Dear Valued Clients and Friends,

The title of this week’s Dividend Cafe comes from one of my favorite quotes, ever.

“It ain’t what you don’t know that gets you into trouble. It’s what you know for sure that just ain’t so.”

~ Mark Twain

(I attribute to Mark Twain because everyone does, but ironically given the substance of the quote, even this appears to be untrue, with most scholars believing there is no reputable source for who quoted these exact words).

The underlying message here is never more relevant than in investing, it seems to me. Plenty of people don’t know certain things, and that has some impact at given times. But I am quite convinced that far more damage is done, not at the things that are that people don’t know, but the things that people believe to be true (and act upon), when in fact they are not.

This week’s Dividend Cafe is going to be dedicated to several examples of just this.

I do imagine every reader will pick up a little something in this week’s Dividend Cafe, and some readers may very well have their world turned upside down. I also imagine some may take exception to some of the points I seek to make. All of these outcomes are perfectly okay with me, so jump on in to the Dividend Cafe …

Gold as a Hedge against Government Irresponsibility

This one is perhaps one of the more important ones because it is so well-baked into the consciousness of so many well-meaning people. “I own gold because I worry about the government getting out of control.” It is not the latter part that I take issue with; it is the conclusion that gold has represented the antidote to those various bouts of government excess and imprudence. My view is that gold has proven to be a non-sequitur to this challenge – more sought after for sociological and marketing reasons than historical realities.

It would be hard to imagine a decade of more monetary and fiscal irresponsibility than this last one (so far). Even if you defend all the Fed has done (I can certainly defend some of it), the point is that the last ten years have been filled with extreme monetary experimentation, to say the least. The Fed’s balance sheet has blown out. We spent most of the last decade with the Fed Funds rate at 0%, and only slightly above it when it was above it. Fiscal deficits have been extreme, to say the least.

Yet despite all the projections of the dollar’s demise, it remains the world’s dominant currency, with none even remotely close to filling the gap between second and first place. Inflation remains stubbornly low for Fed purposes. And here is the primary investment point I would make – Gold is basically flat for over a ten-year period (less than 1% per year since the beginning of 2011). QE1, QE2, QE3, Operation Twist, ZIRP, $25 trillion+ national debt, three COVID stimulus packages totaling $5 trillion, QE4, $7 trillion Fed balance sheet, corporate bond purchases, TALF 2, $15 trillion of global debt trading at a negative yield – truth be told I could add five paragraphs of “things” if I wanted to get into the full granularity of what has gone on just in the last ten years of our country.

Yet, Gold is basically dead flat for a decade.

*Bloomberg, Joe Weisenthal, April 5, 2021

Inflation and Government Spending

I almost feel guilty even throwing this one because I have been so obsessed with it all year (why a blowout in debt is deflationary, not inflationary), and yet I simply cannot ignore this subject given how widespread the misunderstandings are here.

When I devoted two Dividend Cafes to this earlier in the year (part one here and my favorite – part two – here) I didn’t do so because everyone already saw this issue the way I did – I did it because it was and is a widely misunderstood issue. So I am being redundant here, yet don’t believe the pure empirical reality of this subject can be absorbed without a lot of repetition and committed conviction and consistency.

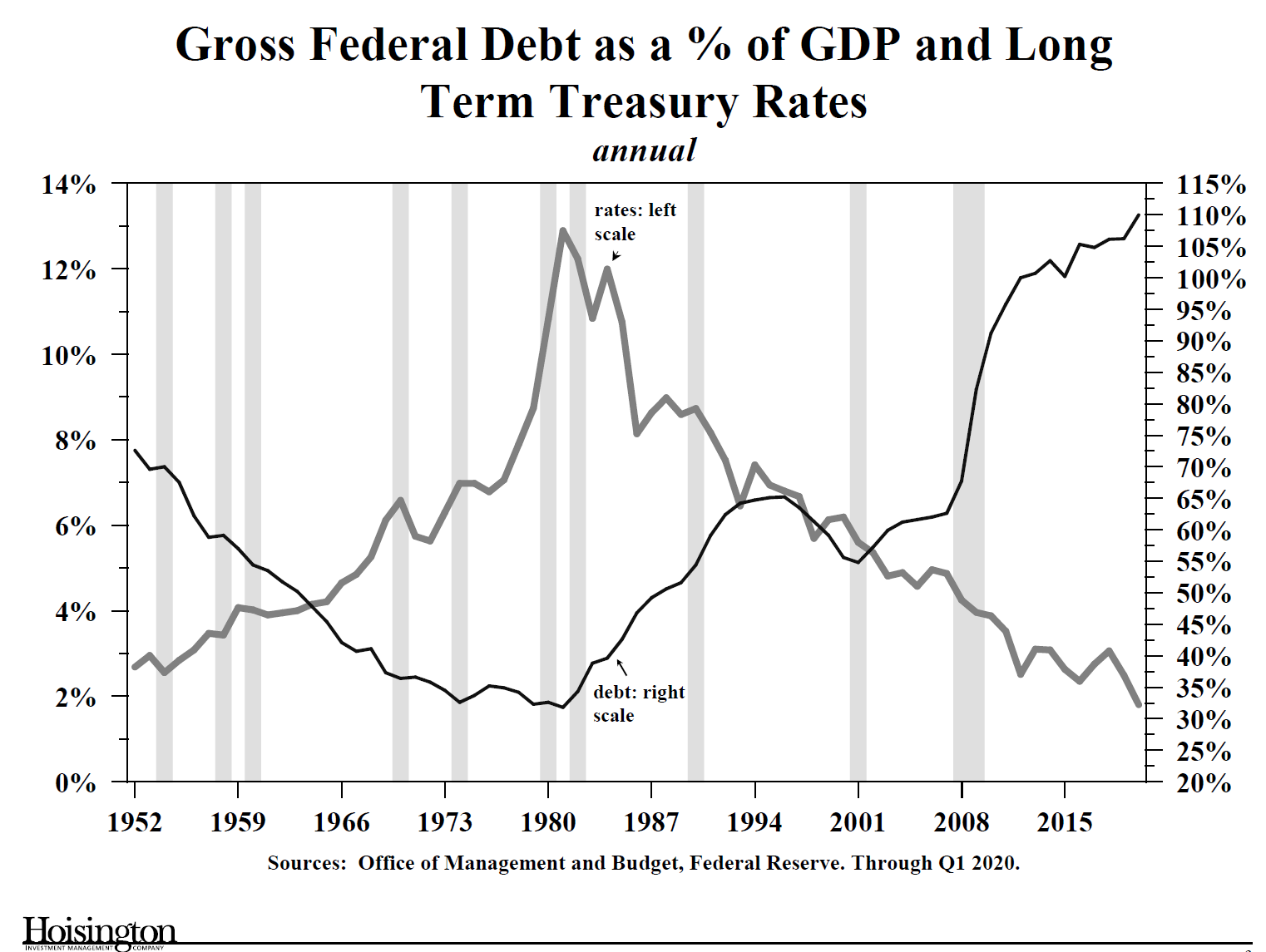

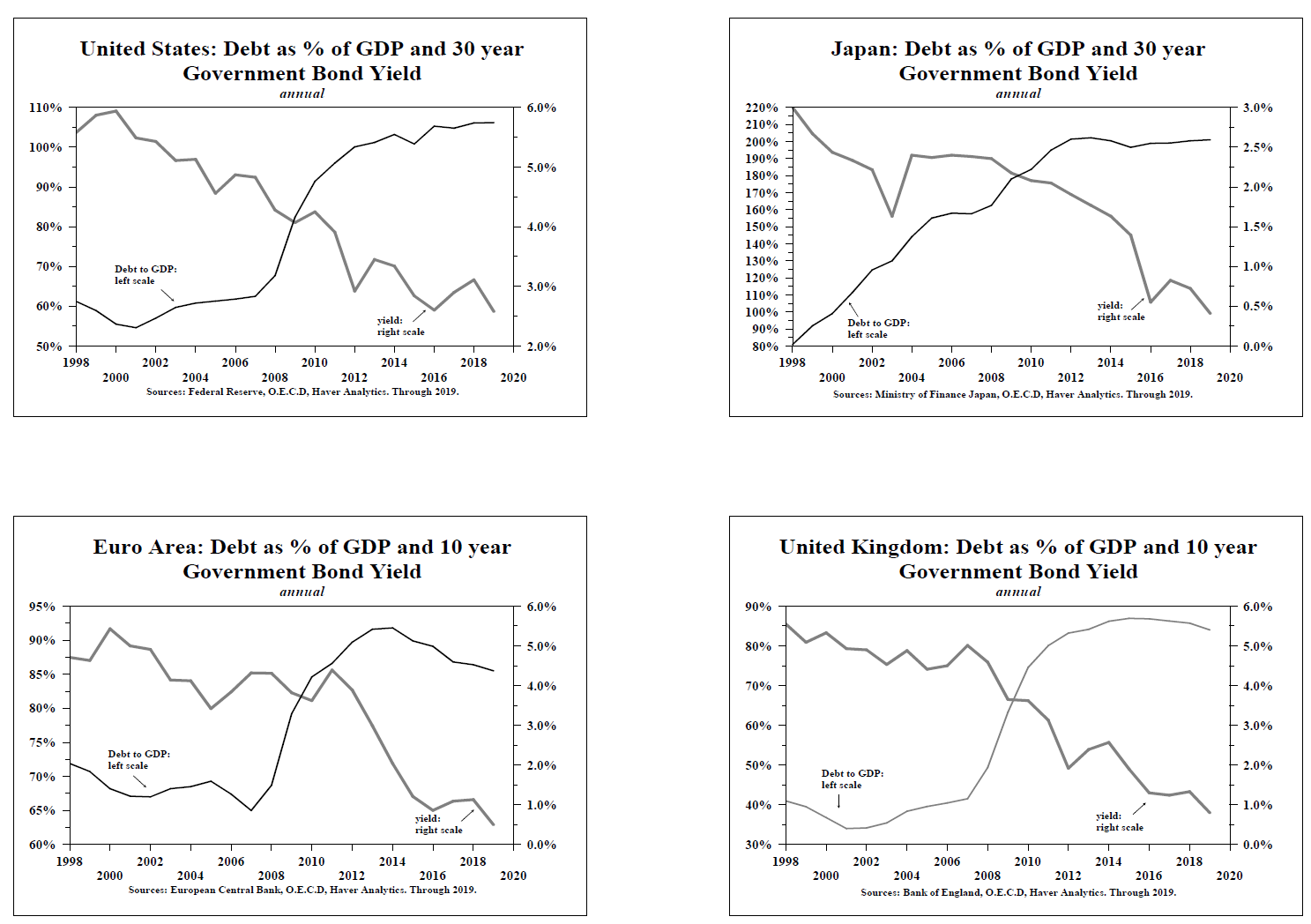

We have seen an explosion of government debt for decades, and we have seen no correlation between bond yields (which price in inflation) and the direction of that debt. The economic impact from excessive debt is treated with more debt, and more monetary stimulus, which then creates the negative feedback loop that keeps velocity of money from forming – of real organic growth from happening – and it holds interest rates down even further.

One of my favorite charts on this subject is this little quadrant here, where the United States, Japan, the United Kingdom, and the European Union are all shown together over the last thirty years, where all four major global economic zones see their debt exploding, and all four see their interest rates collapsing. If the consensus understanding of this subject were correct, the line that goes from the top left to the bottom right in all four boxes would basically be on top of the other line, from the bottom left to the top right. But rather, these two lines form an X – they are inverse of one another – for the very reasons I am stating.

*Hoisington Capital, Lacy Hunt, Q2 2020

Growth and Value Merely Alternate who is leading

The truth is that there have been periods where both were up a lot, only one was up a lot more than the other (value over growth in the 1980s; growth over value in the 1990s). And yet there has also been a period where value outperformed dramatically, only because value “held ground” while growth got killed (2000-2008).

The misnomer here I would highlight is (a) Any belief that one has ever held dominance over the other for more than a decade, but also (b) The belief that we are only talking about one hitting singles while the other hits triples; in fact, strikeouts happen, too.

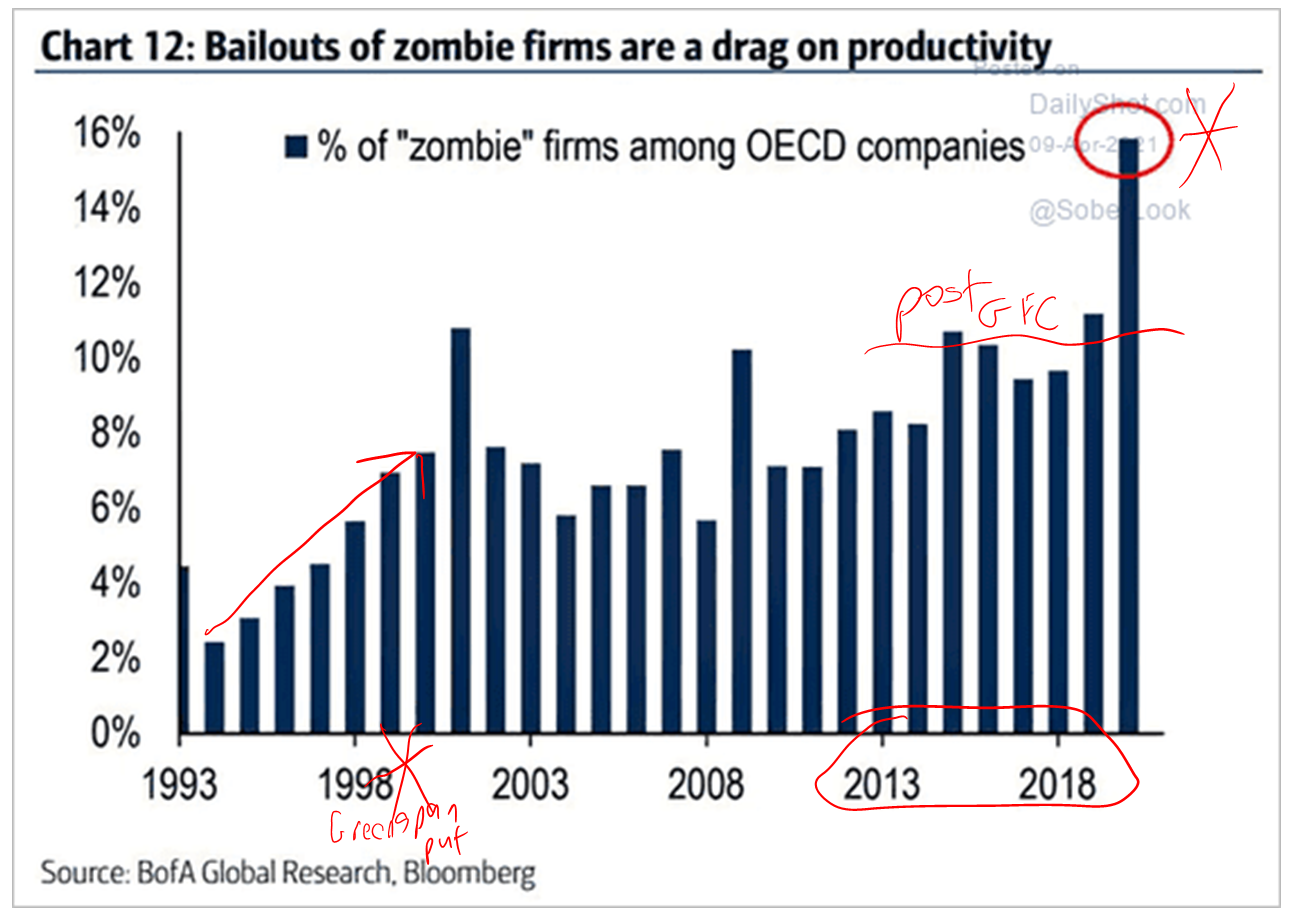

Helping the economy by supporting dead businesses

It is so often said one of the great things for the economy with periods of low rates and high financial repression is that companies which otherwise would fail because they do not make enough money to cover their debts are able to succeed. High financial repression (policies that result in loans available to companies at rates below their natural or organic level) helps companies avoid their fate – namely, that point at which their cash flows are less than the cost of servicing their debt, or, that point at which principal reduction is needed (and yet funds are not available to do so).

It sounds understandable at first glance to assume a company avoiding bankruptcy or failure or job losses is a good thing. And for a short period of time, it can be. But what is missed in that calculus is that significant resources get “stuck” in a company that is just running in place – being artificially propped up against the real forces of the marketplace. This means there exists sub-optimal allocation of resources, and less productivity throughout the economy (i.e. those resources of labor and capital being held in a sub-optimal business are therefore not being released to new projects and opportunities that would be more productive).

So in this case, we bite off our nose to spite our face. We avoid the pain of short-term job loss and company liquidation, but we endure the long-term pain of a sustained drag on productivity – the very thing holding back our economic growth (and therefore job growth and wage growth) for over a decade now!!

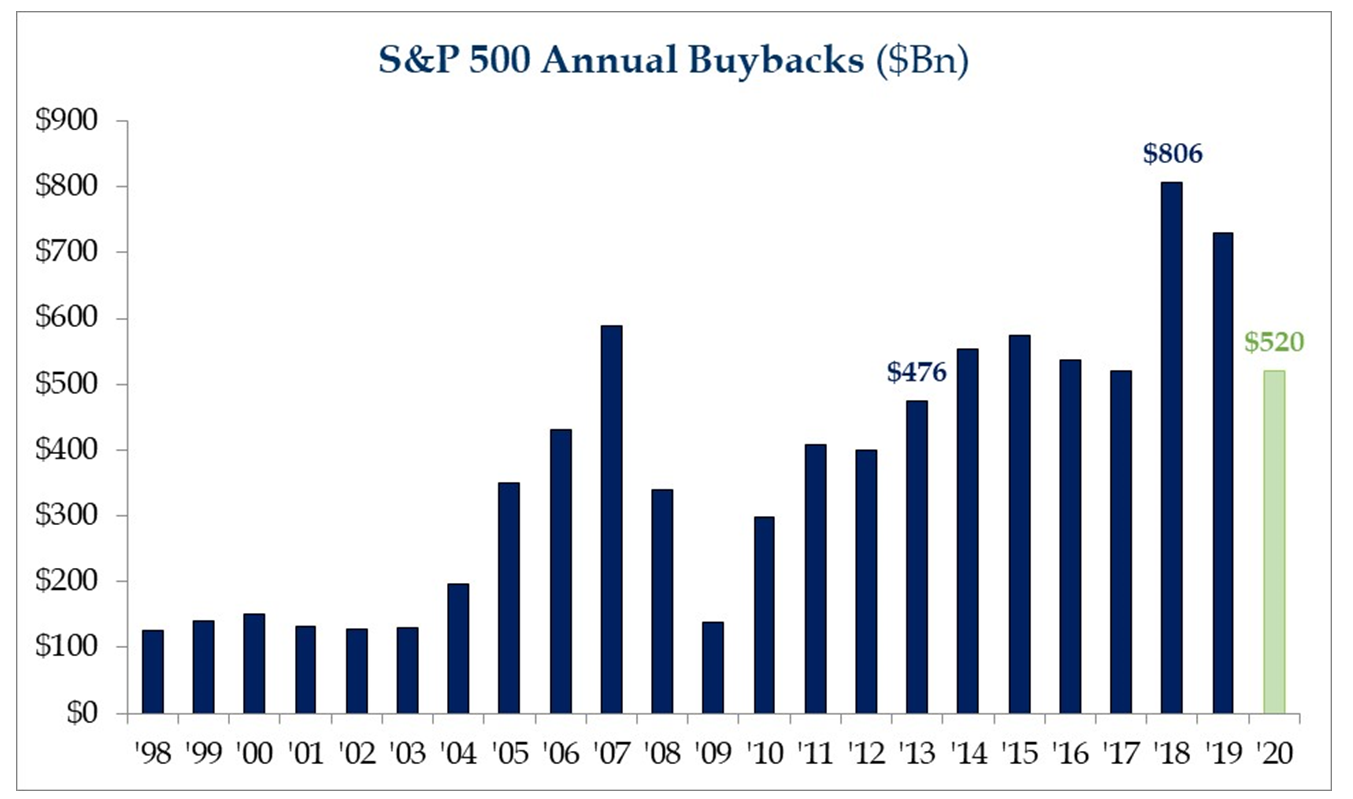

Stock buybacks are better than dividends

Stock buybacks and dividend payments are simply two competing options for what a company can do with its after-tax profits. They are options on the menu for capital return to shareholders. We see dividends as de-risking and monetizing the investment for shareholders, and certainly providing consistency to the investor. Share buybacks do not result in tangible fruit for income-oriented investors, are often not executed even after being announced as authorized, and at various stock price levels prove to not be well-priced or well-timed.

Additionally, many times stock buybacks are not actually returning cash to shareholders, but are offsetting the new issuance of shares needed for executive and employee compensation (this is significantly the case with technology stocks).

The two can and usually do co-exist, but there is no doubt in our mind that dividends are the more shareholder-friendly mode of capital return.

Economic collapse from a 2% interest rate?

I don’t know if 3% is the right number or not, but I do know the hand-wringing over 1.5% bond yields suffocating economic growth has been one of the silliest things I have ever seen. Just post-GFC, let alone most of post-WW2, we have been in a period of 2-3x higher bond yields in the 10-year.

Chart of the Week

One of the [many] points we often try to make regarding stock buybacks in terms of their efficacy in benefitting the financial fortunes of shareholders versus the benefits of dividends is that share buybacks are the first, and easiest, thing to pull when “the going gets tough.” Dividends entrenched into the history and culture of the business model of a company are far less volatile for the shareholder.

*Strategas Research, Daily Macro Brief, April 9, 2021

*Strategas Research, Daily Macro Brief, April 9, 2021

Quote of the Week

“Should an investment narrative become particularly disputed, the best course of action is to identify the camp that is more emotional, and bet heavily against them.”

~ Jim McClure

* * *

I know this week’s Dividend Cafe was a little out of the norm, but I thought the material important. I really could have delved into many more examples, and perhaps those will find their way into these pages in the weeks and months to come, but I hope this gave a little taste of where I see a lot of misunderstanding in the investing landscape.

Certainly, reach out with any questions or thoughts on your mind (that open dialogue is always encouraged). And in the meantime, have a wonderful weekend. Earnings season launches next week, and you know how much I love earnings season.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet