Dear Valued Clients and Friends,

I have mentioned all week how excited I am for this week’s Dividend Cafe, and now here we are. I have explained why our annual week of money manager meetings is so important before, and have written weekly recaps before as well. But this is different. This week not only comes in the midst of a bear market (as the 2008 and 2011 trips did, as well) but was also the best-scheduled meeting we have ever had, meaning, the caliber and topical significance of many of the managers and economists we were in front of was top-shelf. Combine that with a dinner with one of the true legendary CEO’s in America, and it was an absolutely tremendous week.

It also comes at a very important time. I do not mean that because stocks are in a bear market, or interest rates are rising. I mean it because of the circumstances behind both of these things, years in the making, with years of profound investment ramifications ahead. I believe a lot of perspective was gained on this year’s trip that needs to be applied to a decade of thoughtful guidance, not merely covering a month or a quarter.

I hope you will find the information shared as interesting, actionable, useful, and provocative as I do. And, of course, reach out with any questions at any time. This is the stuff we live for, and I am confident this Dividend Cafe is one you will be glad you read.

So with that, let’s all jump in, to this “money manager week recap” edition of the Dividend Cafe!

|

Subscribe on |

Hot and Cold Weather

“Climate is what you expect; weather is what you get.”

Perhaps no line will stick out to me more than that from our TBG Money Manager Week 2022. This line did not come from one of our portfolio managers but from the iconic economist, Jim Grant, who I have followed my entire adult life, and a whose annual symposium on Tuesday was a big part of our week. Jim’s point was that the Fed has decided to try and make weather with their predictions of the weather (meaning, rate policies can’t ever speak to what rates ought to be; interest rates, like all prices, are meant to be discovered, not imposed).

Why did this stick out so much? Because I believe that almost everything we are dealing with in markets right now can fundamentally be reduced to this: Interest rates are the price of time, and absent coherent rates, you make activity in a given time period incoherent.

We have spent fourteen years with a price of money not set by a calculus of risk and reward, not set by economic actors and risk-takers responding to reality, but rather by a weatherman trying to make the weather they are supposed to be predicting.

Shiny Objects are the Victims

I can blame the promoters of NFT’s (“non-fungible tokens”), the exchanges of Ponzi schemes like crypto, the buyers of silly plant-meat companies trading at 1,000x revenue, and the media-hype of things like FAANG, all I want. But these NFT’s, bitcoin, tech stocks, and all the rest did not create their “shiny object” allure – they merely benefitted from it, until they didn’t. And yes, there are charlatans out there for whom grift is a middle name. And yes, again, human nature is an easily-deceived and manipulated investor. But nothing fed the bubble of shiny objects that 2022 has blown to smithereens quite like a zero cost of capital, and the distorted valuation of risk assets that such a monetary regime has fed.

Better late than never?

Of course, one can respond to my criticism of what the 2008-2021 Fed wrought by pointing out they have now got religion; they are reversing easy monetary policy, hiking rates, purging excesses, and even doing quantitative tightening. So won’t this fix the mistakes made and push us back to something more like monetary equilibrium?

But here’s the thing – excessive accommodation followed by excessive tightening is not moderation; it is moving from one extreme to the other. A boom followed by a bust is merely two examples of failed stability. A strong and stable dollar and an environment free of distortions optimize conditions for a robust market economy. Jumping back and forth from the freezer to the oven does not get you to room temperature.

And yet, an even more important point became a theme of my week …

Quantitative Tightening Sounds Good in Theory

I understand the Fed has begun “roll-off,” – meaning, allowing bonds on their balance sheet to mature without reinvesting the proceeds. And I understand they set a $47 billion target for how much they want to “roll-off” each month, with a further target to double this to $95 billion.

I also now believe it is all nonsense. I do not think they will get the $4.8 trillion off of their balance sheet that they added since COVID began, let alone the $4 trillion they added out of the Financial Crisis.

*Federal Reserve Board website, Credit and Liquidity Programs, Oct. 19, 2022

In conversations with multiple bond managers, hedge fund managers, structured credit managers, macroeconomists, and more, the consistent conclusion (oftentimes reached from different premises or points of view) is that the Fed is incredibly limited in what it can do to really reduce its balance sheet.

For one, other countries have already shown it is easier to talk about doing than actually do (Japan, Korea, United Kingdom, etc.). But for another, our own country has already proven the same thing in the very recent years of this last decade.

Tom Hoenig, long-time Fed Governor and member of the FOMC Committee during this whole period of QE starting in our country post-GFC, spoke at the aforementioned Jim Grant symposium. He reminded us that QE1 was not called QE1 when it came out, because there was never supposed to be a QE2 or QE3 or QE4 or QE5 – we just called it QE because they were supposed to do a “one and done” of $600 billion to “stabilize housing” and “aid market functioning” back in 2009. I think that the term “aid market functioning” can be one of the scariest terms in modern finance. On one hand, a “lender of last resort” is at the heart of central banking, but on the other hand, “aiding market functioning” seems to lack a limiting principle, and can go to a place of real distortive intervention before you can see where your $4 trillion went.

Anyways, Hoenig pointed out that QE2 was really an admission that markets had become dependent on QE1, and QE3 was an admission that QE as a policy tool might be able to do more than just “aid market functioning.” Then, in late 2018, the Fed re-introduced QE right as they were supposed to be tightening the balance sheet because of liquidity challenges in cash markets. But they didn’t call it QE; they called it a reverse repo facility; but it was QE by another name, because they were stuck. And THAT is the exact same condition in which we find ourselves now.

That the Fed then went into a QE binge post-COVID is another reflection of the monetary mentality in which we now live – aggressive interventions lacking any semblance of an exit strategy are normal, status quo, and it would even be considered dangerous if we didn’t have it.

Getting our criticism straight

I was relieved to see someone of Hoenig’s intelligence reiterate what I have been screaming for many years. “The primary concern from QE was not and is not inflation – it is the distortion of asset prices and downward pressure on productivity.”

QE is a problem – a huge one – but it is not the source of price inflation we saw in the last 18 months. Rather, a +1.1% productivity rate throughout the decade of QE vs. a +2.3% productivity rate the decade before, is.

Alphabet soup not coming to the rescue

Reverse repos are offsetting “quantitative tightening” now, and the Fed has no way to reduce the balance sheet when cash is leaving the banking system and heading to cash markets. What appears to be a pending stressor on the idea of the Fed leaving the bond market is inadequate purchasers of U.S. debt. Now, higher rates cure a lot of that, but the Fed will not tolerate the term structure being this high once they are ready to see the lower end of the curve come down. Quantitative Easing is the drug they know the best, and have most access to.

And I am firmly predicting that this time is no different. Zoltan Pozsar (former Fed economist, Senior Advisor at the Treasury Department, and current head of Global Rates at Credit Suisse) reminded us of the permanent reality of monetary policy – plans get disrupted by reality all the time. QT may be their plan; the reality of the situation is different.

With the yield curve, inverted hedging is very expensive, and that means a lot fewer FX players in the market, and a lot less financial market purchasing of Treasuries for what would normally be organic market activity. Further elimination or reduction of market buyers of Treasuries enhances the need for central bank purchasing of the same. The Fed will soon face the same thing Japan, the Bank of England, and the European Union have all been forced to admit: They created a scenario where they can’t leave QE behind.

Summing up the Fed stuff

(1) So I don’t believe QT is going to really happen much.

(2) And I do believe QE is going to come back, first in camouflage, then without a disguise.

(3) I do believe the terminal level for the federal funds rate is coming at the end of 2022, and that a long pause, then actual rate reductions, will follow.

(4) I believe that Volcker is credited for bringing down inflation because:

- The inflation then was far more monetary-oriented than it is now,

- His actions were coupled with world-changing supply-side incentives from marginal tax reductions to deregulation, and

- Energy inflation was organically turning down after massive investments in oil and gas rigs; we are dealing with the opposite.

Therefore, I believe comparisons of Powell to Volcker are fallacious, and that not only are the men different, but the circumstances themselves, are.

(5) Our focus on interest rates as a tool to manipulate growth is wrong, and our focus on rates now as a tool to decrease inflation is wrong, too. Interest rates, above all else, put a price on time and a price on anxiety. Disrupting that misallocates capital, it distorts valuations, it destroys savings (which erodes investment), it screws up pension funding, it causes yield-chasing, it enhances economic fragility, and it alters healthy economic activity by incentivizing engineering vs. productivity.

Other than that, it’s a great idea to mess with the price of money.

Attribution and Retribution

I really unpacked much of this last week, but let me get into more detail on the challenges facing indexers in the decade ahead.

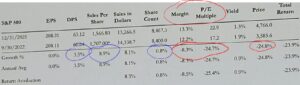

2022 is an easy story to tell, even if it is a weird one. Dividends are up 3.5% on the year, sales from S&P companies are up +8.9% on the year, and the share count is down a little (more earnings to go around with less shares from buybacks). Yet, margins are down -8.3%, and more significant than anything else, the P/E ratio on those $208 of S&P earnings is down -25%. So there you go.

*Semper Augustus Investment Group, Attribution & Retribution, Oct. 18, 2022

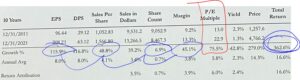

But let’s look at the same thing for the last decade. How does the S&P 500 go up +363% with a total increase of sales that were not even +50%? Well, you got a 6.9% decrease in total share count, so that’s a little something (less shares to divide up the earnings), and the profit margins on those sales increased a stunning +45% over that time, so profits were up +116% in a decade. +49% sales gets to +116% profits with greater margins and less shares. Easy enough. But how do you get from +116% profits to +363%??? Well, you see the valuation go up +75% in that same decade, that’s how.

*Semper Augustus Investment Group, Attribution & Retribution, Oct. 18, 2022

Let’s say we got a 50% increase in sales over the next decade, the same extraordinary 50% increase we got over the last decade (I think I am being generous since we were coming out of the mother of all recessions ten years ago, but I’ll play along). At a 15.5x multiple on the S&P, with the same profit margin percentages we have now (which will be nearly impossible), with the same reduction of share count we had over the last decade (which is really optimistic), you get to a flat return for the S&P.

Am I predicting a flat return for the S&P over the next decade? No. Maybe sales beat expectations a tad (it would only be a tad). Maybe the multiple is higher than that (it could be). Maybe margins improve (I am starting to stretch). But my point is that if you turn knobs to the best-case scenarios, it is really hard to get more than a 2-4% annual return for the broad index without going back to a 22-25x multiple as we had a year ago when interest rates were 0%.

A little down. A little up. Flat. Up and down in between. But not historical returns, and not anything like the decade we just had.

Multiple expansion giveth. And multiple contraction taketh away.

P.S. – For what it is worth, if someone put a gun to my head, I would take the over in that range of forecasts. I can easily see a bunch of variables lining up positively over time (with plenty of gyrations along the way) to deliver something slightly above these scenarios. But my point is this – the key word is “slightly” – and it requires so many things to line up perfectly. It is simply not a cogent philosophy to rely on purely passive index movement when one breaks apart attribution.

Naked in the low tide

The last decade has not provided clarity on who has talent and who does not in the world of levered loans, high yield, and direct lending. $5 trillion more corporate credit exists than did at the time of the GFC. How does that not cause every one of us to pause and reflect? Does it mean everything is terrible and the world is ending? No. People who throw out a big number just for shock value and without any argumentation as to why it is supposed to be bad are intellectually dishonest (or perhaps just deficient themselves). But the big number does, at least, reinforce the seriousness of what I think now represents the challenge.

Much of that money was lent to really good borrowers, for really good (productive) purposes. Some of it was not. Whether it be the high-yield bond market, the syndicated loan space, or the avalanche of new direct lending, there has been a lot of credit extension that represent a lot of good investment opportunities, but also some bad.

Private Credit is a complicated space that allowed everyone to look like a genius in a period of financial repression. Now the tide is coming down, and it behooves investors to be far more discriminating than they have been.

To that end, we work.

Did someone say strategy? A few specific areas across asset classes

In our “boring bond” portfolio, we are well aware that liquidity and quality are now paying investors quite nicely without a need to sneak up the credit curve.

In our “credit” portfolio, the overweight in Floating Rate relative to High Yield has served us well as rates have climbed. And now an overweight in High Yield relative to Floating Rate will do the same as credit quality will matter more in the next phase of the economic cycle, and the bulk of the rate increases are behind us.

When it comes to private credit, and real estate within our “Alternatives” sleeve, the caliber of underwriting matters, discipline around deal flow matters, and growing cash flows trump pie-in-the-sky assumptions about cap rates, any day.

On the tax-free side of “credit,” we are more bullish on High Yield Muni than almost any other asset class. Though even the “boring bond” side of muni has history on its side.

*Invesco Asset Management, Oct. 2022

The decision to view “Growth Enhancements” outside of the world of shiny objects has been one of the best decisions we have ever made (including selling our very large ARKK position quite near its all-time high, about 73% ago). Emerging Markets and Small Cap are down as well, but not nearly in the same range as the more popular “growth strategies du jour,” and we believe are the right forward-looking asset classes to play a risk-on environment. We are going to eliminate one of our small-cap strategies inside our Growth Enhancement portfolio and increase weightings to the other small-cap strategy and to our Emerging Markets strategy.

We are potentially consolidating strategies in our Structured Credit exposure, and are conducting a review now as to whether or not are heavy allocation here benefits from our current use of two hedge funds.

Private Equity continues to be a favorable asset class in our Alternatives exposure, and we have found exactly the right evergreen solution from exactly the right sponsor to optimize exposure in this space. We also have found a quality “multi-asset” solution that combines Private Equity, Credit, and Real Estate from a quality sponsor we are anxious to partner with.

Chart of the Week

I really hope this one speaks for itself:

*Voya Investment Management, October 2022

Quote of the Week

“We cannot and ought not to restrain by legislative enactments the marvelous energy of this nation and the natural course of things; but we ought not to administer an artificial stimulus.”

~ Albert Gallatin, 1841

* * *

I did a 24-page document summarizing all my notes from the trip for our Private Wealth Advisor Group. I hope this summary is more digestible and useful than that. Should you have any questions out of this, do not hesitate to ask.

The Fed was a source of enhanced volatility before this trip, obviously. But what I think I most appreciate now, more than I did two weeks ago, is the innumerable legs that come out of that. So many aspects of investment markets are impacted by the monetary regime in which we find ourselves. We are determined to be diligent, studious, and careful, in all the things that matter around us.

To that end, we work.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet