Dear Valued Clients and Friends,

I send this week’s Dividend Cafe at the end of a 24-hour trip to Las Vegas, where I spoke at a conference yesterday. 2,600 people have come to the 110-degree city of sin for the purpose of hearing various economic and political musings, and one such forum of musings was a panel with myself, Steve Forbes, George Gilder, and Mark Skousen discussing, of all things, my book! It was a surreal experience to be next to Gilder, whose Wealth and Poverty was a transformative book in my intellectual development as a pretty darn young guy (you would actually think less of me if you knew how young I was when I read it).

Anyways, by the time you read this, I will be on a plane back to New York City Friday afternoon, where I will be working all of next week before returning to Newport Beach next weekend.

We are living in a time where there have been more bad ideas than money to invest in (or at least bad prices at which to buy those ideas). Soon we will see more money than people acting on bad ideas. But right now, a little parsing out of what the laws of contrarian investing mean is in order, and I think you will find it fascinating.

Jump on into the Dividend Cafe …

|

Subscribe on |

Investing is easy

Louie Gave recently reminded me of the famous mantra from Neat Botz:

“Investing is an easy game. You have to figure out whether there is more money than fools, in which case you increase your risk. Or whether there are more fools than money, in which case you need to reduce it”.

You really can’t sum up the contrarian ethos much better than this. When there is more money than people doing dumb things with money, there is great opportunity for investors. And when there are more dumb people doing dumb things with money, it becomes a very risky world.

Those statements are certainly true as they go and cleverly put. But there is a missing component to it that perhaps goes without saying but really exacerbates the contrarian challenge in all of it: Those periods where fools outnumber money are not readily apparent in real-time because the fools look like geniuses for extended periods of time.

Enough of the name-calling

Now, I do happen to agree with every jot and tittle of what is written above and feel the ethos of what Botz wrote is profoundly true and important. But partially because we live in a sensitive [snowflake?] culture and partially because I hate the idea of anyone perceiving me wrongly, I want to make sure people understand that the word “fool” here is being used as a general catch-all term. One who makes a bad investment is not a fool in the literal sense of the word. One who gets caught up in a shiny object may have made a foolish decision, but the point is not to pile on. I am borrowing Botz’s nomenclature because the point is that there is an indisputable reality in history that I don’t think can or should be ignored, even if it requires some harsh conclusions.

The whole premise of contrarian investing is basically a pretty harsh premise: The masses end up being wrong a lot! The greed/euphoria and panic/fear cycles that lure in human beings are a by-product of human nature. Contrarianism is the belief in investing according to this rule of human nature. Can those who fall prey to it be called fools? I would argue only in a non-personal, abstract, generic way. Every individual is a human and deserves better than to be insulted for their possession of a human nature.

But is human nature, especially when it comes to this law of investing, often foolish? Sadly, this is all too obvious.

Wheat from Chaff

Investing is the deployment of capital for the achievement of risk premium that comes from future cash generation. Cash generation can service debt (interest and principal repayment). Cash generation can represent profits that equity owners have a claim on. Cash generation can be rents or royalties from owned real estate or intellectual property. But investing is the return one gets from the risk premium in such forecasts of future cash generation. There can be multiple variables and layers, and it can be quite complex, but fundamentally, investing is the realization of a return for the risk one took to invest in a future cash generation (debt, equity, real estate, etc.).

When we talk about “fools” in the above paragraphs, we basically talk about that poor soul who knows not the basic definition of investing. We talk about those who have decided thousands of years of laws of nature no longer apply. We talk about those who are prone to listening to their friends, a chat group, bar talk, or peer pressure more than the fundamental realities of math, science, logic, business, finance, and economics.

We do not mean “those with a different opinion.” One can believe ABC is going to do well, and another can believe XYZ is going to do well, and though one may be right and one wrong, they only become a fool if their rationale for ABC or XYZ is separated from the laws of the universe.

A claim on a “bored ape yacht club non-fungible token” is, shall we say, hard to rationalize in a rational world with rational arguments. Rank speculation, hope, and crowd-surfing are not that hard to identify. Bored. Ape. Yacht. Club.

The recent history of euphoric busts all share the same things in common: A casual willingness to ignore common sense in pursuit of a speculative return. From TheGlobe.com in 1998 to housing in Barstow in 2005 to Chinese reverse merger UPOs in 2011 to solar SPACs in 2021 to crypto in 2022, they all possess the same four realities:

- A willingness to suspend logic, analysis, or traditional wisdom, and some prima facie explanation of why it wasn’t as crazy as it seemed

- A popularity that soothed the suspension and added emotional confidence to the speculation

- A period of looking like a genius while other “fools” joined the party

- A spectacular bust that left capital destruction in its wake

Do not ignore that point #3

What I referenced in my opening section above is the key piece here. If someone said my Uncle’s new tricycle company is going to be bigger than Tesla and made stock available for sale and everyone laughed at the folly of it, there would be no reason for me to write about this. But what if, for an entire year, my Uncle’s tricycle company passed Tesla’s market cap? This is where the rubber meets the road in contrarian investing … It is not enough for you to believe others are being foolish for a period; you yourself inevitably have to look foolish for a period; it is unavoidable.

Now, I myself would rather look foolish for not owning something that ran up then crashed than I would look foolish for buying the hype about a tricycle company. But regardless, the law of contrarianism states that it will not be easy, that timing will be impossible, and that there will be sustained periods of time where it seems that the world has gone mad.

It takes thick skin, conviction, and a calculator.

Protest too much, methinks

One thing I have learned over the last 25 years is that there is a powerful inverse correlation between the anger with which one defends an investment and the merits of the investment. I suppose it is, again, human nature, but one with a strong conviction and coherent thesis for ownership does not need strong emotions to accompany it. One of the reasons for my heavy skepticism of bitcoin and crypto as a price-increasing investment strategy was the almost creepy zeal with which its proponents screamed (usually on Twitter) of its impenetrable merits.

I do not get emotional defending dividend growth investing for the same reason I do not choose to argue with those who say Michael Jordan is not the greatest basketball player of all time. You do you, boo. I love sharing the merits of dividend growth investing with the world, but I don’t care to argue it. I have written a book on the case, and I explain it on television, podcasts, videos, and written word all the time. It is what we do. It is who we are. But it does not require anger or emotion. Anger and emotion are what one brings to an investment thesis to make up for the shortcomings in its rationale. We have no such shortcomings about dividend growth.

Be wary of those who do not merely believe XYZ is the greatest thing in the world and that you are missing out to not own it but also emanate a deeply insecure hostility in the presentation of their case. They are trying to convince themselves, not you.

Conclusion

The intelligent construction of a portfolio must never rely upon the wisdom of the crowd and in fact, should diligently seek to avoid the madness of it.

The long-term beneficial results that come from this intelligent portfolio construction will require sacrifice along the way as some “fools,” speculators, gamblers, and charlatans appear to be outfoxing your outdated convictions about cash flow, fundamentals, and nature’s reality.

And like almost all sacrifice, the redemption that follows will be rewarding.

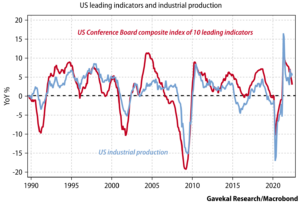

Chart of the Week

As much as we try to intelligently talk about recession possibility and ramifications (HERE and HERE), there continues to be conflicting data that makes a high conviction call impossible. Here you see that leading economic indicators, while off highs are still clearly in positive territory,

Quote of the Week

“Thus over-investment and over-speculation are often important; but they would have far less serious results were they not conducted with borrowed money. That is, over-indebtedness may lend importance to over-investment or to over-speculation.

The same is true as to over-confidence. I fancy that over-confidence seldom does any great harm except when, as, and if, it beguiles its victims into debt.”

~ Irving Fisher

* * *

I hope this Dividend Cafe ruffled no feathers. It is meant to reaffirm a principle that can not be disputed. Humans are tribal creatures, and there is nothing wrong with our hopeful aspirations. But separating the romantic from the real is the duty of a grown-up, and to that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet