I am an absolute glutton for nostalgia; I’m a softy.

Every day my iPhone populates these reminders of “my memories.” The software puts together these short video reels with collections of different photos from my phone. A sort of life-over-the-years type theme. The elevator music on the clip plays softly in the background as a selection of photos from my kids two years ago or a vacation we took last summer to populate one by one. Again, I am a softy. These little videos are always a tearjerker for me. I console myself saying under my breath, “They grow up so fast…”

I am on a family text, and we often exchange these memory video albums with each other. Corporate or familial nostalgia only amplifies these emotions and sentiments.

One of my favorite finance writers talks about how he would spend hours at the library reading antiquated Wall Street Journal publications from historically significant dates. He describes the benefit he gleans from understanding what it felt like for those writers and reporters at the moment leading up to The Great Depression or the day following 9/11.

You become a time traveler of sorts. When reading, you get to live in the moment of the author, but you have the benefit of knowing what’s written in the next chapter. In statistics, they have rules (or etiquette) for running clean data sets to make sure that you are not backtesting an investment model based on information that you wouldn’t have had at that point-in-time. For example, if I ran a model that created a portfolio of companies with the highest profit growth per year, I would illustrate some incredible results, yet this would infer that I could know on January 1st which companies would have the highest profit growth on December 31st of that year.

Every New Years, my wife and I watch When Harry Met Sally. Perhaps Harry said it best,

“When I buy a new book, I always read the last page first, that way in case I die before I finish, I know how it ends. That, my friend, is a dark side.”

Now, with more than a sufficient introduction on this topic, I’d like us to exercise some Thoughts On Money nostalgia and revisit an article I wrote on February 19th, 2020: Why It’s Sometimes Ok to Underperform.

First and foremost, we can all acknowledge what a unique time in the history of our country was on February 19th, 2020. At that time, I/we had not even the faintest clue of what the next handful of years would look like and the cultural collateral damage that COVID would cause.

In this former writing, I was making the argument that, at times, it is not only ok but should be expected to underperform if you have a particular investing strategy that you’ve committed to for the long haul. I use the term underperform loosely and more as a descriptor that you will always find another strategy that may have been superior in a season, but this is only realized in hindsight. Furthermore, I was highlighting the headwind or drag that the energy sector was having on my personal investments, yet I believed it to be an opportunistic allocation. I laid out my reasoning that this allocation was a coiled-up spring of sorts, and the headwind today would soon (as I believed) be a tailwind for my portfolio.

In this article, I highlighted this specific image (see below), noting the reality of where energy was over the first 45 days of the year and, understandably, how some could find that disappointing.

Source: StateStreet (as of 2-18-2020)

Let’s just say that this piece did not age well if you were rereading it at the end of 2020 and casting your final judgment at that standpoint. A picture is worth a thousand words. See below…

Source: AWealthOfCommonSense.com

If you were feeling fed up with a strategy/approach that favored an allocation to energy investments in February, you may have hit your tipping point by December. In my experience, these are the moments that can make or break you as an investor. You are forced to reexamine your philosophy and reaffirm your convictions in the midst of a season of struggle. To add salt to the wound, any coffee or cocktail conversations with a friend touting their results speculating on big tech names may have made you feel a bit less than others. It’s lonely being a contrarian, as the name would suggest.

Yet, great investors do not succumb to peer pressure. They do not capitulate on their convictions easily. Warren Buffett has been accused every so many years over the last 50 years or so to be potentially “out of touch” with the “new” reality of investing. If you’re curious, 92-year-old Warren hasn’t abandoned his approach, and he has continued to build on one of the most impressive investing careers of all time.

And there is still another layer to this story. This article I had written was all in response to a conversation with a friend who was employing the same strategy/approach that I was. My attempt was to comfort him and encourage him not to abandon ship. The aftermath that I was not able to share at the time of that writing was that he did eventually call mercy.

I vividly remember my conversation with him in early 2021 when we split ways, and my final encouragement was not to abandon his energy positions yet. I told him that he had already been punched in the mouth a few times on these investments, yet the boxing match wasn’t over. I didn’t think it was fair to him to have taken the risk without sticking around for what I believed would be the eventual reward.

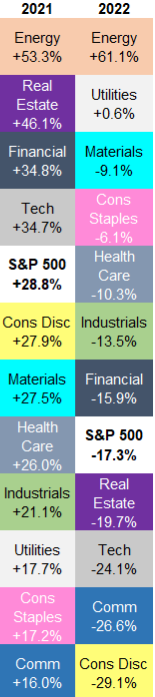

Over the last two-plus years, I was in the dark. I didn’t know where that investing journey for my friend went and how it had all turned out for him. It came to mind every once and a while, but I always just wished for and hoped for the best. A common adage in the world of investing is to say, “I wasn’t wrong, I was just early.” Perhaps that was the appropriate response in this case, as we now know how 2021 and 2022 played out:

Source: AWealthOfCommonSense.com

The reason I am even writing this today is absolutely not to highlight that one allocation had a troubled year followed by two strong years of recovery but because my friend did follow up with me in the last few weeks asking for some guidance/advice. This was my first opportunity to look under the hood and see what had transpired since we last connected some 28 months ago.

As I assumed, and perhaps understandably so, last year (2022) was quite a troubling year for his portfolio. The darlings of 2020 that he had regretted not owning, he acquired in 2021 and was left to endure the pain they dealt out in 2022. It was like he experienced the downside of risk in 2020, but didn’t stick around for the reward, then he chased the shiny objects where the rewards were in the past just to endure their risk as well. It was a painful scene indeed and one that is not unique to my friend. This is the classic challenge of investing – a sport of endurance.

In my February 2020 writing, I concluded with a section called “Buffett vs. Nasdaq” and drew attention to 1999, where the Nasdaq outperformed Buffett by more than 100% in a single year. If you’ve ever had a bad hair day, tripped and fell in a large public setting, or had your voice crack as a teenager during a school presentation, then you understand what embarrassment feels like. We are human, we hate the feeling of being embarrassed, and we hate the feeling of missing out. Another section in that article I titled, “Thou Shalt Not Covet.” You get the idea. Yet, again, with the benefit of hindsight, we know that Mr. Buffett was the tortoise of this story and that over the next few years(2000-2002), he handily outperformed the hare (the Nasdaq).

Again, investing is an endurance sport and not for the faint of heart. The damage caused by constant strategy rotation and chasing yesterday’s winners is real. I looked at an investment statement from 2021, and that same statement in 2023 for my friend, and I got to see the real impact of these decisions.

I hope you know that my heart here is absolutely not to poke fun or to create an I-told-you-so moment. My hope is that we can all glean wisdom from these stories because they go beyond the textbook; they are not just theory. Anecdotal, yes, but the practical application of what we study here on TOM every week.

So, what’s the primary takeaway? Well, the title is a good place to start because it was true in 2020 and it is true today “It’s Sometimes Ok to Underperform” or better said; you can always find better results in hindsight, but the goal is to adopt a philosophy that suits the needs of both your plan and your personality. Flip-flopping philosophies is a recipe for disaster and will ultimately create financial harm. Now, this is not an advocation to simply be stubborn for stubbornness’ sake or advice to not adapt to your environment, but rather to create a foundation and pillars of financial truths to build your investing approach on top of. Warren Buffett surely knows more about investing today than he did 50 years ago, yet those pillars of financial truth and wisdom that were true 50 years ago still have application in his process today. How can this be true? Because markets are made up of people and human behavior – fear, greed, coveting, etc. – were around since the beginning of time as much as they are today.

I’ll leave you with this, friends, investing is already hard enough, don’t make it even harder than it needs to be.