Dear Valued Clients and Friends,

I wrote a piece for the Dividend Cafe in May last year about the subject of housing and having re-read it this morning, I wouldn’t change a word. But those more evergreen principles don’t take away the appetite many have for the current state of affairs. Economic conversation right now largely centers around recession questions, and discussions about financial markets are understandably focused on the stock market. Yet right in the Venn diagram of both the economy and the market is the state of housing, and almost every person I know lives somewhere. So this topic is perhaps more relevant in a practical sense than many of the others that garner our attention.

I sometimes avoid this topic because that relevance is so misunderstood and misapplied (i.e. “if I could just know what would happen to house prices in the next few months, I would know if I should buy or rent” – or worse – “if I just knew what would happen to house prices in the next few months I could resume my foolproof home-flipping plans”). But as you shall see in today’s Dividend Cafe, our interest in the topic of housing is for a different application altogether.

Let’s jump into housing yet again, in the Dividend Cafe …

|

Subscribe on |

A volume story

A major theme of ours throughout 2022 was the slowdown in volume of home sales as a precursor to an eventual price adjustment. Candidly, we were more right than we thought we would be, as the stunning level of sales activity in 2020 and 2021 (well ahead of trendline and reasonable levels) didn’t just disappear, but collapsed down to levels last seen in 2010. Again, this simply points to a drop in the volume of houses being bought.

*Apollo, U.S. Housing Outlook, January 2023, p. 6

Not just a slowdown, a fast slowdown

That drop in sales activity I refer to is not unheard of after the Fed begins increasing interest rates (see 1994, 1999, 2004), but other rate hike cycles did not produce a slowdown in transaction volume. What we are seeing now, though, is the most decisive and quick slowdown in activity we have ever seen in the aftermath of Fed tightening, likely due to the same magnitude of high volume and low rates we saw in the last couple of years before this slowdown.

*Apollo, U.S. Housing Outlook, January 2023, p. 10

Hard to get a sale without a tour

When I say “volumes” drop before “prices” do, it is important to understand the mechanics of what is going on. The housing market is not seeing robust interest in a deal but only at a lower price; it is seeing an evaporation of interest. Prices can’t go lower when there are no prices – prospective buyers have evaporated in the landscape of higher rates, high (unaffordable) prices, and economic uncertainty.

*Apollo, U.S. Housing Outlook, January 2023, p. 15

The trend is your friend until it isn’t

Trendline growth of home price appreciation went parabolic in 2020 and 2021, and is finally seeing a weakening and early stage of reversal … A decline here to where trendline would be in 2023 had 2020 and 2021 not “bubbled” is a likely destination for median prices given supply and demand fundamentals.

*Apollo, U.S. Housing Outlook, January 2023, p. 4

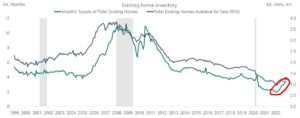

Speaking of supply

The low level of inventory that, coupled with nearly “free” money in 2020 and 2021, created the boost in prices we saw has begun to reverse. There is work to do – we remain under-supplied (especially of new product), and the Chart of the Week below has more to say on this, but that red circle below will have a lot to do with supply and demand finding equilibrium at a price level that can clear the market.

*Apollo, U.S. Housing Outlook, January 2023, p. 5

Construction on the rise

At a time of low inventory that is at least starting to increase, we do see more homes under construction now, a good sign for the supply side (to bring prices to a clearing level of affordability).

*Apollo, U.S. Housing Outlook, January 2023, p. 7

A confidence game

Declines in sales volume, declines in price, and a higher cost of capital are not merely backward-looking data points; they also influence the confidence necessary for future housing-related activity. Homebuilder confidence plummeted going into the financial crisis (“skin in the game”) and stayed in a flat trough for a few years before rallying higher, culminating in the blow-off top of 2021. Homebuilder confidence in 2022 plummeted violently, indicating some period needed to “trough” and a likely period to follow of “wallowing” in such a trough before a rebound becomes possible.

*Apollo, U.S. Housing Outlook, January 2023, p. 14

Always and forever, this

I have often said, Americans do not buy a home, they buy a monthly payment. The signs of a price correction were abundantly clear two years ago when despite record-low interest rates, affordability was at record lows. How is that mathematically possible? Because purchase prices were too high. Then, you add significantly higher interest rates to purchase prices that were too high, and “monthly payments” (aka – affordability) skyrocket. A combination of lower prices and lower rates has to bring this number down, period.

*Apollo, U.S. Housing Outlook, January 2023, p. 19

The pile-on effect

Not only, then, do higher rates, and higher prices and economic uncertainty cast a shadow over the housing market, but then financial conditions tighten in terms of availability of mortgage credit, period. Higher rates mean less qualified borrowers, and more challenging conditions mean tighter underwriting, which puts further pressure on the whole space. This chart demonstrates the challenges in availability of mortgage credit, now, with all of these combined circumstances.

*Apollo, U.S. Housing Outlook, January 2023, p. 22

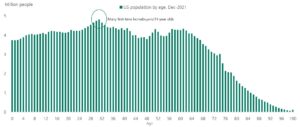

Everyone grows up eventually

As demonstrated above, we are not overbuilt in terms of supply. And as you see here, the age demographics in our country indicate a good expectation for future demand. Are there more 30-year-olds than I want there to be playing video games versus being ready to support a home purchase? Yes. But more or less, the age demographics right now are a tailwind for housing (don’t check in with me on this in thirty years; you won’t like the answer).

*Apollo, U.S. Housing Outlook, January 2023, p. 29

So where does it normalize?

At the end of the day, this is the most important chart to show. Supply is not a problem for prices, and demand is not a problem for prices. Only one thing is in need of correction.

Prices were so darn high in 2007, the affordability was brutal, and prices had to correct. But because that was on top of horrid credit quality, and houses had no protective equity, a multi-year collapse ensued, and a vicious cycle had to play out to clear the market (record foreclosures as people walked away en masse from obligations). Prices dropped enough that affordability came back, and of course, rates dropped too behind years of free money from the Fed. Now, we are back at record-low affordability, and the combination of lower prices and, at some point, lower rates, need to restore affordability … This is the process that awaits the housing market.

*Apollo, U.S. Housing Outlook, January 2023, p. 25

Macro conclusions

We have low unemployment in our economy at the moment. We have rising wages in our economy at the moment. We have a strong young adult population, and though people marry later, have kids later, and generally grow up later (all three of those things are pretty connected to one another in my experience), household formation would indicate that single-family residences are well-needed.

The argument that “investors have distorted the market” is a peculiar one, economically. A high amount of buying from institutional owners does not change the fundamental supply of who needs to live somewhere, or the fundamental demand of who wants a home. If Mr. Smith is buying from Mrs. Jones or from Jones Institutional LLC, there is no reason Mr. Smith would pay a different price with one seller vs. another. That does not change if the role of buyer and seller is reversed. And market reality is not altered if we are talking about renting vs. buying. Demonization of institutional purchases may very well fit a class warfare narrative, but it lacks economic logic.

Supply-demand reality is different in Florida than it is in California. It is different in Arizona than it is in Illinois. It is different in Texas than it is in Michigan. “Nationalizing” this conversation is not entirely helpful. Certain job markets, tax and regulatory realities, and overall quality of life considerations will matter on the margin, a lot. I am presenting a nationalized narrative because the broad subject of “affordability” as a rationale for an inevitable price correction is a national reality, not a local one. Will prices drop MORE in some places than others because of qualitative concerns? Yes, they will. And this nuance is either one you can already realistically discern, or it is one that people can use to pretend their circumstances are better than they are. But I can’t capture all those nuances in the Dividend Cafe.

Personal conclusions

I go back to the Dividend Cafe I wrote eight months ago. I do not believe this topic matters that much to one who can afford to live in the house they are living in, and who has no plans to sell. The “trading price” of one’s house is irrelevant to one who is not trading. Can there be economic knock-on effects if there is less furniture being bought, fewer appliances being bought, and less activity for those employed in mortgage, title, brokerage, and other such real estate-adjacent activity? Sure. But a 10-20% correction in prices is needed to restore those economic activities, and in that sense, a 10-20% correction will prove good.

Should someone wait to buy a home right now? That is a personal decision around timing, desire to get settled, priority of sticker price, and amount of loan-to-value (amongst other things). There is no one right answer. Here is what I can tell you …

(1) The more equity in one’s owned home, the less one needs to care about this conversation …

(2) The more one views their house as a home and not a financial asset, the happier of a person they will be …

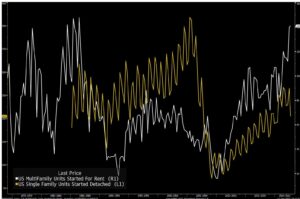

Chart of the Week

I think there is some incredible information in this chart, which does lead to some good questions about the current state of things but doesn’t necessarily provide the answers. One can see from the yellow line how absurdly overbuilt new home construction was (single-family residences) back in the housing bubble building up to 2008. That supply took many years to work through, there were vast and fatal losses in much of what had been built, and new construction/new supply has stayed way below pre-crisis levels ever since the Great Financial Crisis (GFC). But equally clear is that multi-family apartment construction had been underbuilt pre-crisis, and it recovered much more quickly and impressively post-crisis. This was due to a combination of changes in the economic landscape and cultural dynamic. Well, single-family supply has clipped lower as of late, and the question is whether or not that sets a floor for prices. And multi-family supply has surged, with the question there being whether or not we are now overbuilt in multi-family product, or rather just catching up to what has been a culturally robust demand for such.

*Bloomberg, Jan. 12, 2023

Quote of the Week

“Ignore the consensus and embrace the complexities in economics and in life. There are no single shot theories that work, no silver bullets – just perseverance.”

~ Dr. Lacy Hunt

* * *

Reach out with questions as you wish. I hope the different style of presentation this week was useful. I am off to our New York City office tomorrow, where I will be all of next week. Make it a great weekend, and please, Dallas, please, beat the 49ers.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet