Dear Valued Clients and Friends,

Late in 2006 I was running a practice at UBS Wealth Management and using their equity management team out of Chicago for a lot of my equity management services. I would go to Chicago and meet with them at least a couple of times a year and found the process collaborative, informative, and intellectually engaging. But all of my other money manager relationships were in New York City, so when UBS asked me to go to speak to their new advisor class in November that year (in Weehawken, NJ, where their operational headquarters are that they inherited from the old Paine Webber), I decided to schedule a few meetings with other portfolio relationships. I was only overseeing $100 million at the time, 4% of the assets we manage now, yet it never occurred to me that I may have a hard time scheduling appointments.

As a pure aside, this trip double-dipped as a recruiting trip for another major Wall Street firm who was pushing me to join them in the opening of a new Newport Beach office for their firm. I met with their legendary CEO, a fellow named Ace Greenberg, and heavily considered their extremely flattering offer. The name of that firm … Bear Stearns. In March 2008, they would be dead and gone, sold to the loving arms of JP Morgan for $2 per share (from over $150). Suffice it to say, I didn’t join them after those enticing meetings. God was watching.

Anyways, I ended up meeting with a few managers on that trip and became convinced that I would become a smarter investment manager by more regularly meeting with the brain trust of the portfolio strategies we partnered with for the betterment of our clients. By 2007 I had joined Morgan Stanley (the winning suitor in that aforementioned recruitment effort), and I was growing my business quickly. I not only was meeting with managers I had a pre-existing relationship with but was seeking new partners in what was a new firm, a new menu, and certainly now a very new market as the subprime market had broken, credit conditions tightened, and the world sat on the precipice of what would be the greatest financial crisis since the Great Depression less than one year later.

Back then I was meeting with 6-8 managers per day, and a client for dinner every night. This was well before I had opened an office out here or taken an apartment in the city. They were long and grueling and exhausting days, but I got introduced to new portfolio strategies, met world-class investment talent, and escalated the level of due diligence we conduct as part of our regular process at The Bahnsen Group to new levels.

The following year was one for the ages. I wrote all about my living through the financial crisis at the ten-year anniversary two years ago (and still commend this reading to you). But there was very little time to meet with a competitive floating-rate bank loan fund to the one I was then using when we were literally making history day by day with the extinction of more and more iconic financial firms, the world’s credit markets were hanging on by a string, and my own firm (Morgan Stanley) was fighting for its survival. The then worst day in markets since Black Monday took place on this trip in 2008 (several days in the COVID month of March replaced it on a percentage and point basis this year) when TARP was initially voted down in the House. I sat with hedge funds, credit managers, and of course my staple of dividend growth intellectual firepower, and pondered the future of the universe.

The trips changed my life in 2009 and several years thereafter, literally. Not only did a few bond managers and hedge funds and somewhere around their private equity strategies bring me inside their secret sauce, but I committed after the financial crisis to be the most mentally and intellectually engaged financial advisor in the country. Though the mantra of “never forget” after the 9/11 attacks were really the by-product of a lesson that had to be learned geopolitically, ethically, and for the national defense of our country, there was a sort of “never forget” moment after the GFC as well (great financial crisis). The vast majority of my peers did not know what the hell had just happened and were fine with it. They knew markets blew up, and they knew markets were in the midst of recovering; but they did not truly understand why markets blew up, why they were recovering, why their own firm had flirted with extinction, and what risks and realities warranted a deeper appreciation into the future. I wasn’t content to not know. I was thirsty for knowledge, but I also was committed to a mantra of “never forget” applied to the GFC. To this day I consider some of the meetings I had in this New York money manager due diligence trip of 2009 the most important meetings I ever had in my career.

I am not claiming that I became something special out of these trips – I don’t think that, and I don’t believe these trips are anything more than what every single financial professional who gets paid to manage client money ought to do. Over the years the access to portfolio talent has increased, the discernment on who we meet with has gotten better, and the menu of meetings has expanded (not just money managers but analysts, research boutiques, trading floors, entire asset management platforms, and so much more). There have been years of strong epiphanies, broad portfolio changes, manager terminations, manager hirings, and occasional milestone experiences (dinner with Ben Bernanke, private round table with Steve Schwarzman, and too many more to count). And yes, there have been meals. Steak, Italian, Chinese, Sushi, French – because when in the greatest dining city in the world …

Brian Szytel began joining me on these trips in 2014, and Deiya Pernas became a staple in 2015. By then we were fully formed as our own business entity, The Bahnsen Group, with our legal, economic, and brand identity independent and disconnected from Morgan Stanley. We now had a fully open architecture around our alternative manager relationships, and we had the ability to solidify truly custom and special fixed income strategies. Our highly bespoke custom SMA with Voya was borne out of these trips, as was an old exchange-traded note with Miller-Howard that led to us ringing the bell at the stock exchange. Fun times. But also, really special solutions driven by an insatiable desire to be better, to be different, and to actually care. To that end, we work. Never forget. It’s all true.

In early 2017 I opened an office in New York City, initially sub-letting from our partners at Hightower Advisors before getting our own Sixth Avenue spot a couple of years later. In late 2019 we took on new expanded office space to truly call our own at the Graybar Building at Grand Central (Lexington and 44th, if you are ever in the neighborhood). We now have the conference room and offices to host meetings, and of course, as is the case for all of midtown, can walk in less than 20 minutes to trillions of dollars worth of asset management headquarters. We believe in #NewYorkTough, but we also believe in #NewYorkSmart, and there is nothing like the brain trust of idea generation and thought leadership encapsulated in the ’40s and ’50s between Third and Seventh Avenues in this glorious city. It is infectious – the good kind of what that term means.

Anyway, this was a particularly important year for us. Some managers experienced surprising outcomes in the COVID March moment that have required real diligence and monitoring. As we have been talking about ad nauseum as part of our Operation Magnify process, the realities of credit and boring bonds being co-mingled were no longer acceptable for us on either a risk or reward basis. And when it comes to the entire liquidity of a portfolio, risk endurance, and correlations to equity-like circumstances, there is nothing like a 36% drop in 31 days out of the government response to a global health pandemic to truly test what you own, how it is structured, and who you are partnered with. The 37 meetings I had by Zoom and phone since March with various managers were all fine, but they were not what this trip is for – the truly intimate process of sitting face to face with those you have entrusted client capital to, and affirming if what you know is still what you know. I mean it when I say it is not just intellectually gratifying; it is morally obligatory.

The COVID moment has caused a fair amount of people to more or less lose their minds, and give way to a degree of irrationality and incoherence in some personal decision-making that I probably ought not to comment on much beyond that. But many managers are back in their offices here in New York City. Some came back just to meet with us this week (and I mean, several did that, seriously). Some are working with 20-50% of employees in, and at least one structured credit manager and all fifty of their employees – every last one – were back in their office at 54th & Madison – in person, sanitized and energized, ready to bite the [blank] off a bear, as the old saying goes (read: Liar’s Poker). God bless them for it. The city needs them back. It needs every0ne back. It’s time. But I digress.

It is one thing for us to recognize that Boring Bonds are not going to return the same portfolio result to investors for years to come that they have in the past; it is another thing to do the work to change what your strategy around Investment Grade Corporates (IG’s) and Treasuries (T’s) will look like around that reality. It is one thing to separate Credit from Boring Bonds in your portfolio construction, but it is another thing to truly, thoroughly vet the strategies that will make sense for your Credit exposures (tax-free high yield, bank loans, securitized credit, junk bonds, EMD, etc.). A highly intensified on alternative income solutions for the future may sound nice, but to develop the right platform relationships necessary to create your own custom structure for such takes a lot of work. Finding the right idiosyncratic strategies to fit within such a structure must be a part of a diligent and careful process. Asking hard questions of your hedge fund relationships or tax-free bond managers is more impactful when done in person. It invites candor, transparency, understanding, and it creates the conditions necessary for advisor-fiduciaries to make the decisions they need to make on behalf of their clients.

All of these things and more were on the menu this week. Our business is better off because of the meetings we had this week, and our clients will experience better results because of it. We truly believe that.

The aftermath of the Great Financial Crisis did change me as a person and as an investment professional. Some of the great behavioral lessons were evidenced in the advice I gave during the March COVID moment. I have a much more keen sense of what “national margin calls” are and how not to behave during such de-leveraging episodes. A lot of the technical realities of these phenomena are things I learned on the trading floors of these manager locations in NYC. But apart from a better understanding of the technical mechanics of markets, I also have a paradigmatically different view of conviction than I did pre-GFC. All of the advisors at The Bahnsen Group do, as well. There are no willy-nilly, half-assed, barely-confident commitments to our investment philosophy at The Bahnsen Group. We are all in. You need that during good markets. You need that during bad markets. And you really, really need that during collapsing markets. Good, bad, or worse, there’s never a good time to go wobbly in our world. (I am using that expression more frequently as of late; our world misses the great Prime Minister).

I confess that I do not care in a given quarter or given year how much the stocks we own in our dividend growth portfolio go up or down compared to the stocks inside a random market index, but I hardly think that is a profound confession. I have been screaming it for years and years now, and it is the moral and cerebral takeaways of experiences like the financial crisis that taught it to me. Investors do not achieve financial success over a lifetime by racing against something else that has no common ground with their goals or life situation. This is barely an argument that should have to be made, it is so obvious. Investors have a lot of nuances in their financial lives, a lot of particulars, a lot of liquidity needs, a lot of variance around their comfort levels, a lot of curveballs in their investment lives. Investors have glorious joys in their lives and unfathomable personal tragedies, and those things change aspects of their optimal portfolio.

Investors are people, they are not abstract baskets, and they invest because they want to have the instrumentation of cash as a means to producing the end of contentment. Now, I am well aware spiritually, emotionally, and psychologically how untrue it is that financial peace and prosperity assures contentment. You likely are, too. But I also am aware that those other categories of our lives that do influence our contentment are not what people hire me for – it is just the financial one. I can talk to any client, any friend, any person, any time – about their dreams, hopes, fears, and lives – but my advice in most categories will lack expertise, except the financial one. That is what we do, and that is why people hire us.

And for my money, and your money as well, there is nothing I believe will more consistently and substantively generate financial peace and prosperity for you than adherence to a philosophy that is goals-driven, that is planning-driven, and that seeks consistency in implementation. Chasing hot dots and fads and momentum is a path to destruction and ruin (whether you are an individual playing with your family’s fortune, or a Wall Street firm leveraging generations of capital by 40-to-1).

Any portfolio that never under-performs is going to blow up, badly. Part of a properly diversified portfolio is the assurance of under-performance. Something in your portfolio should always be under-performing. Math, logic, and science dictate such. I could elaborate on this, but I think it is obvious. Email me directly if you want me to spell it out more, as I am happy to do so.

The takeaways this week have been deep and wide. Yes, I think we have found an incredible new high yield tax-free bond manager. Yes, we feel more clarity on what we are doing with Boring Bonds. Yes, our Real Estate portfolio managers have exceeded expectations. And yes, we have really conducted the deep dive we needed into the juicier parts of our Structured Credit portfolio, and come away with a better understanding of the non-agency RMBS and CRT market.

But we also completed this week totally energized around the things we believe in, the macro matters that are really driving markets for years to come, and the principles we tediously share because they are so important. Whether it is Dividend Growth or Structured Credit, we don’t think anyone can consistently buy low and sell high; we believe they can secure growing cash flows and invest in the attractive and sustainable creation of such. Whether it is small-cap equity or emerging markets, we don’t believe anyone can consistently predict what stock prices will do one week versus the next; we do believe some can understand and identify growing earnings streams with defensible business models.

So thank you, New York City, for another year of education and growth. And thank you, our dear clients, for allowing us to have a purpose to this great intellectual journey. We are tirelessly committed to your financial well-being. To that end, we work.

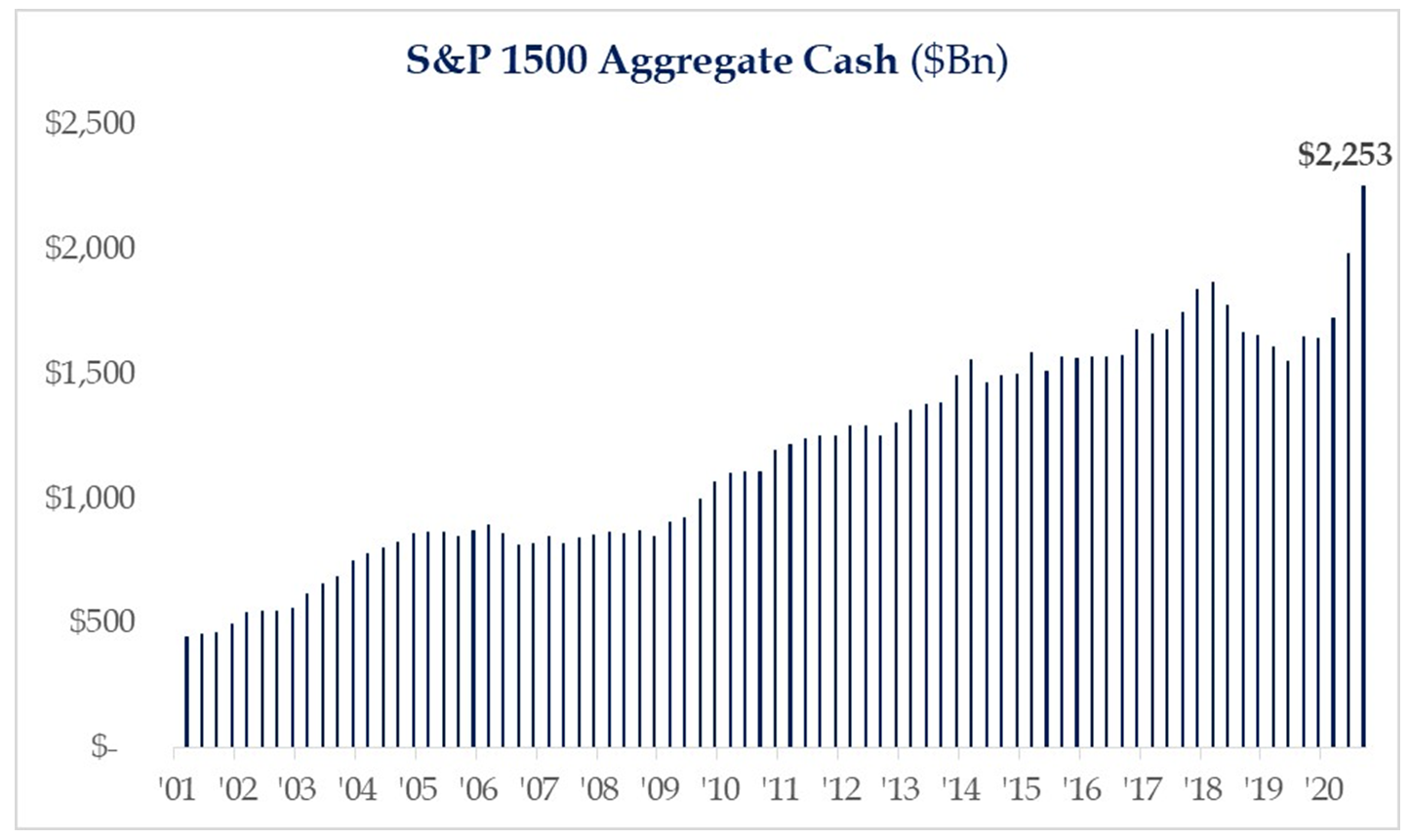

Chart of the Week

I really believe on this crux hangs so much of what will happen with markets into 2021 and beyond … We know there is record levels of cash on company balance sheets, and we know much of that is from debt issuance done in 2020 with emergency low rates and high access to liquidity. What we don’t know is what companies will do with those funds – will liquidity be needed for ongoing management through this period?; will they buy back shares?; will it work its way into CAPEX and business investment? How this cash is deployed will prove to be a significant part of the market story that is to come.

*Strategas Research, Daily Macro Brief, Oct. 14, 2020

Quote of the Week

“No one can bar the road to truth.”

~ Aleksandr Solzhenitzen

* * *

Thank you for bearing with this somewhat unconventional Dividend Cafe. And thank you for believing in the tenets that make us who we are. I hope this has given you some glance into our story, and I invite any questions or comments you may have. Enjoy your weekends, and be free.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet