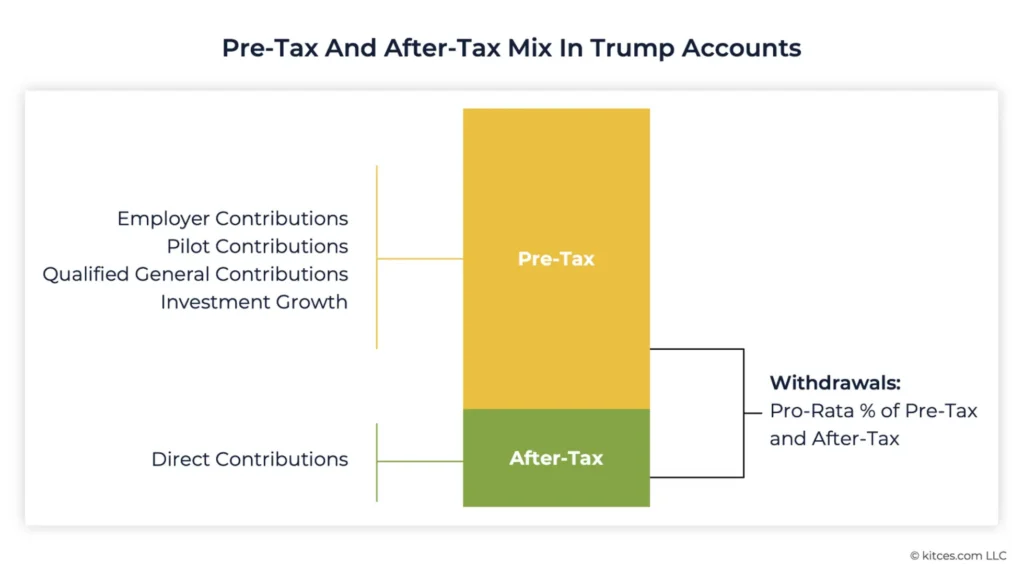

Taxation Example

You may be wondering how exactly these accounts get taxed, given that there are three elements to the account…1.) US government contributions, 2.) Parental contributions, and 3.) Growth.

Let’s say my son was born in 2025 and received the free $1,000 from the US Treasury. In 2030, I get motivated to save more money for him, contributing $3,000 myself.

By 2043, my son turns 18 years old, and this hypothetical Trump Account has grown to $10,000 – all tax-deferred, which means no taxes have been paid along the way.

At this point, my son decides to withdraw all $10,000. The withdrawal will include $7,000 of taxable income and $3,000 of tax-free basis. The US Treasury’s contribution is NOT counted as a basis, so only what I contributed myself becomes tax-free. In addition, my son may have to pay a 10% penalty on the taxable portion (depending on what he uses the money for, he may qualify for an exception to this penalty).

If my son withdrew only a portion of the account, then the pro-rata rule applies. For example, 30% of his account is on an after-tax basis ($3,000 of the $10,000 account value). So, a $5,000 distribution would include $1,500 of tax-free basis and $3,500 of taxable income. The chart below helps to explain.

*Source: Kitces.com LLC, June 25, 2026

Should You Contribute?

Beyond the free money, I find Trump Accounts to be limited in their benefit, save for one proactive planning technique.

While the idea is transformative (auto-enrolling millions of children into the participation of capital markets and the corresponding compound investment growth), the actual tax benefits of the accounts leave a lot to be desired.

Consider the following hypothetical scenario…

- Marvin Moneybags (the parent) contributes $1,000 per year to his son Calvin’s account from birth through age 18.

- When Calvin turns 18, his account (with 10% annual growth) is worth ~$55,000 ($18,000 of contributions and $37,000 of growth).

- At this point, Calvin the Compounder decides he’d like to leave his money in the account until he retires at age 65 (otherwise, the $37,000 of growth would be taxable and likely subject to a 10% penalty).

- With 10% annual growth, $55,000 becomes ~$4,850,000 by age 65. Because Trump Accounts are tax-deferred, none of this money is taxed along the way.

- While this sounds incredible, all but $18,000 of this $4,850,000 will be taxable at Calvin’s ordinary income rate when he withdraws the money. If Calvin is a high earner in California, a significant portion – potentially over 50% – could ultimately go to taxes.

Given that the tax liability on a Trump Account increases as the account grows, this is not a very attractive scenario, especially compared to the other (more favorable) account types.

Proactive Planning via Roth Conversions

However, consider what some proactive planning can do.

- At age 18, Calvin is employed full-time, filing his own tax return and not a dependent on his parents’ return.

- Being the proactive, mature young adult he is, Calvin decides to process a Roth conversion of his $55,000. Because after-tax contributions total $18,000, $37,000 of this would be taxable to Calvin upon conversion.

- Assuming Calvin is in a low tax bracket (given he just started his career), the conversion would likely have a small tax consequence.

- Assuming the taxes on the conversion are paid from cash (NOT from the Roth conversion itself), then Calvin the Compounder now has $55,000 growing tax-free for the rest of his life.

NOTE: If the young adult is still a dependent on the parents’ tax return, or is a student supported by their parents, then much of the Roth conversion may end up taxed at their parents’ tax rate.

The optimistic side of me says this Roth conversion strategy could be used quite effectively, especially if you have a proactive financial planner following through on the strategy and navigating the potential “traps”.

The skeptical side of me says very few young adults will actually follow through on it, at which point the account becomes essentially locked until retirement with a growing tax liability.

So Many Options…

As David Bahnsen reminds us, the three most important words in economics are “compared to what?”

The good and the bad news? There are many options to save for your kids.

Attempting to determine which account is best becomes a stressful endeavor. It’s like trying to pick the right ice cream flavor at Baskin-Robbins. 31 flavors can become overwhelming.

What is the Goal?

If your desire is to save money for your kids, the first question to ask is, “What are you really trying to accomplish?”

Once we understand the goals for this money, we can review the options and select the account(s) that make the most sense.

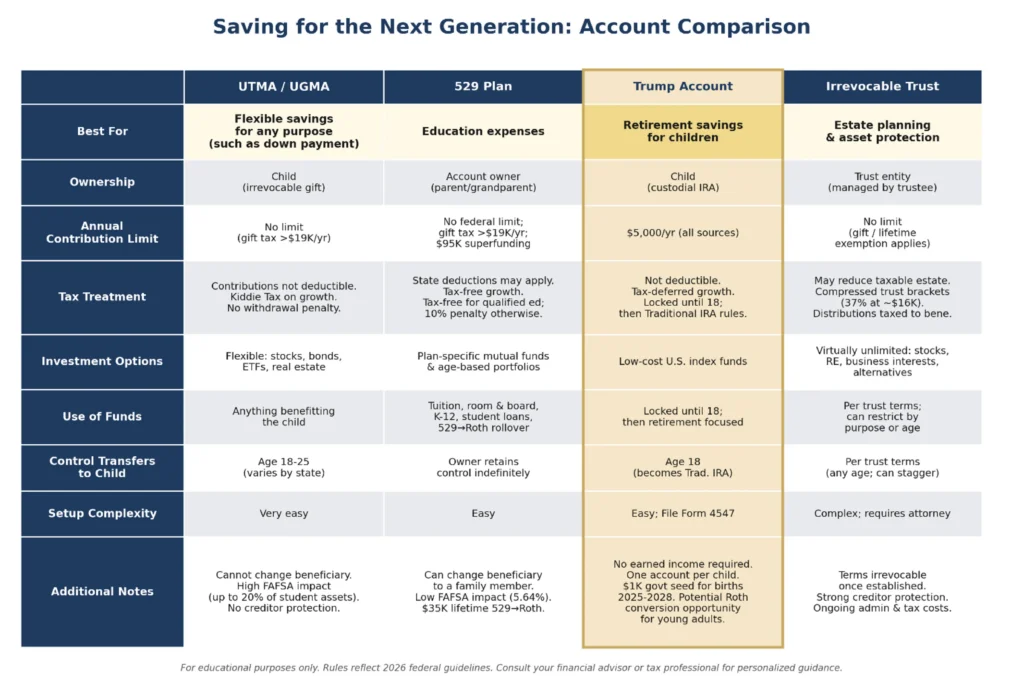

For comparison purposes, I’ve included a chart below of four common account types. Keep in mind this is a non-exhaustive overview, and there are a variety of nuances that a simple chart may not fully capture.

*Source: Kitces.com LLC, June 25, 2026

As you see above, all four of the account types can serve a purpose. But the question goes back to “what are we really trying to accomplish?”

The top row, “Best For”, provides a general overview. For example, if you are trying to save money for your child’s education, then 529 savings plans are typically the most effective account.

There are additional options, including…

- Roth IRAs if the child has earned wages, and

- Parent-owned brokerage accounts that are simply earmarked for the child

With various tax consequences, differences in control, and investment restrictions, a conversation with your advisor is encouraged. Keep in mind, many parents & grandparents choose to utilize 2 or 3 of these account types. For additional commentary, we encourage you to listen to our podcast.

My view of Trump Accounts is similar to my view of Dave Ramsey’s financial advice. I don’t often agree with his financial guidance, as it often lacks nuance and optimization. However, I admire the way his program WORKS because he understands the psychological barriers to action.

I believe Trump Accounts will have a similar effect. Although the tax realities of these accounts are not advantageous in most cases, the reality is that…

- Millions of children will start compounding $1,000 from the day they are born, which means…

- These same kids will experience the miracle of compound interest via the stock market, which will lead to…

- Millions of Americans are more motivated to save and invest for their future.

I can get behind that.

Your Next Step

The question isn’t really whether a Trump Account is a game-changer or a gimmick, but rather if it fits within a thoughtful plan for your family.

If you’re considering saving for a child or grandchild, or evaluating if a Trump Account fits in your plan, we’d welcome the conversation.

Reach out to your Private Wealth Advisor or drop us a note at . We’re here to cut through the noise and build a plan that aligns with your savings goals.

Brett Bonecutter

Private Wealth Advisor