Dear Valued Clients and Friends,

I’ll be very honest with you – I prefer single-topic Dividend Cafe issues. I wrote a multi-topic weekly commentary for many years before moving to a “mostly” single-topic orientation, and I have never loved writing Dividend Cafe more. I feel that the weekly information quality and value is higher with a singular focus each week, and I think the “variety” style works better in our daily market bulletin that is Dividend Cafe’s cousin, The DC Today.

But today’s Dividend Cafe is a bit different. There are a few “big” issues that people are bringing up daily, and I want to do a little multi-question fireside chat with you.

So jump on into the Dividend Cafe … I promise you’ll find something of interest, and maybe even intellectually transformative!

|

Subscribe on |

How low is too low? Let’s Talk Valuation and Earnings

I have made an argument for the eventual demise of “shiny objects” on a valuation basis for a long time. And indeed, P/E ratios have collapsed with mega-cap tech companies (FAANMG), even more so with “barely profitable” new-tech companies, and with anything else that was stretching the bounds of rationality. A lot of this is Fed-related and math-related – that is, the math of a higher discount rate bringing down the valuations of risk assets (as we talked about here). And some of it was just plain gravity – valuations got way too high, and had to come down. As most companies’ earnings themselves are up year-over-year, and virtually every company we’re talking about here has a stock price down year-over-year, the only mathematical possibility is a lower valuation.

*Strategas Research, Investment Outlook, June 23, 2022, p. 4

So this brings up two questions: (1) How low will those valuations go, and (2) What about the earnings themselves? I would suggest there is at least downside risk in both, and perhaps now more in #2 than #1 …

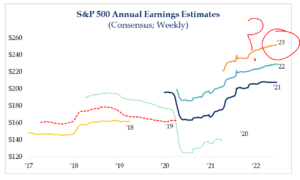

Valuations – currently, the S&P is trading at 17.5x expected 2022 earnings. That is a tad expensive, more so with a 3% ten-year bond yield than a 2% or 2.5% ten-year bond yield, but it is not a bubble anymore. Do some bear markets see 13-14x before they turn? Yes, but that is when there is a deep recession that expects massive earnings deterioration (pay no attention to people who use the multiples of 1975 or 1982 as a reference, when bond yields are north of 10%). If 16x has been the approximate valuation median for ~30 years, you could argue that valuations need to dip below their median to bottom, or reach their median, or that they end up bottoming where they are – either way, valuations either have done their damage or don’t have much more than 10-15% more downside to contribute if these assumptions hold.

Earnings – consensus analyst estimates for S&P 500 earnings currently sit at $251/share for calendar year 2023, a 10% increase over the calendar year 2022 estimates of $219. I am sorry, my friends, but that is asinine. Now, as I have written, I do not know if a recession is coming or not. I believe it is very possible, and yet I am keenly aware that there is a path by which one gets avoided. But let me just say this, if you believe a recession is here, or coming in 2022, or coming in 2023, we are not getting $251/share of S&P 500 earnings. But I will go so far as to say, I don’t believe we hit $251 next year even if a recession is averted.

*Strategas Research, Investment Outlook, June 23, 2022, p. 7

This coming earnings season will provide more guidance as to where companies are, the macroeconomic data does not suggest upside surprises in earnings, and it certainly does not reflect expanded profit margins. We got so much of 2023 and 2022 profits growth in 2021 as re-openings outperformed expectations, I simply don’t see the revenue growth necessary to get another 10% of earnings growth, and I certainly don’t see widening margins.

Bottom line: I actually believe one can make the argument that the lion’s share of multiple contraction in some areas of beaten-down sectors has taken place. It is entirely possible that contributor to price depreciation may be over, or near over. However, I would suggest that the risk will be not merely for valuation deterioration at this point, but for earnings deterioration. A compression of the rate of growth of some sectors and companies that have seen nothing but accelerating growth rates forever could be a significant headwind for the next 12-18 months. Earnings and earnings growth will soon take the mantle from valuations for how equities, especially growth equities, perform.

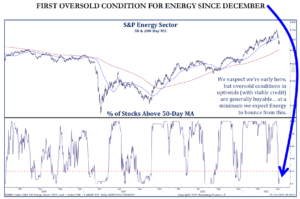

Has the Energy story changed in the last two weeks?

The broad energy sector was up +60% on the year on June 7. At press time it is now up +27% (still not bad, eh). So yes, it has given up a lot of return in the last two weeks, but yes, it is still the market star of the year (these are the reasons we trim profits within a portfolio at re-balance intervals). It has dipped below it’s 50-day moving average but remains well above its 200-day moving average.

*Strategas Research, Technical Strategy Report, June 23, 2022, p. 7

Credit spreads have not signaled any danger, and in fact have stayed much tighter than the CDS spreads in Consumer Discretionary, Communications, and other sectors. Yes, oil prices have come down to just above $100 (from near $120), but the sector is making extraordinary money at $80/oil, let alone $100/oil. A few things I would point out, some that I want to happen, and some that I do not (but all of which are rather bullish for Energy) …

- Russia is gaining ground in Ukraine, and two-way sanctions around oil and gas are almost certainly going higher, not lower

- A cut in the gasoline tax may very well benefit consumers, but it also benefits the energy sector

- There was a “sentiment” from 2014 through 2020 that the Energy sector was dead forever. That sentiment is gone and not coming back.

- There has been a cultural movement that allowed the false pretense that we can live without fossil fuels. That cultural movement has taken a big blow with gas prices this high, supply this inadequate, and Europe this unnecessarily dependent on Russia.

- There is almost surely going to be a change of party control in the House this November and there is at least a 50% chance there will also be a change in the Senate.

- An Iran deal was not able to be reached even by this administration

- Dare I say, there may even be expanded refining capacity that comes out of this moment (currently one million barrels per day short of pre-COVID levels)!

- Liquefied natural gas exports are up +45% versus a year ago, and that is with minimal export capacity (here), minimal import capacity (Europe), and practically no political support. Necessity is the mother of invention, and LNG export expansion.

I would not treat this sector as a “trade” … But if you believe in the story, I do not believe the downtick of the last two weeks is either unexpected or problematic.

Has the case for emerging markets diminished?

My thesis since I initially began investing in equities in emerging markets was two-fold:

- The macro-case: There were billions of people entering the middle class out of poverty in third-world countries and emerging economies that presented opportunity for huge economic growth as a super-cycle of production and consumption took hold.

- The micro-case: The individual companies and enterprises that operated within that macro case would have earnings growth tailwinds combined with a geopolitical and currency risk premium that made them even more attractive on a risk-reward basis.

There have been periods where this thesis was absolutely spot on, and periods where the macro was right but the micro underperformed, and there were periods where the macro and the micro were right, but that currency risk did wash out some of the returns otherwise created.

I believe both of those theses remain cogent and defensible, and there are expressions for such in both an Income capacity and a Growth capacity. However, I believe to see the returns catch full sail it will require the dollar to weaken. Do I believe that will happen? You bet. Do I have any ideas when? Of course not. The leading indicator to eventual declining Fed hawkishness will be EM outperformance. Indeed, EM has relatively held up quite well this year (meaning, in a period where the Fed has tightened and EM should be getting slaughtered by U.S. assets, EM is actually not down as much as U.S. markets are).

I don’t want to suggest this will be easy. Selection will matter. Execution will matter. It is still a bottom-up function at the end of the day (companies, not countries). But for those who have the risk appetite and room in their risk budget to amplify either the growth bucket or yield bucket of their portfolio (we call the former our “Growth Enhancement” portfolio and the latter our “Income Enhancement” portfolio), we believe emerging markets solutions will make great sense for investors in the decade ahead.

Should we be paying attention to Europe?

In a word, yes. I believe the widening credit spreads between Germany and Italy since the mere suggestion of ECB tightening over the last month or so suggests that the 10-year confidence many have had that the European financial drama is mostly behind us may, just may, have been premature.

Individual European member countries cannot afford the interest rates on their sovereign debt that the collective European Central Bank is facing. Now, they could hold rates near the zero-bound, and see their currency plummet relative to the U.S., or they could beg Jerome Powell to lighten up, but if the Fed tightens and the ECB doesn’t, the Euro gets crushed, period. And if the ECB tightens every country not named Germany sees debt service in their under-producing, under-performing, overly-indebted economy fly through the roof. This default risk gets priced into the bond market immediately (i.e. higher yields for Italy etc and lower yields for Germany), and the problem is exacerbated.

The Fed controls a lot more of how this plays out than people think. And how Fed tightening will impact systemic risk out of Europe does matter to Powell, even if he could never say so. Volatility enhancer? Probably. Default global contagion event? I doubt it. Buy the Euro? Not in a million years.

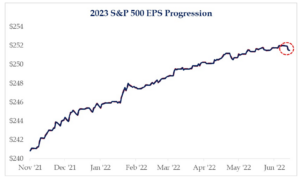

Chart of the Week

Do you think Earnings Per Share in the S&P 500 may need to be guided downward more than this if we have a recession, and if the Fed really tightens as projected?

*Strategas Research, Daily Macro Brief, June 24, 2022

Quote of the Week

“When a deflation occurs from other than debt causes and without any great volume of debt, the resulting evils are much less. It is the combination of both – the debt disease coming first, then precipitating the dollar disease – which works the greatest havoc.”

~ Irving Fisher

* * *

I hope all of these four topics spoke to you, or at least one of them did, but all are important. There will be much more to say on Earnings, Energy, Emerging Markets, and Europe in the weeks and months to come.

And now, there will be a weekend. Enjoy yours.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet