Dear Valued Clients and Friends,

I have been surprised by the level of interest in my treatment of the “China investment” subject in recent weeks. I kicked things off at the beginning of August with this piece, presenting the background around the tensions between U.S. investment in Chinese equity vs. Chinese fixed income. I followed up with this piece making the case that the Chinese perception of U.S. global economic intentions (primarily around our use of the dollar as the world’s reserve currency to facilitate large twin deficits) is at the heart of Chinese beliefs and agendas with their own currency.

None of this has been for the purpose of mere armchair theorizing or navel-gazing. While high-level takeaways in the discussion of China’s place on the global economic stage can be interesting and even provocative, our agenda is investment-specific. We may or may not have an investment thesis to act upon around Chinese financial markets. And we certainly believe the entire discussion is highly relevant for all investors in terms of how the geopolitical and monetary components play themselves out.

Put differently, there will be no investor who gets to ignore China. None. Even if one says, “I want a 0% weighting in Chinese investments,” everything I am discussing around currency, trade, interest rates, the relationship between the U.S. and China, deficits, regulation, technology, and so much more is profoundly important to a U.S. investor. Indeed, I wonder how people think the world’s most valuable company would function if the production and consumption of its products were entirely divorced from China? You get the idea.

This week I bring in some reinforcements. Louis Gave of Gavekal Research, one of the foremost economists in the world when it comes to China, Hong Kong, the Pacific Rim, and global fiscal dynamics joins me for a podcast/video discussion on this entire subject. His own views help shine a light on what the fundamental question is we must answer. I will leave you in suspense as to what that is.

But beyond the discussion with Louie on the podcast/video, I veer into a number of different considerations in this week’s writing that I believe are not only fascinating but vitally important.

Once again, all free people can conclude different things about these subjects. But choosing to ignore the entire topic is not an option. History is being made right before our eyes, and our portfolios are asking us to understand it. To that end, we work.

Mutually Assured Widgets

Americans needed cheap products and someone to fund our deficits for many years (we still do). China needed to sell exports and needed to receive dollars for their excess foreign exchange reserves for many years (they still do). There was a clear case of respective economic goals (even unstated ones) being met by the other party, even if no one wanted to consider us economic partners (let alone friends).

We can debate if the ancillary realities of this economic arrangement were worth it – and many people do just that every day. My only point is that we had it, whether it is convenient to acknowledge this arrangement or not. Each country had an itch (or two) that the other country scratched.

The next phase of this relationship

Those dynamics have largely sat at the center of the first 20 years of this new century. What do the next twenty years hold? American sovereign concerns are a low cost of capital to finance exorbitant deficits and national debt (i.e. low bond yields). Chinese sovereign concerns are a greater role on the global economic stage, giving it a tremendous incentive for higher bond yields and a more stable currency.

That may be far too simplistic of a summary but at a headline level, it captures where we are just to start this discussion. The U.S. has both an agenda and a need to punish its savers and bond investors for years to come with low yields (and indeed, negative real yields). China has the need and agenda to do the opposite – to drive an incentive for foreign countries to transact in renminbi.

Out of this basic thesis comes the beginning of our inquiry.

If only it could be this simple

The easiest way investors could analyze the deployment of their hard-earned capital should always theoretically be where the growth is. I don’t care if we are talking about equity, debt, or currency reserve, tell me where the growth is going to come from, and that’s where I want to have my money. This is the economic truism that even radical redistributionists intuitively know when you catch them off-guard. The cosmic wealth pie of the globe is not fixed. Human action expands the pie through something we call “growth.” Prosperity comes from the glorious process of value-added productive activities – and where there is a lot of that going on, capital benefits indiscriminately (debt, equity, etc.).

So it would be nice to just say “hey, there is great growth here” or “wow, growth is really stunted here” and make some investment decisions around those realities. But countries have a funny way of never making it that simple. Countries with strong secular trends and growth tailwinds often decide to use the powerful force of anti-growth regulations to rain on their own parades. Some countries do all they can to hamper their own growth but have such a powerful DNA for growth they can’t help but succeed (you live in such a country). Others do the opposite – they can’t help but snatch defeat from the jaws of victory if you will.

Inconvenient growth stories

You could argue that all should be splendid for Chinese growth. They came out of COVID with much less damage than other countries. They have experienced unprecedented growth and innovation in much of their technology and internet sectors. The world continues to need their exports and they have all the leverage in the world as the globe fights supply disruptions all over the place.

Yet their growth has been anemic. They have cracked down with a vengeance on their own tech and internet success, choosing to make this moment the opportunity to teach a lesson to their best and brightest about the importance of “national service” over commercial success. They have shut down much of their economy around COVID, not dealing with a population willing to fight back at the imposition of their personal liberties (to say the least).

On the flip side of this, U.S. growth was supposed to grind to a halt. A year ago the country faced unprecedented contraction of economic activity with many predicting that no American would ever shop, dine, or fly again (okay, maybe those weren’t the literal doom and gloom predictions, but they were pretty close). I would suggest that those making those predictions have never met an American, but I digress. The reality of the COVID moment has been a tragic redistribution of national income and wealth, but no pause in economic growth at all, and in fact, a significant surge of activity out of the lockdowns that reflected the pent-up demand in our system. Despite concerns about COVID, taxes, spending, regulation, and more, growth has been solid – at least for now.

Inconvenient cultural realities

One concern I hear a lot is that China’s system of government, its suppression of human rights, its lack of free speech, its hyper-regulation of the economy, its shaky system of private property, its demonization of entrepreneurs, etc. all point to a culture incompatible with a good investing environment. And I would simply say that regardless of what the exact paradigm is for equity and bond investors in China around these dynamics, I am in complete agreement that China’s marriage to technocratic Communism and repudiation of democratic capitalism is a disaster. A moral, political, and economic disaster. I couldn’t fall into the trap of defending these things in China for all the tea in Japan.

But allow me to make a point. If greater crackdowns on tech is the problem, further suppression of religious liberty, calls for more and more regulation, a strong move for government control of banking, a media that functions as a mouth-piece for the state, interventions in the property rights of landlords, etc., etc. – is there a region where we are encouraged? NOW, I fully, completely, totally get that the absolute level of these things in the United States, for example, are far superior to where they are in China, for example.

But the cultural reality for FUTURE investment is that China has a cultural bedrock that is priced in, where many western democracies are going in the WRONG direction, but DO NOT have their destination priced into their capital markets.

Food for thought.

Some key distinctions

I do not like the rhetoric I often hear about the entrepreneurial class in the United States, and I find extremist class warfare to be unbecoming in a country of our DNA. But I do not believe a robust private sector is going to be marginalized any time soon in America. We have people that talk that way but lack the power to bark where they bite. In China, they have the bark and an even greater bite. I do not trust the CCP around corporate and entrepreneurial interests. I recognize that risk may well be priced in, but I think there are other fish in the sea.

Populism cuts both ways

For good or for bad (or for reasonable people, a little bit of both), no one can deny that there has been an upswing in populism in the United States the last five years or so, and in fact, an upswing in populism in most western democracies. But what cannot be ignored about the dynamic playing out in China right now is that they have their own forces of populism to contend with. Populist sentiments may seem less relevant since they carry very different electoral forces in China than they do in America, but anti-American sentiment is rising on the mainland – no doubt about it – and I cannot see how this does not add fuel to the fire of both the national security position and the economic position China may choose to take.

Tough reality

One can take whatever view they want on the prospects for investment in China – whether it be direct ownership, U.S.-listed Chinese companies, or even Hong Kong companies. But I would suggest that those worried about the reliability of the Chinese government have far, far, far more exposure and risk through most American multi-national companies with large presences in China than anything else.

The view that one wants a China-free reality may be smart, dumb, moral, immoral, thoughtful, silly, or whatever – I am not (for my purposes here) telling you what to think about that. What I am telling you is that it is not possible and that the more wants to China-free their portfolio, the less American multi-national exposure they can have.

The greatest foreign policy leverage that China has over the United States is through the U.S. multi-national companies inside China.

China’s ability to crack down on their own internet companies for their own Marxist objectives is one thing. Their ability to crack down on our tech companies for their foreign policy objectives is another.

Currently Speaking

The currency story is crucial here and I believe the points Louis Gave makes in the podcast/video are extremely important. The thesis is not that the PBOC does not intervene in their currency while the Fed does intervene in ours; the thesis is that the PBOC’s interventions are driven by an entirely different policy objective.

Conclusion

To generate the wealth it needs to be a prosperous and leading nation China is highly dependent on its exports, more so than any country in history. A dependency on exports means a dependency on trading partners, and the more trading partners China can have and under more favorable conditions for China, the better.

The single greatest leverage they have to effect this is a superior currency and bond market that attracts foreign capital, sovereign capital, and ultimately, allows their currency to elevate on the world stage.

I suppose they could go invade Taiwan, too. But I ask you – in what world is that not going to impact ALL investors?

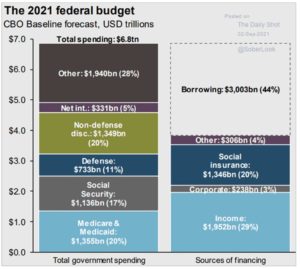

Chart of the Week

I had a different chart I was going to use this week, but just before press time, a friend of mine in NYC sent me this chart. My email back to him was that this chart is actually extremely connected to today’s topic.

If one thinks that we can maintain our foreign policy objectives in China, Taiwan, or the Middle East with defense as a mere 11% of budget, I have a belt and road to sell them.

But ultimately, the broader economic picture is simple: Our national P&L requires downward pressure on rates until kingdom come. And that is bad for the dollar, bad for fixed income savers, and bad for capital formation. Without savings, you don’t get investment and without investment, you don’t get growth. China, suffice it to say, is not borrowing 44% of their government outlays.

My chief policy and economic advisor, Larry Kudlow, tells me all the time – one of Ronald Reagan’s favorite things to say was that strength overseas had to stem from strength at home. A strong economy IS a matter of foreign policy. The CCP may not read the Dividend Cafe, but they know everything in this chart. They know the heck out of it.

*The Daily Shot, Sept 2, 2021

Quote of the Week

“Modern China needs to maintain Deng’s approach to economics but must achieve

Mao’s outcome of a united China. China’s national strategy is odd in that China is a great power that must concentrate on economics — and it has been thrust into an economic and military

confrontation with an important customer and major military power. China’s strategic goal must be to disengage from this position while preserving national unity.”

~ George Friedman

* * *

I wish you all a very happy Labor Day weekend, a time of reflection on this Dividend Cafe, a time for college football, and most of all, the presence of friends, family, and FREEDOM. The bedrock of prosperity – freedom.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet