Dear Valued Clients and Friends,

The market week is cut short by the Good Friday holiday this week, but investors liked what they received out of the four days markets were open. Monday represented one of the biggest up days in market history, and Wednesday and Thursday added to the rally, with the Dow now a stunning 5,500 points off its March 23 low level (which was itself an intra-day number).

No, we do not know what equities will do next week, but we do know that the Federal Reserve gave markets a lot of news this week, and that will be the primary focus of the Dividend Cafe. But if you want to understand what it all means for the economy at-large, for housing, for bond investors, and for those just sort of wondering when our country is going to re-open, we invite you to jump into this week’s very special Dividend Cafe.

Go to COVIDandMarkets.com for daily updates on the health pandemic, public policy response, and ramifications to all financial & investment markets

Two steps back, many steps forward

The market had three risks entering Thursday:

(1) Jobless claims number – they ended up being 6.6 million for the week – not good

(2) A Saudi/Russia oil deal – they ended up not having a deal until after the market closes, with a lot of back and forth and vulnerability along the way (causing oil prices to go from +9% on the day to -6% until after the stock market closed)

And, (3) The Fed announcement about their TALF 2.0 facility (i.e. “Term Asset Backed Liquidity Facility” to buy various financial assets and help ensure smooth operations in capital markets). The risk was that the TALF criteria and guidance would prove less robust than markets were anticipating and hoping for.

Well, #1 and #2 very well could have impacted markets negatively today, but #3 trumped everything else. The Fed’s TALF guidance caused a 7% rally in high yield bonds, nearly 5% in investment-grade credit, nearly 4% in syndicated bank loans, and nearly 3% in emerging markets debt.

And yes, the Dow and S&P advanced close to 1.5% to top off a week for the ages in equity markets, with the Dow up a stunning 2,700 points in the four-day week.

The Fed’s Bazooka

So what is included in this TALF facility, and what other commitments and elaborations did the Fed load into their gun(s) today? It would be easier to discuss what isn’t included, but here are some highlights:

- A facility for corporate bonds now up to $850 billion in size, with lightened criteria for inclusion (including below-investment-grade bonds, and even “junk bond” ETF’s)

- Direct municipal bond ownership (still short maturities only, though)

- Revenue anticipation notes to allow cities and states to access money on anticipated funds (from the Fed) and avoid cash flow pressures around the COVID slowdown

- A Main Street lending facility to purchase up to $600 billion of loans (with equity capital seeded by the Department of Treasury). These loans will stay 5% on the balance sheets of the banks who give them and they can sell up to 95% to the Fed.

- Significant expansion of the TALF program to include Commercial Mortgage Securities, levered loans, and significant amounts of Asset-Backed Securities which support auto loans, credit cards, student loans, SBA loans, etc.

Oil demand

We know the role that the Russia and Saudi production glut played in cratering oil prices in early March. But we are reminded frequently that this is not merely a supply issue, but a demand one as well – where too much oil is being produced for too few buyers/users. Let me put some of this into a proper perspective: before the shutdown of the world economy, the world was producing and consuming 100 million barrels of oil per day … 100 million barrels, per day. Consumption began to collapse in early March, and then Russia and Saudi decided they would destroy their own economies by adding 2.5 million barrels per day (Saudi alone) to their daily production. The “shelter-in-place” orders began to cascade the following week, and all of a sudden a “declining consumption” became a massive “excess supply” (estimated to be 25 million barrels per day at present).

But here is the problem with those numbers. Does anyone actually believe the world is never going to travel, drive, move, fly, and operate again? Those extreme diminished demand numbers reflect a present tense of 3 billion people worldwide effectively quarantined. We can debate if that will last two weeks or two months or in between, but the reality is that the demand turns back on basically instantly when people are allowed to, ummm, leave their house. Will it be back to February levels of daily consumption? Certainly not. But there is some multiple above its current demand that it will revert to – this is reasonably indisputable.

If wells shut down altogether, it will not be a matter of just “turning them back on” (like we do a light switch). Demand will come back to some degree, but supply imbalance will quickly swing the other way. U.S. production going offline in this temporal period could mean oil prices spiking above $100 in a more long-lasting period, if wells shut down altogether. Our production is that important to world supply now!

Housing prices

There are pockets of the country (identifiable by zip code) where high concentrations of FHA loans exist. As the CARES ACT has offered forbearance to those with Fannie/Freddie/FHA loans without any requirement that they demonstrate hardship, it is entirely possible that there will be significant amounts of people not paying their mortgage for the next few months. However, one thing can really stem off that outcome:

Massive education around the fact that those missed mortgage payments do, indeed, have to be caught up!

Homeowners with equity in their homes are far less likely to miss a payment (when they have the means to make it) when they do not believe they are getting free money. My belief is that inadequate education around the terms of this forbearance will lead to excessive missed payments, which risks a downward spiral for home prices where there is geographical concentration of this forbearance.

We know from post-2008 policy positioning how committed to the idea government and Fed officials are that housing prices staying elevated are a key to economic health. Treasury and FSOC are working on a plan to plug the holes caused by the COVID policy response in the mortgage market, and via domino effect, housing at large. Their plan will either educate borrowers why they should make their payments if they can, or a far, far more expensive policy solution is highly likely to be embraced by the powers that be.

Oh, about that OPEC+ deal …

After futures markets closed Thursday, the announcement finally came that ten million barrels per day would be cut from production in May and June, and another eight million barrels per day cut from July through the end of the year. And unexpectedly to me, six million barrels will be cut from January 2021 through April 2022.

The deal did not end up containing a requirement that nations outside of OPEC+ (i.e. us) also curb production.

There is talk at this late hour that Mexico is objecting to parts of the deal. So the bottom line is it all remains a work in progress, and there are significant additional meetings over the weekend that may very well generate headlines (G20 energy ministers, OPEC+ call with shale company heads, etc.).

Looking a few months out into investment markets …

No further commentary

* Strategas Research, Charts of the Week, Holiday Reader, p. 4

Everything went down, but if there was something to stick out?

Everything went down in March, but if one was looking for some “criteria” to understand, on a relative basis only, what factors most likely indicated better performance than other factors, Return on Invested Capital and Return on Equity take the cake. Free Cash Flow growth was also positive. Companies with high margins, high ROIC, and high ROE are always the types of companies one wants to own; but sometimes liquidity and especially leverage can goose returns. Not in March.

Is a “phase four” stimulus coming?

First of all, whenever a stimulus or government bill has a number after it, it always means another one is coming. But in this case, it is particularly likely another stimulus is coming because of how quickly phase three was passed, and how much it left to be done later. The overall size of the ~$2 trillion CARES ACT may be reasonably near the range needed to plug the total economic hole, but at specific targets, the levels are said to be inadequate by the powers that be.

The White House is asking for $250 billion more to the Paycheck Protection Program being administered by the SBA. Congress is said to want more funds for hospitals, state and local governments, and entitlement programs out of this bill. My guess is that both sides will negotiate now and ramp up another bill, but without a gun to either side’s head with the first bill already passed and the Fed deep at work.

Oh – and phase five? You betcha …

P.S. – My sources tell me a “master infrastructure” bill will not be in phase four, though some highway spending might be. The politics of this seem to suggest that phase four takes 2-3 weeks (more small business funding coupled with more state/local/hospital support), and phase five takes 2-3 months, with infrastructure and supply chain re-domestication being the big focuses. 2-3 months may be ambitious.

The Fed’s thinking

Are they at risk of going “too far” in this credit expansion (not merely the sheer dollar level of their created credit, but in the level of risk they end up exposing the balance sheet to, or exposing Treasury equity capital to)? Well, of course, that is a risk – especially the former category. The Fed is saying, in crystal clear English – they would rather be accused of going too far than accused of not going far enough. It is really that simple. They have embarked upon a no-stone-unturned approach, here.

Politics & Money: Beltway Bulls and Bears

- Bernie Sanders officially dropped out of the race this week … There will be plenty of time to assess the Presidential race in the summertime and beyond. For now, anyone who thinks they know what will happen in November is fooling themselves. Where the public ends up assessing POTUS treatment of the COVID pandemic and the economic recovery are both unknown at this time and both much bigger variables than anything anyone else could make up. I actually doubt anything else will much matter to the November outcome than those two things.

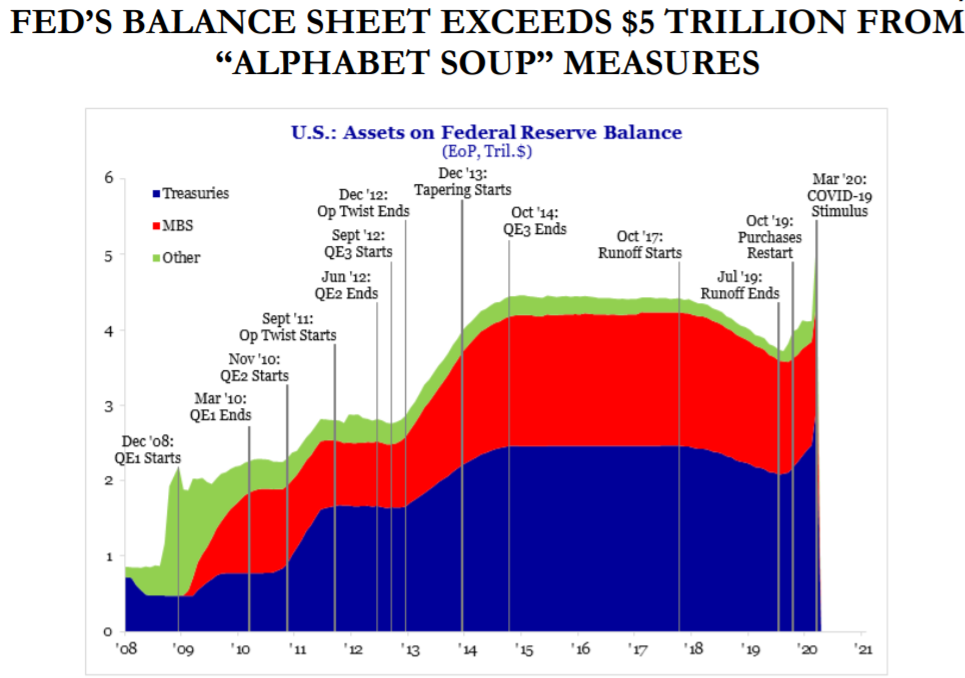

Chart of the Week

The Federal Reserve has had quite a run since the financial crisis, and the events of the last month (and the next three months) are going to make this chart look a lot different than it does now. $5.2 trillion and counting …

* Strategas Research, Quarterly Review, p. 14

Quote of the Week

“Do not cry. We were living in fear. But from now on we will live in hope.”

~ Tristan Bernard

* * *

Enjoy your families and friends in whatever way you can this weekend, and thank you for taking the time to read my weekly Dividend Cafe. It is an incredible blessing to write it for you, and I welcome any questions, any time.

I am not exaggerating when I say that today will go down in history as one of the most impactful days in central banking history.

But this weekend, we celebrate another day that was quite literally the most profound day in history.

And history has never been the same.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet