Dear Valued Clients and Friends,

It is so hard to stick to my normal Dividend Cafe format these days (not that anyone cares). I am trying to write two per week, and the markets are changing minutes after certain segments get written (or more challenging, the news itself alters or stories take on different shapes). On two days this week (Monday and Thursday), the violence of the market drops required additional email communications. Clients receive their special bulletin specific to portfolio holdings on Wednesday, as well. The state of affairs now makes the exact timing and precision of these communications difficult. We hope you understand.

I set it up that way because there are things in flux right now as I type that by the time I submit to my team may change, and by the time you read this may change again. I apologize for that. But that is the state of affairs in which we find ourselves.

My feeling is that the market this week went through a Black Monday type day (October 1987). On that fateful day, we dropped 22.6% in one day (and it did rebound 6% the next day). This week, going into Friday morning, the market is down 18% in four days (and as I sit here in type from a Starbucks on 47th Street at 5:30 am eastern, the market looks set to open up 5%). So while the violence was four days, not one, and 23% is a lot more than 18%, there is still the same feeling of shock and horror and the rapidity with which this all happened.

I am dedicating this week’s Dividend Cafe to what happened this week, what has to happen from here for markets to (a) normalize, (b) begin recovery, and (c) finish recovery. It is a long one, but hopefully easy to read and useful to your understanding and thinking about this crisis.

Week in Review

As we know, markets dropped over 2,000 points on Monday as the Russia/Saudi oil war exploded over the weekend, and as continued COVID-19 issues swept the markets. The market advanced nearly 1,000 points in a bounce-back Tuesday, before going negative on the day, before then closing up over 1,150 points. On Wednesday, the market gave all of that back and then some (down 1,500 points), and on Thursday, the leg down became simply surreal, dropping 2,350 points (10%) in a single day. I hesitate to even mention that the futures are pointing to a 1,000 point increase (+5%) on Friday morning, both because it could change by the time I am done writing, and because each of the three or four 1,000+ point days we have had in recent weeks have not indicated additional big down days were behind us. Nevertheless, no matter what plays out Friday, this has been a brutal week in the stock market.

Summarizing the week with Maria Bartiromo on Friday March 13th

Where are we

The sweeping impact across society of event cancellations, school cancellations, “work from home” orders, and so forth have created the feeling of a society on lock-down. March Madness (NCAA basketball) has been cancelled. The NBA and MLB are suspended. The SxSW event in Austin was canceled. The significant pullback on activity is going to have a profound impact on the economy, and no one knows the duration it will last. This is a key statement, because the markets have certainly priced in a very negative outcome here (as markets always do with uncertainty), and the range of potential realities to American life range from 2-3 weeks of heavily depressed activity to even 2-3 months.

This is important and will determine much of how we think about this in the months to come, because there are two scenarios we believe are totally feasible yet dramatically different from one another:

(1) A painful and huge depression of activity for 2-3 weeks that dissipates when health data and reports dramatically improve, and containment and low impact become more evident. In this “best case” scenario, GDP is hammered in Q2, but the lost activity stays “pent up,” and Q3 sees a massive resurgence in GDP activity.

(2) The health epidemic and fear depresses activity for months, and Q3 becomes a lost cause economically. In this case, a recession is inevitable, more headline news rattles markets, and we see ongoing challenges economically.

And it must be said – many outcomes exist that would be considered “between option 1 and option 2.”

Our view is that there is a 25% chance of option 1, a 25% chance of option 2, and a 50% chance of “in between.”

And it is very difficult to speculate what the market has thus far priced in, but it most certainly has far, far over-shot option 1.

Talking w/ Charles Payne on Thursday March 12th

How to think about COVID-19 as an investor

I do not mean the big-picture, evergreen, timeless principles that we advise on all the time which actually are more important than anything I am about to say (have I mentioned lately that dividends will reinvest at lower prices for accumulators and dividends will continue to pay and even grow for withdrawers of capital?). In this section, I want to facilitate a framework for the major categories relevant to investors around this entire escapade:

(1) Health Care policy (basically, how is containment going, and how is the development of a therapeutic and eventually a vaccine going)

(2) Oil price war (collapsing oil prices around temporal global demand suppression, and now the geopolitics of Russia/Saudi)

(3) Monetary policy (will the market respond to the Fed’s settling of some form of zero-bound interest rate, plus other liquidity conventions)

(4) Fiscal policy (what combination of targeted relief, spending, and even tax cuts are coming to offset the present tensions)

My interest here is not to advocate for some policies versus others. I have been quite explicit in these very pages about what I believe regarding the real efficacy of monetary accommodation here. My interest is in assessing what investment markets want or are looking to in order to optimally handicap all that is happening.

This week we saw the following:

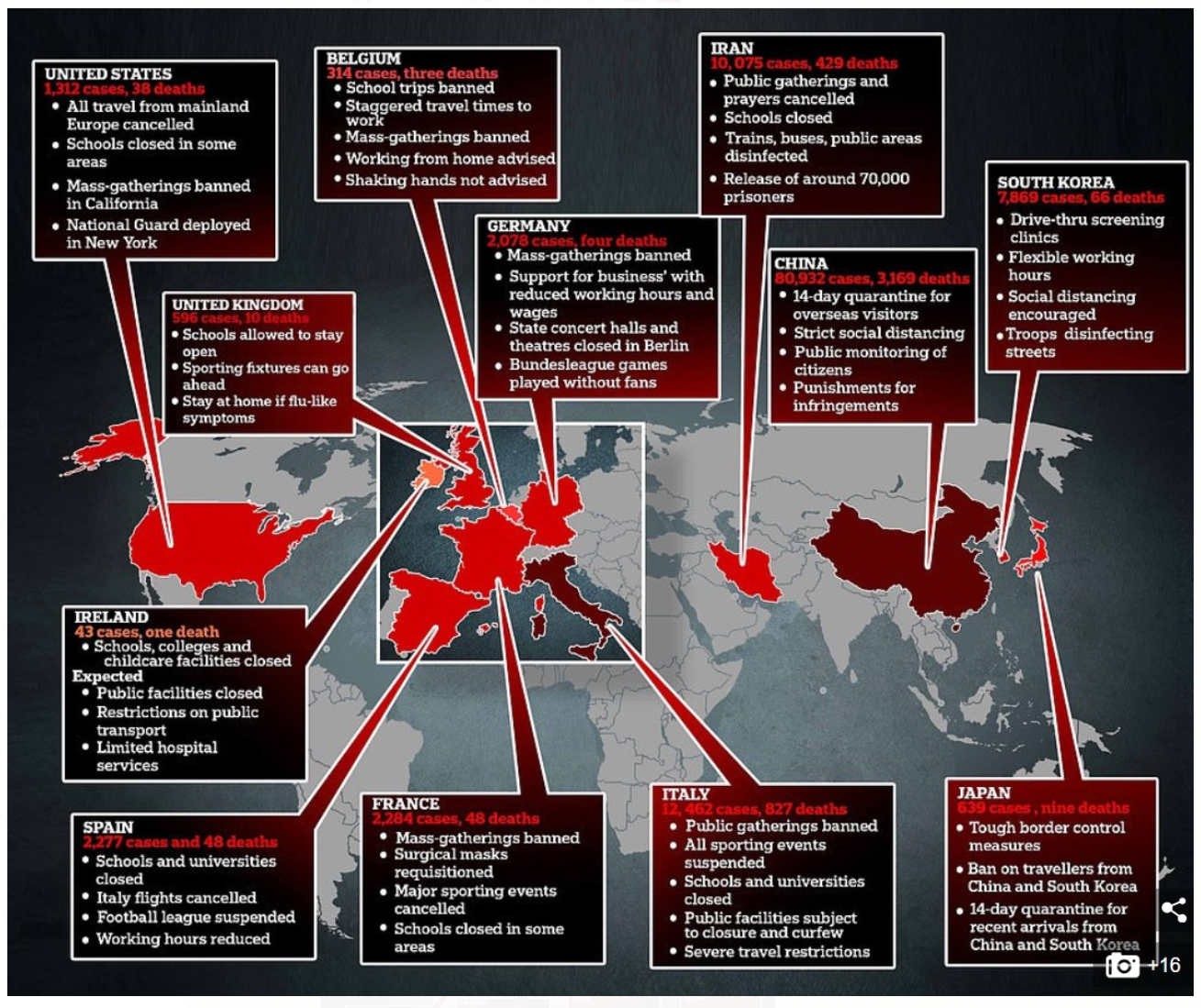

(1) Health Care policy – the Trump administration announced a ban on travel from Europe to the United States. He did so without consulting at all (or informing) any European authorities. The violence in Europe’s markets transcended ours, which added to U.S. market tensions (margin calls, forced selling, broad panic, etc.). A large part of the country has cut off most public events. Testing capacity is supposedly increasing. Cure rates remain very high; mortality remains very low; and the profile of who is most vulnerable to this remains very consistent.

* TS Lombard, March 12, 2020

(2) Oil price war – oil prices dropped 30% Sunday night when Russia rebuffed Saudi’s request to curtail production in concert, and Saudi responded to that by saying they would flood the world with more oil. Prices came off their lows Monday and stayed in the low-to-mid 30’s all week from there (vs. mid-to-high 20’s).

(3) Monetary policy – the Fed announced $500 billion of repo transactions Thursday afternoon (adding to money market liqudiity), and said they will continue such through the end of the month up to $1.5 trillion. Futures markets are pricing in a 75% chance of a 0% fed funds rate in the week ahead and a 25% chance of a 0.25% rate. The rate is currently 1-1.25%. So the overwhelming implied probability is that short term rates will be back to the zero bound that we were at from late 2008-2016 in the coming days. More to say on all of this below …

(4) Fiscal policy – as of press time, no deal has been announced. I was in the west wing Wednesday with the National Economic Council and saw first hand the range of policy proposals being sent from the White House to the Hill. The issue is, of course, that Nancy Pelosi and the Democrats have the leverage (i.e. votes), and it is taking time to get the White House and Democrats into a more agreeable place. The President announced a $50 billion funding increase to the SBA (Small Business Administration) to assist businesses who suffer from COVID-19, but the bulk of what is being discussed (payroll tax holiday, movement of April 15 tax deadline to mid-summer, sick leave federal funding, etc.) will require a joint deal between the White House and Congress (not to mention Senate approval).

Where these four things need to go

Health Care Policy

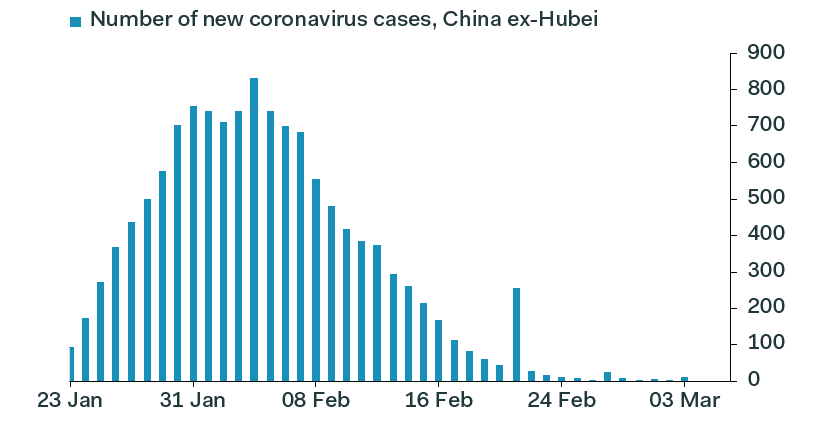

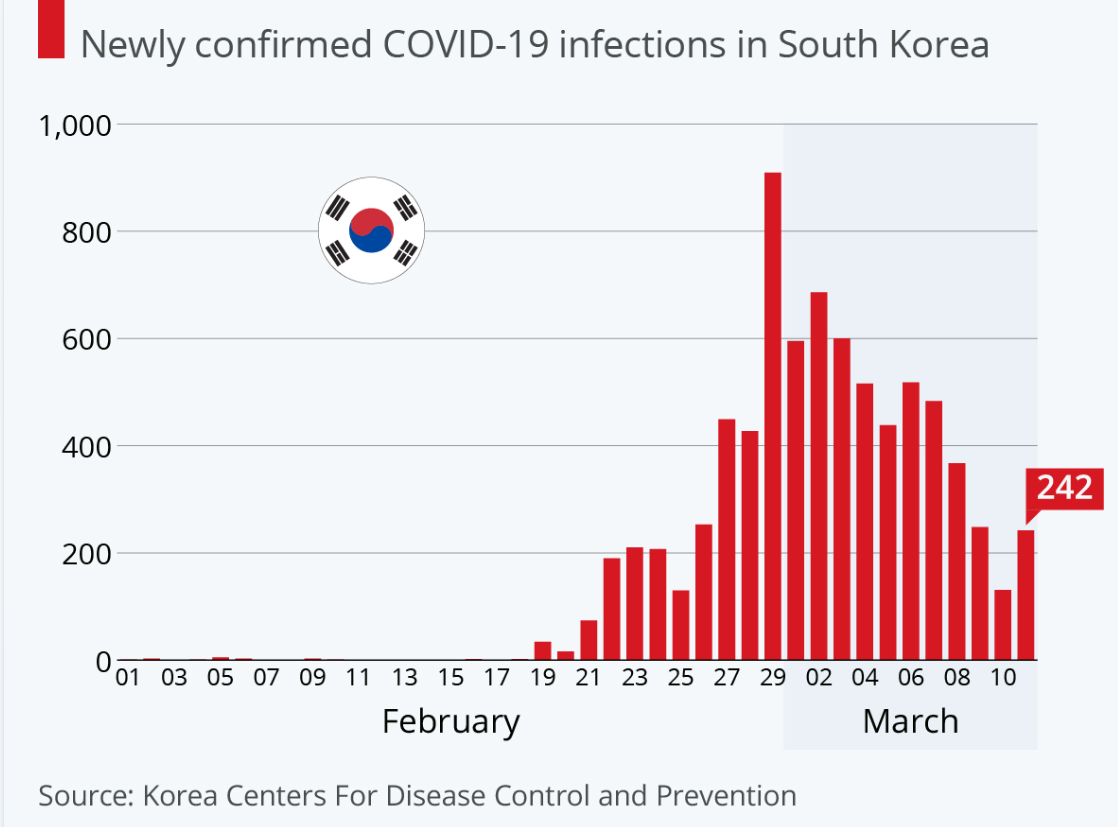

I will put monetary policy and fiscal policy aside for a moment as there is nothing that will move the needle in the markets quicker than reports that the health fears are subsiding, being contained, being tested, showing recovery, and generally re-instilling public confidence. The numbers in China and South Korea have moved dramatically in the right direction, with new diagnoses collapsing, and cure rates being very high.

* Pantheon Macroeconomics, U.S. Economic Chartbook, March 12, 2020

The markets have swooned in concert with American panic around the epidemic, and when the wide array of behaviors and actions taken in the U.S. create a reversal of diagnoses here in the states, that will trump all other categories relevant to this dynamic. Timing this is impossible, so I have to say to you two things (because it is hard to appreciate this when each hour the news pop up a new school closing or sporting event shut down):

(1) The market will begin recovering before things feel totally better, because markets are discounting mechanisms. Markets don’t need the entire health picture to be better; they just need it to begin to trend better.

(2) This. Is. Going. To. Happen. We are going to contain this, and we are going to resume normalization. I do not know when. But I have to stay invested, not because I think I know when it will happen, but because I know that I do not.

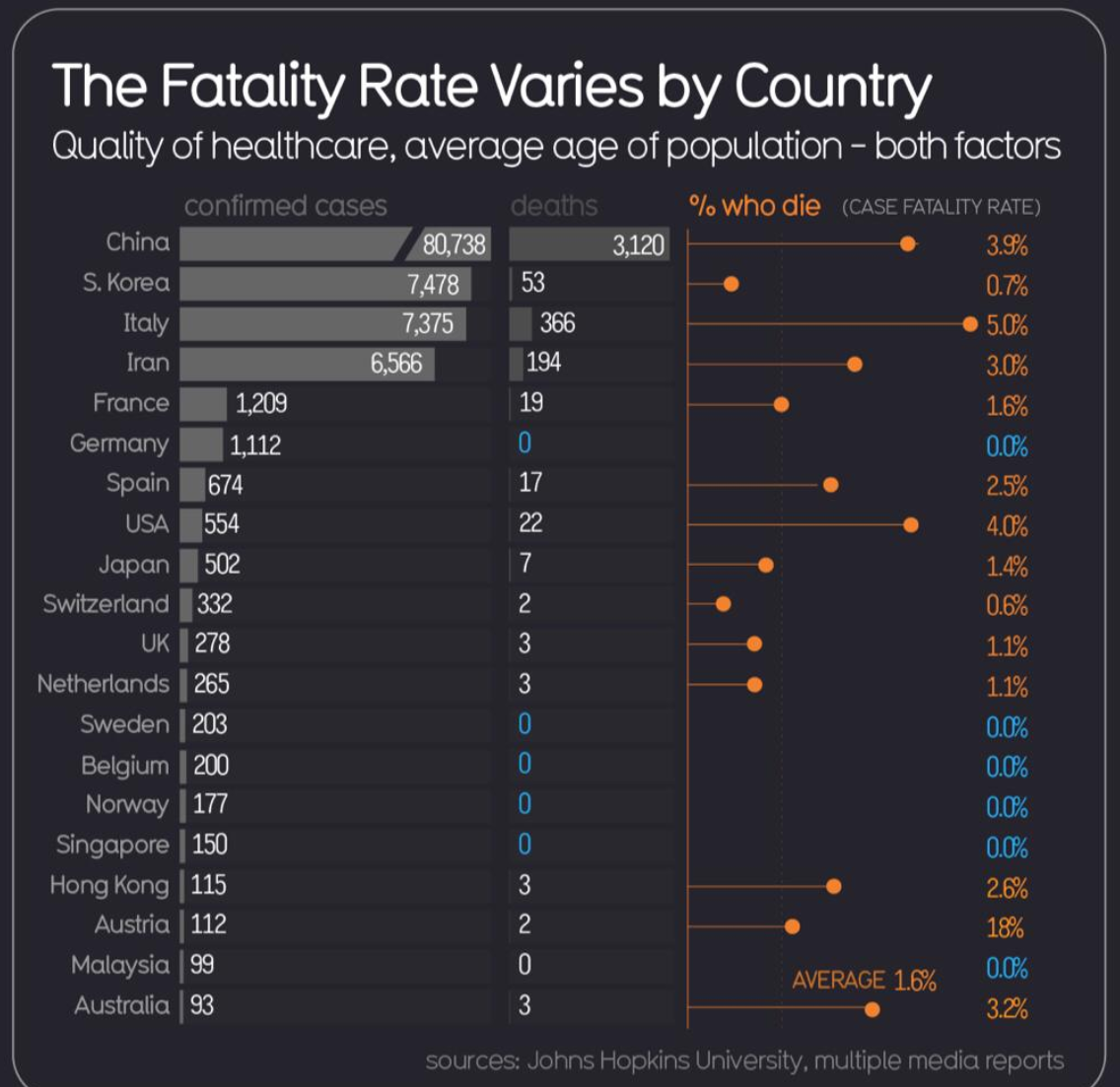

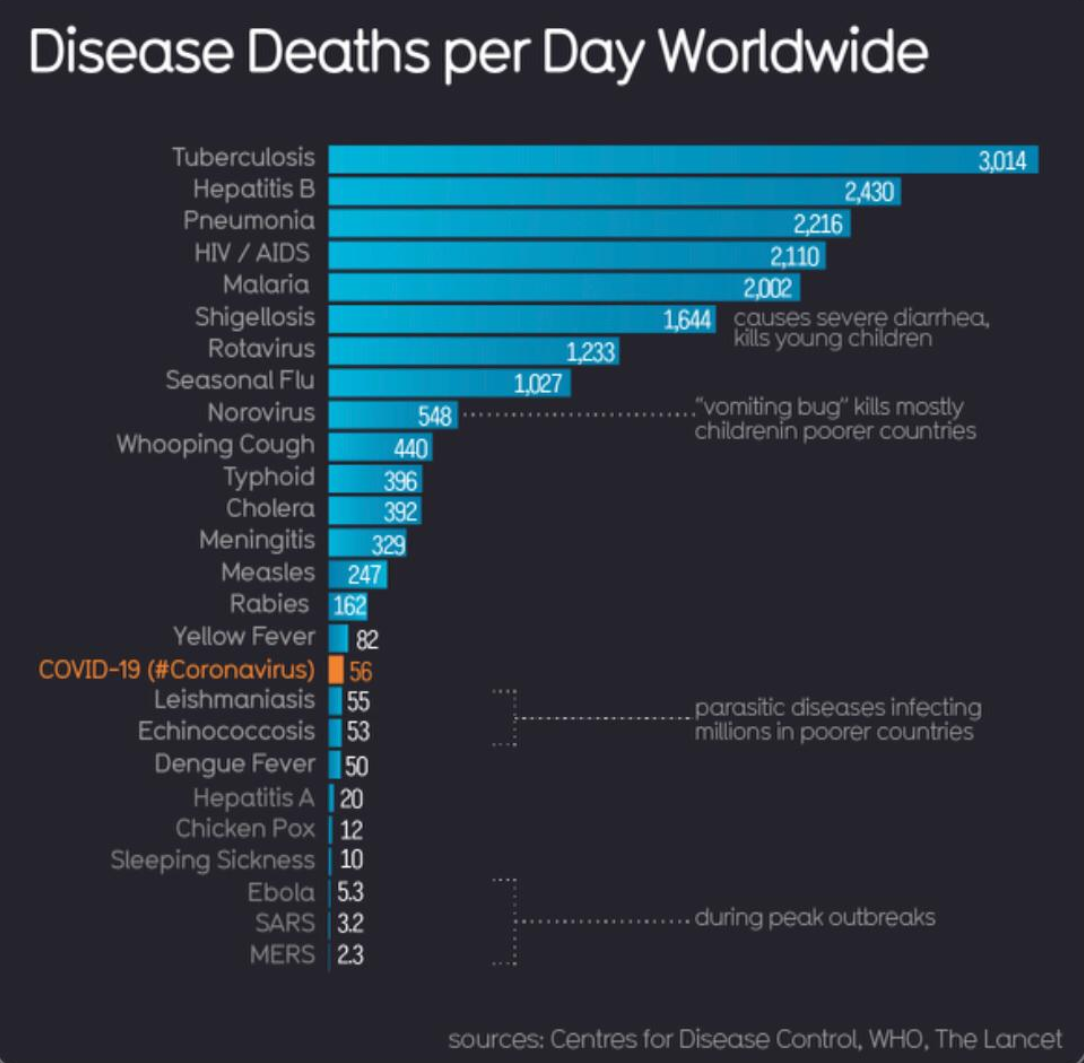

The other piece I will say on the health care aspect … This is a pandemic creating great economic contraction as goods and services decline towards the end of defeating it. But the high cure rate and low mortality rate warrant understanding.

* Johns Hopkins University, March 11, 2020

* Center for Disease Control, World Health Org, March 11, 2020

Oil Price War

This one will receive more elaboration in an early week Dividend Cafe next week, as unpacking Saudi/Russia/shale particulars will require more focus.

Monetary Policy

As I was typing this Friday morning, the Fed announced that they would begin buying Treasury bonds across all durations, starting with the 30-year bond. Yields at the long end of the curve jumped on the news, providing needed steepening to the curve. These purchases were not part of a new commitment (i.e. quantitative easing) but stated to be “interventionist” to “address a particular market dislocation.”

In the coming days and weeks, largely dependent on how bad things get in the market, the Fed has other policy tools they may consider deploying:

- An emergency term auction facility to provide liquidity to commercial enterprises

- We’ve already discussed the zero-bound fed funds rate we think they will go to or near next week

- Forward guidance that they plan to stay at their effective lower-bound rate (ELB) for the foreseeable future (maybe even increasing inflation target to 2.5%)

- Very direct and aggressive, explicit quantitative easing (commitment to a continued path of enhanced balance sheet)

- A cut on interest paid on excess reserves

- Significant reductions on capital requirements at the banks (encouraging them to lend, and assisting bank profitability)

Fiscal Policy

This area concerns me. Market expectations for a major federal plan are very, very high. There is huge exposure to disappointment, and sell-off should a plan not surface in the short term. My friends at Strategas Research have taken to calling the stock market the “vigilante” here that forces a Congressional and Executive action.

And again, as I type, news has come out that President Trump is holding a press conference at 3:00 pm eastern today (which I will note, is before the market close). That means you are reading this after he has announced what is likely a “micro deal” with Speaker Pelosi. From what we hear, a bigger macro deal is still needed. If indeed he is announcing something materially stabilizing for markets, we will know in the final hour of Friday trading. A reversal is also possible.

We expect to hear that there will be assistance around family and sick leave, free testing, easing of requirements for social benefits, enhanced unemployment benefits, more Medicaid funding, and possibly more.

Beyond this “micro” bill, the other fiscal tools still on the table include a payroll tax cut, targeting industry support (airlines, hotels, cruise ships), a tax credit to incentivize moving manufacturing back to the U.S., and more SBA loan expansion. The talk of changing the April 15 tax due date is still out there, too.

How to think about investing as an investor

Market volatility and distress are so common in the life of an investor (and always painful) and so common throughout my study of history that I have tried to develop the right practices, questions, thoughts, and structure around why an investment portfolio ought not be discarded or dramatically altered during inevitable periods of uncertainty and pain. Several thoughts and considerations I encourage investors to think through at times like this:

(1) If there is a temptation to sell, would I be bothered by markets rallying higher right after I just changed temporary volatility into a realized loss?

(2) If there is a temptation to sell, am I comfortable both with my timing for exit, and my thoughts around re-entry? What exactly is my plan for re-entry? If it is to come back into the market 10-20% higher, does that actually make a lot of sense?

(3) Does my present life situation actually economically suffer from the current market volatility, or is it more general angst around watching the values fall?

(4) Was my portfolio constructed with the awareness that risk assets not only can but do fall on occasion? Has something happened outside the bandwidth of expected downside occurrences?

(5) When I look out to a more reasonable timeline than next week (say, next year), do I see this present malaise still dominating headlines, or do I see these things being in the rear-view mirror?

(6) Has anything about the rationale of ownership for any investment holdings I have materially changed through this downturn?

(7) Is my cash position adequate (between cash reserves and expected continued liquidity/income needs) to avoid touching the risk assets in my portfolio?

(8) Do I trust my financial advisory team to guide me through this?

The intent here is to use the questions to center the important issues, and allow the answers to provide clarity and confidence. Or, if they simply create more questions, to drive further conversation with your advisors.

Retirement planning

I have found the last few weeks as challenging and painful and stupefying as everyone else has, especially this week. But I owe it to my clients and to other readers who are actually real-life people with real-life financial goals to say something practical …

Three weeks has never ruined a 30-year retirement plan, and it won’t yours.

One dependent on market prices for withdrawals has a flawed plan. We build our business and investment philosophy for the clients whom we love differently.

I don’t want to see asset prices decline this quickly, ever. And I hate the feeling that we really don’t know how far or for how long they may decline. But I do know that we have not positioned our client’s withdrawal needs around the stability of stock asset prices. This becomes a brutally important reinforcement of the withdrawal characteristics of dividend growth investing. It just does.

Politics & Money: Beltway Bulls and Bears

- I will be doing a deep dive into what a Joe Biden Presidency would mean (for good or for bad, for investors) once things settle with markets and this particular health scare. Biden’s chances over Trump have skyrocketed in the last few weeks for obvious reasons.

Chart of the Week

I hope this gives you optimism and understanding.

Quote of the Week

I had this quote taped to my desk from September 17, 2008, the day my father would have been sixty years old and the day Morgan Stanley almost went under when the financial crisis was spiraling out of control. It stayed on my desk as a daily read until March 9, 2009, when the market recovery began.

“I am a little wounded, but I am not slain;

I will lay me down and bleed a while.

Then I’ll rise up and fight again”

~ John Dryden

********************************************

“History provides a crucial insight regarding market crises: they are inevitable, painful and ultimately surmountable.”

~ Shelby M.C. Davis

* * *

I invite every one of you to join our conference call on Tuesday, the 17th. I beg you to remember there will be more volatility before stability. I reaffirm my commitment to telling you the truth and recommending the right behaviors and responses all the way through.

And I promise you, this too shall pass. For now, we must think longer term than this quarter and the next. We simply must. To that end, we work.

May God heal those afflicted, above all else, and prevent further affliction. Amen.

With regards,

David L. Bahnsen

Chief Investment Officer, Managing Partner

The Bahnsen Group

www.thebahnsengroup.com

This week’s Dividend Cafe features research from S&P, Baird, Barclays, Goldman Sachs, and the IRN research platform of FactSet